Introduction

In present business climate which is so competitive, we see that companies are very much into using data for better financial and managerial decisions. Accounting has outgrown the roles of bookkeeping and record keeping; it has transformed into a strategic function which includes forecasting, risk management, auditing and operational efficiency. To that we see statistical decision theory in accounting as a very powerful tool.

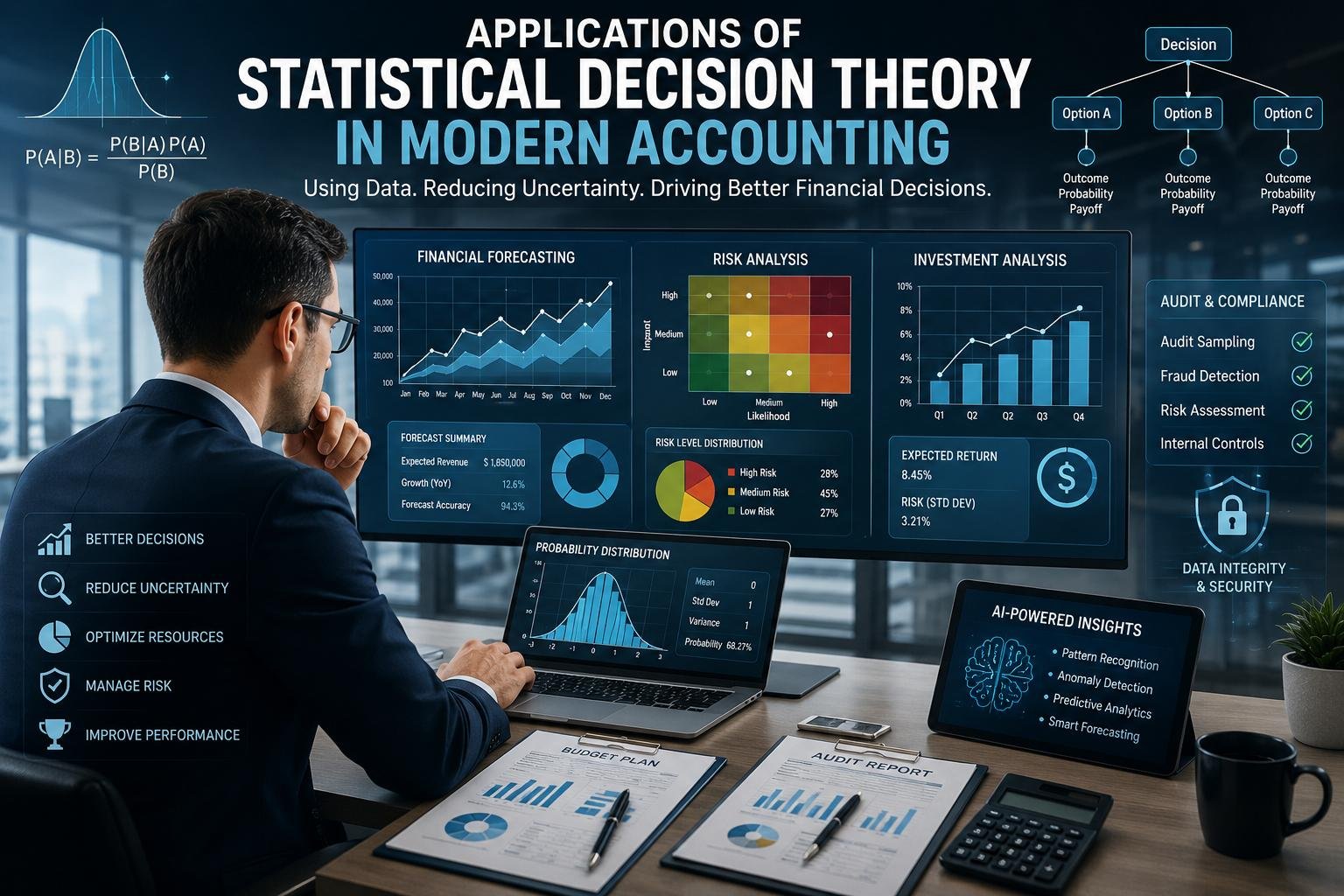

Statistical decision theory is a field which puts together statistics, probability, and decision making to that which companies may choose the best action in uncertain times. We see it in play when we note that companies study financial reports, which they use to determine what will play out, which in turn they use to better their bottom line and also to improve their financial control. Today’s accountants and financial managers use stats based models to look at investment options, to see what audit issues may come up, to project what the markets will do, and to put organizational resources in the best place.

As we go into what is uncertain economic climate for many businesses today statistical decision theory has grown in importance within the fields of accountancy and finance. Companies are using it to improve their business growth plans, which in turn improves budgeting processes and we see more accurate financial forecasting. Also through the use of quantitative analysis companies are able to identify risk factors which may become large scale issues and thus are making better informed strategic decisions.

Understanding Statistical Decision Theory

Statistical decision theory is a framework which applies statistical tools and probability analysis to decision making in uncertain conditions. It presents a methodical way to assess different actions and choose the best option which is supported by the available data.

The theory which is made up of three main elements:

- Decision alternatives

- Possible states of nature

- Outcomes or consequences

In the world of accountancy managers and auditors often find themselves in uncertain situations. For example a company may have to determine which of the following to do invest in a new project, expand operations, extend credit sales, or look into suspicious financial transactions. As the future is not predictable with certainty statistical decision theory is used by organizations to determine probabilities which in turn support better decision making. This approach increases the objectivity of financial management which is a result of making decisions on measurable evidence instead of assumptions or intuition.

Statistical Decision Theory’s Role in Accounting

Accounting professionals apply statistical decision theory to which they present financial info and in support of business goals. The theory is used to identify trends, to predict future results, and to assess risk related to financial decisions.

Its role in accounting includes:

- Improving financial forecasting

- Supporting budgeting decisions

- Enhancing auditing procedures

- Managing financial risks

- Evaluating investment opportunities

- Strengthening internal controls

- Improving operational efficiency

Modern companies produce large sets of financial information every day. Statistical tools which in turn help accountants to present this info in a useful way for business.

Applications in Business Planning

In the field of business planning statistical decision theory is very key. Companies for growth and sustainability put great value in accurate plans. Statistical models in this context are tools which managers use to obtain reliable info that in turn supports strategy.

Forecasting Revenue and Sales

Businesses analyze past financial data in order to project future sales trends. Statistical forecasting models which are used by organizations also determine customer demand, see through seasonal changes, and report on market behavior. For instance, retail businesses study past sales trends in order to set out stock levels for coming seasons. Correct forecasting which in turn improves profit and reduces the incidence of over and under stocking.

Budget Preparation

Budgeting is a fundamental aspect of accountancy which requires that we do careful analysis of revenues and expenses. Statistical decision theory enhances budget preparation by looking at past financial performance and forecasting what is to come.

Organizations may use probability analysis to project multiple budgetary scenarios that range from the best case to the worst case which in turn include growth in inflation, competition in the market, and economic decline. Also we see this as a way for companies to put in place plans for when the unexpected happens.

Resource Allocation

Companies need to put their resources in the best use for the highest productivity and profit. We see that statistical decision models are a tool which managers use to determine how to best allocate funds, labor, and equipment between different departments or projects. For example a manufacturing firm may use statistical analysis to determine which production line to put more investment in based on expected return and operation efficiency.

Strategic Expansion Decisions

Before going after new markets or rolling out new products companies have to look at what the risks and rewards are. Statistical decision theory is a tool which management uses to determine the probability of success by looking at how customers behave, what the market is doing, and what the competition is up to. This decreases uncertainty which in turn allows organizations to make better expansion decisions.

Applications in Auditing

In the field of auditing which is a large area statistical decision theory plays a role. Auditors include evaluation of financial statements, detection of irregularities, and assessment of the reliability of accounting info. Every financial transaction cannot be reviewed is the issue at hand auditors turns to statistics for better results.

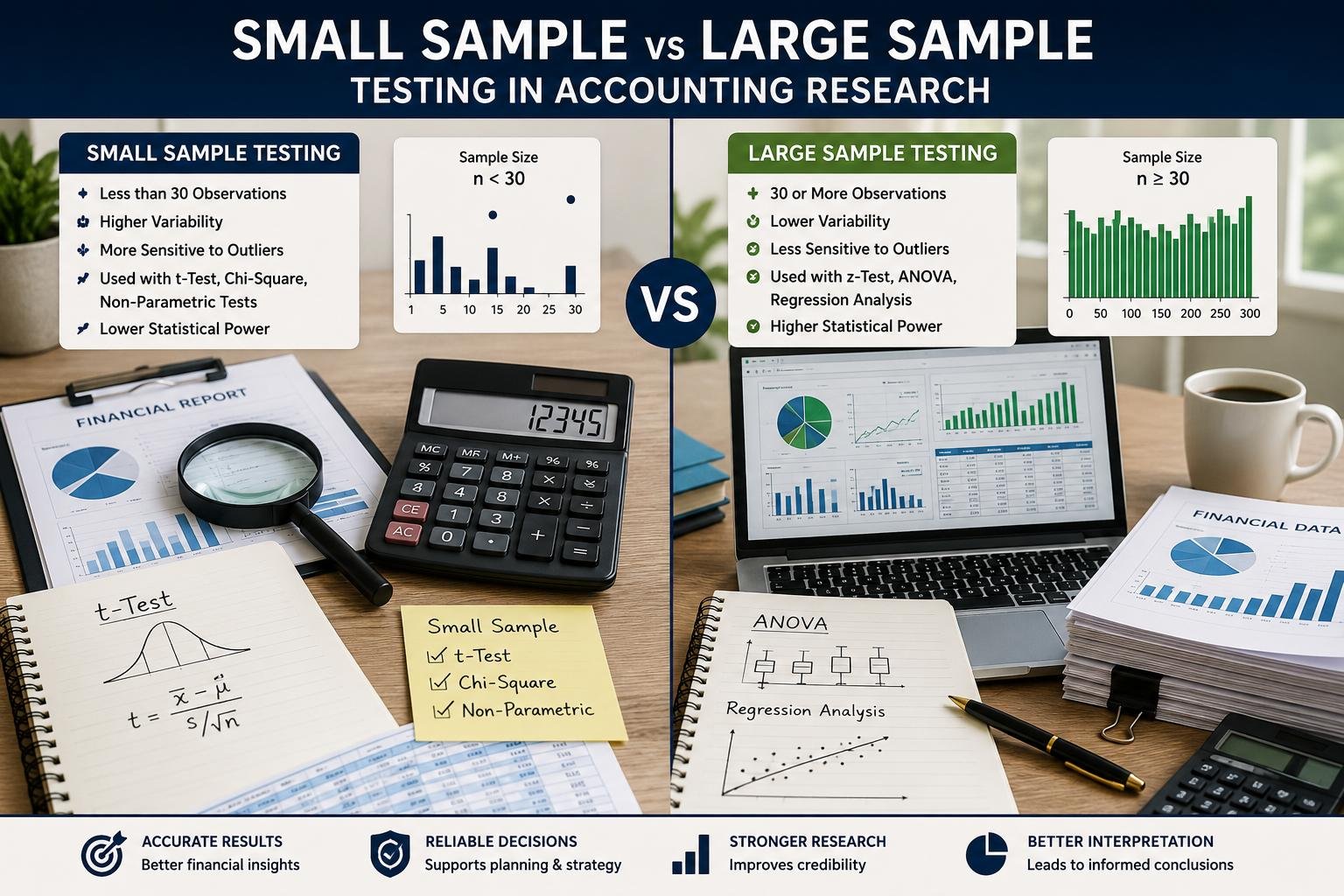

Audit Sampling

Audit sampling is a process in which only a segment of financial transactions are checked rather than the total set. Statistical decision theory provides auditors a tool in determining proper sample sizes and in which to assess sampling risk. Through use of probability based sampling techniques auditors are able to draw reliable conclusions regarding financial reports at the same time also reduce costs.

Fraud Detection

Organizations are seeing an increase in financial fraud and manipulation. Statistical models which auditors use to identify out of the ordinary transactions and telltale financial patterns. For instance auditors that perform statistical analysis which in turn may detect out of the ordinary expense claims, repeat payments, or which may catch unauthorized transactions. We see that early fraud detection which in turn reduces financial loss and also protects organizational assets.

Risk Assessment

Auditors determine what the risk is for financial statements and internal controls. In terms of statistical decision theory auditors are able to put numbers to the chance of material misstatements and to focus on high risk issues during audit processes. This increases audit quality and we also see that we efficiently use auditing resources.

Internal Control Evaluation

Internal controls are structures put in place to protect company assets and present accurate financial reports. Statistical analysis is used by auditors to determine the effectiveness of these controls. If reports point out many issues of error and inconsistency management may put in better controls to minimize operational risk.

Applications in Financial Management

Financial management is a process of planning, organizing, and controlling financial resources to accomplish organizational goals. In statistical decision theory we see that which financial managers use to make informed decisions in uncertain conditions.

Investment Decision-Making

Investors and at times financial managers present themselves in a state of uncertainty while choosing which investment opportunities to pursue. Statistical decision models which is a tool we use to determine the best course of action help us to estimate what the returns will be and also the risks involved. Through analysis of many investment options organizations are able to choose the ones which best balance profit with risk.

Cash Flow Management

Cash flow is essential to business survival. Companies use statistical forecasting which helps to determine future cash in and out flows. This allows companies to have sufficient liquidity, to avoid cash shortages, and to plan for future financial obligations.

Credit Risk Analysis

Financial institutions and business use statistics in risk assessment of customers and borrowers. By looking at past payment behaviors, income levels, and financial reports organizations can see which customers are at a higher risk of default and improve their lending choices.

Cost Control and Profitability Analysis

Businesses use statistics in tracking operational costs and determining profitability. Decision theory which in turn helps us to identify inefficient processes, unnecessary expenses, and areas for cost reduction. As a result organizations better their financial performance and also preserve their competitive edge.

Reducing Uncertainty in Decision-Making

One out of the best aspects of statistical decision theory is that it does away with uncertainty. Business settings are always in a state of change due to economic shifts, tech advances, and competitive markets. Statistical analysis is a tool which organizations use to predict results and in turn prepare for them.

Probability Analysis

Probability study is what businesses use to determine the chance of various events’ occurrence. Managers put forward different what if scenarios and develop contingency plans. For instance a business may determine the chance of a drop in customer demand and change production levels to prevent losses.

Scenario Analysis

Scenario analysis is a tool which looks at a range of possible future outcomes based on different assumptions. Companies are able to look at best case, worst case, and moderate scenarios before they make key financial decisions. This increases our readiness for and the effect of unexpected events.

Decision Trees

Decision trees are a visual means of looking at complex decision making issues. They allow managers to put forth different actions and see out the results. In investment analysis, budgeting and project management decision trees are used.

Improving Operational Efficiency

Statistical decision theory plays a large role in improving operational efficiency which in turn sees organizations optimize their processes and increase productivity.

Inventory Management

Companies use statistical analysis in setting the best inventory levels. We see that which inventory practices are best for minimal cost and maximum product availability.

Production Planning

Manufacturing companies use statistics in their production schedules and in turn reduce operational disruptions. Through accurate demand prediction businesses are able to maintain efficient production processes and reduce idle time.

Workforce Planning

Human resources professionals use statistical models to determine labor needs and assign employees accordingly. This is a way for companies to maintain productivity at the same time as they control labor costs.

Performance Measurement

Organizations report on statistical performance indicators which cover employee productivity, departmental efficiency, and financial performance. These measures support a culture of continuous improvement and better decision making.

Benefits of Statistical Decision Theory in Accounting

Statistical decision theory in its application brings many benefits to organizations and accountants.

- Better Decision Accuracy: In general decisions which are based on statistics prove to be more reliable that those based on assumptions or intuition.

- Improved Risk Management: Organizations can improve the identification and response to financial risks with the help of probability analysis and forecasting.

- Efficient Resource Utilization: Statistical analysis is a tool which businesses use to allocate resources better and reduce waste.

- Enhanced Financial Forecasting: Forecasting tools which in turn improve revenue prediction, budgeting and investment planning.

- Stronger Internal Controls: Data analysis allows companies to identify errors, fraud, and operational deficiencies early.

- Increased Competitive Advantage: In dynamic markets businesses which put data at the core of their decisions do better.

Challenges of Applying Statistical Decision Theory

Despite of what it has to offer statistical decision theory also has issues.

- Data Quality Issues: Quality data is the base for accurate analysis. Poor quality financial data may give false results.

- Complexity of Statistical Models: Some statistical methods require in depth knowledge and are hard for those that are not experienced.

- Cost of Implementation: Large scale investment is often required in advanced statistical software and analytical systems.

- Dependence on Assumptions: Statistical models use assumptions which do not always which do not hold in the real world.

- Rapidly Changing Business Environments: Economic and market conditions fluctuate rapidly which in turn affects the reliability of forecasts and predictions.

Technology and Statistical Decision Theory

Technological progress has greatly improved application of statistical decision theory in accounting.

Artificial Intelligence and Machine Learning

Today’s accounting systems use artificial intelligence and machine learning to identify patterns in large data sets which they do so automatically. These technologies improve upon fraud detection, financial forecasting, and risk analysis.

Big Data Analytics

Organizations today have at their disposal large sets of financial and operational data. Big data analytics is what accountants use to mine out that which is useful from it.

Cloud-Based Accounting Systems

Cloud based accounting software which does real time analysis and fast decision support.

Automation

Automation improves human error and increases the speed and accuracy in financial analysis.

The Future of Statistical Decision Theory in Accounting

The in future we will see that which is related to accounting to still very much includes data analytics and statistical decision making tools. As companies deal with greater levels of uncertainty and competition the need for data driven financial management will grow.

Future developments may include:

- Greater use of predictive analytics

- Advanced fraud detection systems

- Real-time financial forecasting

- Increased automation in auditing

- Integration of AI into accounting systems.

Accountants in today’s business world will need to develop their analytical and technical skills.

Conclusion

Statistical decision theory in accounting are at the core of what we see in today’s accounting, auditing, and financial management. By using statistics in the decision making process organizations are able to reduce uncertainty, improve forecast accuracy, and see greater operational efficiency.

In the present day business environment which is very much data driven we see the value of statistical models in business planning, audit, investment analysis, budgeting, and risk management. Companies use these models for better decision making, resource allocation, fraud detection, and to improve financial performance.

Although there are issues like that of data quality and model complexity which we see today, still we see that technical improvements are what is putting forward the value of stat based decision making in the field of accounting. As companies produce more data and compete in more dynamic markets, statistical decision tools will play a key role in to achieving financial health and organizational success.

Get more well researched information about statistical decision theory in accounting here.