Introduction

In present day’s competitive business world companies are at a continuous put to manage resources well, contain costs, and maintain financial discipline. To that end we see that which do best are those that have put in place excellent accounting control systems. These accounting control systems put in a structure for which financial activities are monitored, which in turn promotes accountability, and also which play a role in what decisions are made.

Standard cost and budgetary control. In tandem these tools enable organizations to look to the future, assess performance, identify what is out of line, and put right what is not. This article looks at the field of accounting control systems in detail which we do through the study of standard cost and budgetary control and we see how they play a role in achieving cost efficiency, accountability, and financial discipline.

Understanding Accounting Control Systems

Accounting control systems which are what organizations put in place to protect assets, we see to the accuracy of financial reports, and which also improve operation performance. These structures are essential to internal management’s use and also serve as the base for good financial governance.

Accounting control systems in basic terms are for businesses to answer key questions:

- Are we out of our means?

- Are our operations efficient?

- Do we have success with our financial goals?

For more insight into the structure of present day financial systems in which organizations participate see this resource on accounting control systems.

Key Objectives of Accounting Control Systems

Accounting control frameworks put in place to achieve which of the following:

- Cost management: includes identifying and reducing unneeded expenditures.

- Quality of Financial Data: Providing accurate information for decision making.

- Fraud Prevention: Lowering of financial risk.

- Performance Assessment: How we do at what we set out to do.

- Compliance: to our internal policies and external regulations.

Among in many of these systems what we see are standard costing and budgetary control which stand out as very effective.

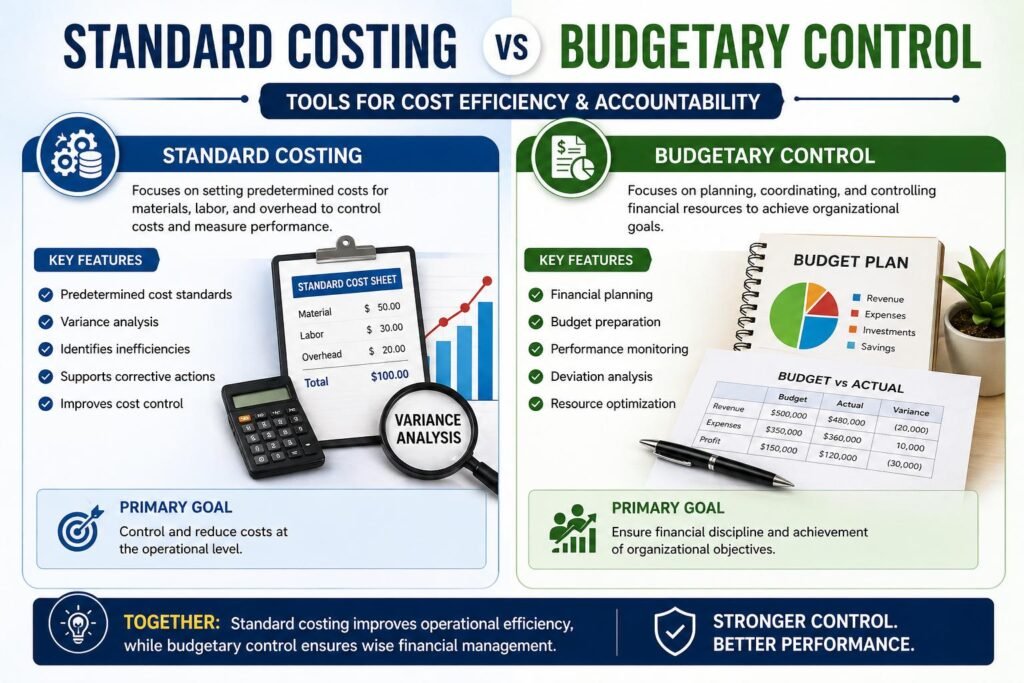

Standard Costing: Tool for cost control.

What Is Standard Costing?

Standard cost which is a method of setting out put costs in advance. We determine standard costs which are in fact estimates of what materials, labor, and overhead will total in an ideal operational state.

Instead of going till we see what the true costs are, companies set benchmarks in advance. These benchmarks serve as targets which in turn make it easy to measure performance and identify inefficiencies.

How Standard Costs Are Set

Setting out standard costs is a detailed exercise in analysis and we usually see it done in this way:.

- Material Standards: Determining the amount and price of raw materials.

- Labor Standards: Determining labor time and wage rates.

- Overhead Standards: Distributing indirect costs by activity levels.

These standards are from past data, industry benchmarks, and engineering studies.

Variance Analysis

A standard costing element which is very much is variance analysis that looks at actual costs as compared to budgeted.

- Favorable Variance: When real costs are below standard.

- Unfavorable Variance: When we see costs go over the standard.

For instance, a company that budgets for 12 has an unfavorable variance.

Variance analysis helps managers: Variance analysis for managers:

- Identify inefficiencies

- Investigate causes of deviations

- Implement corrective actions

Benefits of Standard Costing

- Improved Cost Control Reduced costs: Standard cost systems which in turn enable companies to watch over their expenses very closely and also reduce waste.

- Improved Performance Measurement: Employees’ and departments’ performance is measured against pre-determined standards.

Better Decision-Making: Managers may base their decisions on variance reports.

Simplified Accounting Processes: Standard costs simplify inventory valuation and cost tracking.

Limitations of Standard Costing

While helpful at times standard costing also has issues:

- Standards may fall behind if not revised regularly.

- It does not work well in very dynamic industries.

- Overemphasis on cost control affects quality

Although of these constraints, standard costing is still the base element of good accounting control systems.

Budgetary Control: Planning and Reporting Financial Results.

What Is Budgetary Control?

Budgeting is the preparation of budgets which is then compared to actual results and taking corrective action as required. Also a tool for planning and control helps organizations to maintain financial focus.

A budget is a financial plan for a time frame which also puts forth what monies will come in and out, It is a method of looking at future income and expenses over a certain period of time. A budget is a report which we create for a specific time which includes what we think will come in and go out. Also it is an overview which we present of the financial actions we as an individual or a business see playing out in a given period.

Types of Budgets

Organizations have a variety of budget types based on their needs:

- Operating Budget: Includes daily expenses and revenues.

- Capital Budget: Puts in large time based investments.

- Cash Budget: Monitors income and outgoings.

- Flexible Budget: Tunes in to activity levels.

The Budgetary Control Process

Budgetary management includes the following steps:

- Setting Objectives: Setting financial goals which support the organization’s strategy.

- Developing Budgets Developing out in depth plans for income and expense.

- Implementing Budgets: Allocating resources and executing plans.

- Tracking Progress: Comparing actual results with budgeted figures.

- Implementing corrective measures: Addressing deviations and improving future performance.

Benefits of Budgetary Control

- Financial Discipline: Budgets set spending parameters which in turn help organizations avoid overspending.

- Enhanced Coordination: Departments are in sync for our financial goals.

- Performance Review: Managers may look at budget adherence.

- Proactive Planning: Organizations are aware of upcoming issues and opportunities.

Limitations of Budgetary Control

- Budgets are also at time inflexible and do not adapt quickly to change.

- Preparing budgets can be time-consuming.

- Unrealistic budgets may demotivate employees.

Also in practice budgetary control is a strong tool which is used to maintain financial stability.

Relationship between Standard Costing and Budgetary Control

Standard cost and budgetary control are very much related and in many cases are used together in accounting control systems.

- Standard cost is a per unit measure which also includes.

- Budgeting is for large scale financial issues.

They present a full scale solution for cost management.

For example:

- Standard cost analysis brings to light production inefficiencies.

- Budget control which in turn keeps spending in check.

This integration allows organizations to:

- Watch both small scale and large scale financial performance.

- Improve operational efficiency

- Strengthen accountability

Enhancing Accountability through Control Systems

Accountability is seen to greatly from the implementation of accounting control systems.

Responsibility Centers

Organizations also put out responsibility centers which include:

- Cost centers

- Profit centers

- Investment centers

Managers are responsible for their centers’ performance.

Performance Reporting

Regular reports that are based on standard costing and budgetary control which do:

- Track progress

- Highlight deviations

- Assign responsibility

This open communication in turn sees to it that employees do so very well and very responsibly.

Promoting Cost Efficiency

Cost effectiveness is a key issue for which all organizations strive. Accounting control systems play a role in this by:

- Identifying waste and inefficiencies

- Encouraging optimal use of resources

- Supporting cost reduction strategies

For example in standard costing we see that variance analysis brings to light excessive material use which in turn prompts for correction.

Also budgets serve to have spending in step with what is important to the organization.

Strengthening Financial Discipline

Financial responsibility is how an organization manages its money.

Accounting control systems promote discipline by:

- Setting clear financial targets

- Monitoring adherence to budgets

- Enforcing accountability

This decreases the chance of going over budget and also promotes sustainable growth.

Practical Applications in Business

Manufacturing Sector

In manufacturing, it is common to use which system that does:

- Control production costs

- Monitor efficiency

- Improve profitability

Budgeting plays a role in determining production levels and managing resources.

Service Industry

Service organizations use budgetary control to:

- Manage operating expenses

- Forecast revenues

- Ensure profitability

Standard cost analysis in services which includes labor time.

Small Businesses

Even small businesses profit from accounting control systems which:

- Tracking expenses

- Planning budgets

- Improving financial decision-making

Challenges in Implementing Accounting Control Systems

While we see value in them at the same time implementation of accounting control systems is a challenge:

- Resistance to Change: Employees may not accept new systems and procedures.

- Cost of Implementation: Setting up infrastructure is a large investment.

- Complexity: Systems can be hard to figure out and manage.

- Data Accuracy: Quality data is a base for good control.

To address these issues organizations must put in place training, technology, and continuous improvement.

Technology’s Role in Present Day Control Systems.

Technology has brought about change in accounting control systems which in turn has improved their performance.

Automation

Automated systems:

- Reduce human error

- Improve data processing speed

- Enhance reporting accuracy

Real-Time Monitoring

Modern software allows managers to:

- Track performance in real time

- Identify issues quickly

- Make timely decisions

Data Analytics

Advanced analytics provide insights into:

- Cost trends

- Performance patterns

- Future projections

This increases the value of both standard costing and budgetary control.

Best Practices for Effective Control Systems

In order to see the greatest results from accounting control systems, organizations should:

- Regularly update standards and budgets

- Involve employees in planning processes

- Use technology to enhance efficiency

- Conduct periodic reviews and audits

Align your control systems to organizational goals.

Conclusion

Accounting control systems which play key role in better performance, responsibility and financial health of an organization. Through the use of tools like standard costing and budgetary control, businesses are able to do better planning, monitoring, and control of their financial processes.

Standard costing gives in depth look at cost performance which in turn helps organizations to identify inefficiencies and to improve operations. In terms of budgetary control we see a more general approach to financial planning and which is to see that resources are put to wise use.

In this which we present them together we have a base for informed decision making, improved performance, and long term success. In a world of increasing business competition organizations which put in place effective accounting control systems do better in achieving their finance goals and sustaining growth.

Get more well researched information about accounting control systems here.