Introduction

Small Sample vs Large Sample testing in accounting research depends greatly on statistics which we use to study financial trends, business performance, audit results, and economic relationships. We as researchers tend to gather data from companies’ financial reports, audit samples, market reports and then we apply statistical methods to extract what we hope are meaningful results. Also of great importance in this process is the issue of what size sample we are working with which in turn determines what statistical tests are appropriate to use.

Research results’ accuracy is a function of choice of statistical method. What we put forth is that use of the wrong test may result in misdirection, inaccurate forecasts, or poor business decisions. Also it is upon students, accountants, and researchers to be aware of the issues between small scales vs. large sample testing in accounting research to report reliable results.

In the fields of accounting and finance statistical testing is used in auditing, investment analysis, budgeting, forecasting, tax studies, and performance evaluation. What the data set size is, be it small or large determines the way in which the info is analyzed and interpreted.

Financial analysis and interpretation which researchers present after conducting correct statistical testing is very important. Right statistical methods increase the value of accounting research and also support organizations in making informed financial decisions.

Understanding Statistical Testing in Accounting Research

Statistical analysis is the use of mathematical tools to study data which in turn is used to determine the validity of the results. In accountancy research we see that statistics help researchers to identify trends, compare financial results, measure risk, and test hypotheses.

In the case of an accountant who is to determine the success of a new budget strategy in improving the company’s profitability. Also a researcher may do a study on the difference in audit error rates in two departments. In both these cases what we use is statistics to determine if the results we see are in fact meaningful and not just due to chance.

Statistical test choice is based on which of the following:

- Sample size

- Nature of the data

- Research objectives

- Variability within the data

- Distribution of the population

In that which they do, sample size is a large player because it affects the reliability and behavior of statistical calculations.

What Is a Small Sample?

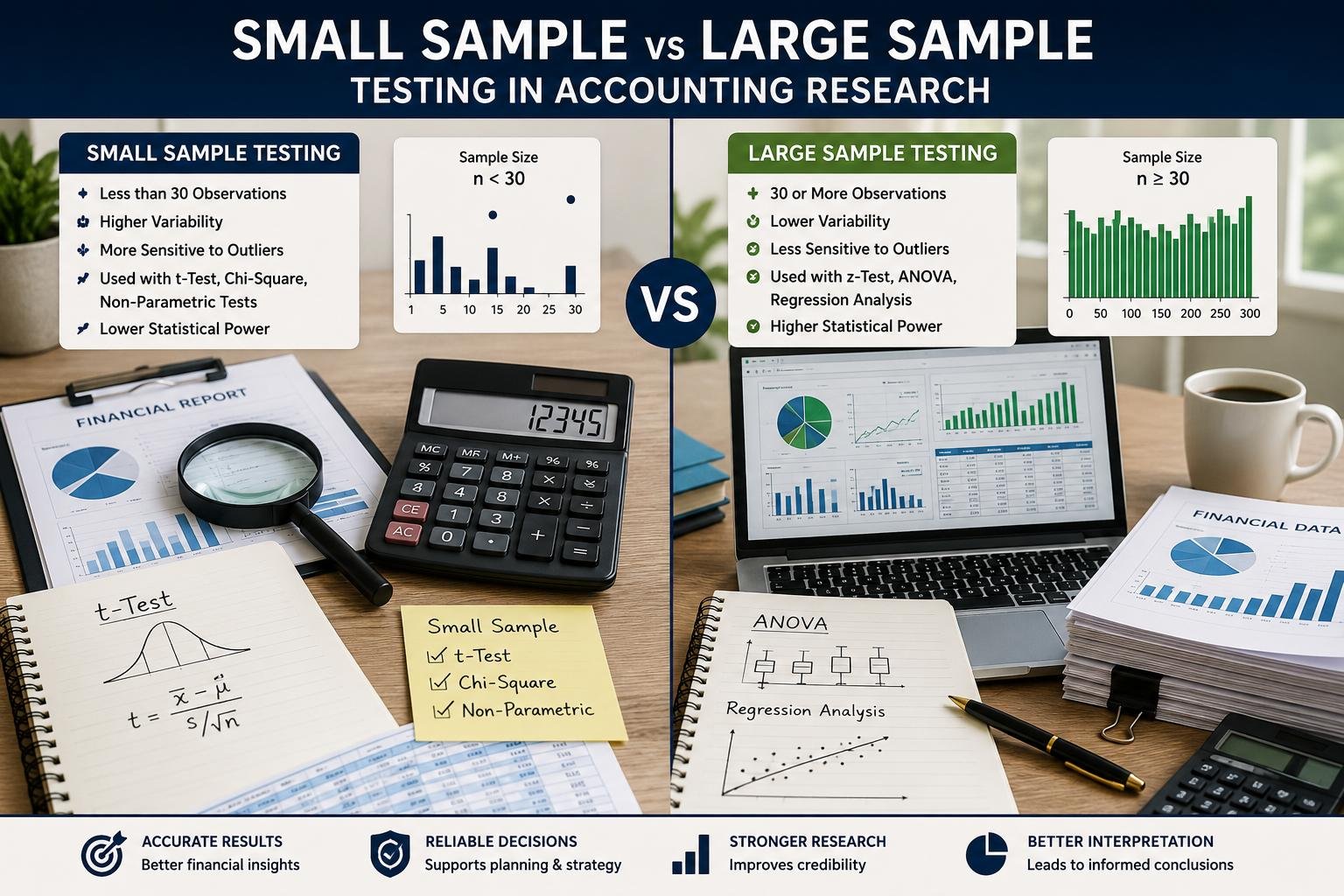

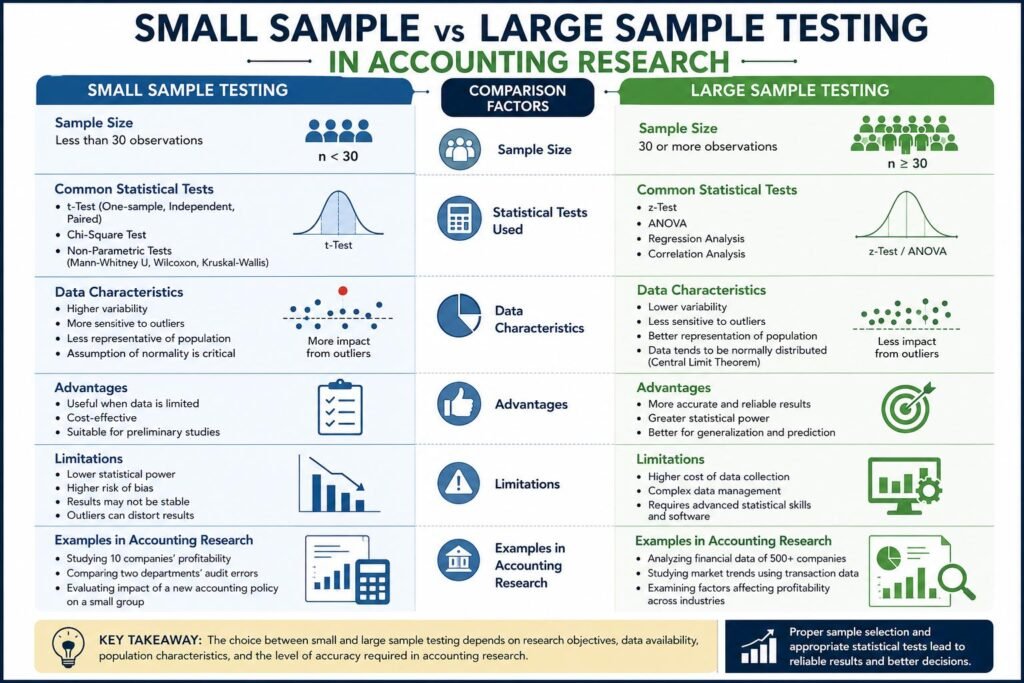

A small data set is what we use to refer to a collection of less than 30 observations. Although the exact number may vary by research field, in accounting research we see that which fall below 30 are classified as small samples.

Small samples are often used when:

- Data collection is expensive

- Limited financial records are available

- Research involves specialized organizations

- Confidential accounting information restricts access

- The population itself is small

For instance a researcher looking at the performance of ten multinationals is using a small sample.

Characteristics of Small Samples

Small sets usually have the following features:

- Limited amount of data

- Higher sensitivity to extreme values

- Greater variability

- Lower representation of the population

- Assumption of data distribution.

In small samples there is greater sensitivity to outliers. A single atypical value may greatly affect the results.

What Is a Large Sample?

In large scale studies you will see that they include at least 30 items or more. In today’s accounting research we see a trend towards large samples which is a result of digital systems which enable researchers to collect large sets of financial data very quickly.

Examples of large samples include:

- Customer transaction records

- Financial reports from a large number of companies.

- Market performance data

- Taxpayer databases

- Audit records from multiple branches

Large scale samples give out more in depth information on the population as a whole and also tend to produce more reliable statistical results.

Characteristics of Large Samples

Large samples often have these features:

- Better representation of the population

- Reduced influence of extreme values

- More reliable averages

- Greater statistical power

- Easier estimation of population parameters

In large data sets researchers see less of an impact from chance variations.

Role of Sample Size in Accounting Research

Sample number impacts the quality and reliability of accounting research. Also large or small sample size may put forth incorrect results and weak research reports.

Accuracy of Results

Large scale samples tend to give more accurate results as they include more info on the population. Small samples may not present financial reality accurately.

Statistical Reliability

As sample size grows so does the reliability of statistical tests. Large samples reduce sampling error which in turn improves confidence in results.

Decision-Making

Organizations depend on accounting research for strategic planning, auditing, investment decisions, and risk management. Appropriate sample selection supports better decision making.

Research Credibility

Studies using proper statistical tools are seen to be of greater credibility by scholars, accountants, and financial analysts.

Statistical Tests for Small Samples

Small sample analysis requires special statistical methods which at time do not follow a normal distribution. Researchers also use tests which account for uncertainty and variability.

The t-Test

The t test is a very popular method for small scale studies.

It is used to:

- Compare means between groups

- Analyze financial performance differences

- Evaluate accounting policies

- Test research hypotheses

For instance a researcher will use a t test to study the mean profitability of two small accounting firms.

Types of t-Tests

One-Sample t-Test

Used in the comparison of a sample mean to a known value.

Independent Samples t-Test

Used to compare the means of two unconnected groups.

Paired Samples t-Test

Used in which to compare related items of data, for example financial performance before and after policy implementation.

Advantages of the t-Test

- Suitable for small samples

- Simple to apply

- Widely accepted in accounting research

- When population variance is unknown.

Limitations of the t-Test

- Assumes normal distribution

- Sensitive to outliers

- Less so with very unbalanced data.

Chi-Square Test for Small Samples

The chi square test is used for determining relationships between categorical variables.

In the field of accounting research we see that it may also determine whether:

- Fraud occurrence and company size

- Audit quality and industry type

- Accounting methods and financial outcomes

However at very low expected frequencies chi-square results may be unreliable.

Non-Parametric Tests

When in small samples the assumption of normal distribution is not met researchers use non parametric tests.

Examples include:

- Mann-Whitney U test

- Wilcoxon signed-rank test

- Kruskal-Wallis test

These tests do better in that they put forward fewer statistical assumptions.

Advantages of Non-Parametric Tests

- Flexible with non-normal data

- Suitable for ordinal data

- Effective with small samples

Limitations

- Less powerful than parametric tests

- May provide less detailed interpretations

Statistical Tests for Large Samples

Large in sample size broadens the array of statistical methods available to researchers as large data sets tend to become normal via the Central Limit Theorem.

z-Test

The Z test is also used in the case of large scale samples when we know the population variance or the sample size is large.

It is used to:

- Compare population means

- Analyze investment performance

- Evaluate financial ratios

- Study market behavior

Advantages of the z-Test

- Suitable for large data sets

- Produces stable results

- Easier interpretation

- Strong statistical power

Limitations of the z-Test

- Requires large samples

- Assumes normality

- Often depends on known variance

Analysis of Variance (ANOVA)

ANOVA is used for comparing means between groups.

In accounting research ANOVA is used to determine:

- Profit margins among industries

- Audit efficiency across branches

- Financial performance among companies

Large sample sizes improve ANOVA results.

Regression Analysis

In accounting and finance research regression analysis is a key tool.

Researchers look at relationships between variables using regression which:

- Revenue and advertising expenses

- Profitability and operational costs

- Stock prices and economic indicators

Large sample sizes increase regression accuracy as more data points improve prediction quality.

Benefits of Regression Analysis

- Measures relationships between variables

- Supports forecasting

- Helps identify financial trends

- Improves business planning

Central Limit Theorem and Its Role

As we increase sample size the Central Limit Theorem reports that the distribution of sample means will approach normal. This principle is of great importance in accounting research as it enables researchers to apply normal distribution based tests on large samples even when the original population fails to be perfectly normal. Large scale results which the theorem presents are in general more flexible and reliable.

The comparison of Small Sample vs. Large Sample Testing in Accounting research

- Data Availability: Small sample studies are affected by the issue of limited data which large scale studies do not have as they benefit from in depth financial reports and large databases.

- Statistical Flexibility: Large in sample size what which researchers use a great deal of statistical methods as opposed to small samples.

- Reliability: Large scale testing tends to produce more stable and reliable results.

- Sensitivity to Outliers: Small scales of data are more affected by atypical financial reports than large scales.

- Research Cost: Small scale studies may be more economical as they include fewer data points, though this also varies by research design.

- Complexity: Large scale analysis requires in depth software and statistical knowledge.

Choosing between small and large scale samples

Researchers must look at many issues before choosing a testing method.

Research Objective

The study’s aim is what determines which test is best. In exploratory research we may see the use of small samples, in contrast to wide ranging financial research which usually requires large samples.

Availability of Data

Researchers have what data they access. In some cases of accounting studies confidentiality issues may reduce sample size.

Population Characteristics

In large and diverse populations greater sample sizes are required for accurate representation.

Statistical Assumptions

Researchers have to check that the data meets assumptions like normality and equal variance.

Software and Technical Skills

Large scale data sets may require the use of specialized accounting software and application of analytical expertise.

Applications in Accounting and Auditing

In both large scale and small scale testing we see important applications in accounting and audit.

Audit Sampling

Auditors usually review samples which is a different approach from going over each transaction. We use statistical tests to determine the reliability of financial reports.

Fraud Detection

Researchers can use statistics for the detection of atypical accounting practices related to fraud.

Investment Analysis

Financial experts use large scale studies to analyze market trends and investment performance.

Budgeting and Forecasting

Organizations model out what the future brings in terms of revenue, costs, and economic conditions.

Tax Research

Tax experts apply statistics in study of tax compliance and tax policy results.

Challenges in Small Sample Testing

Small scale studies which are what we see in this case report a number of issues.

- Limited Representativeness: Small sample sizes do not always reflect the population.

- Increased Risk of Bias: Bias is more of an issue with small sets of data.

- Reduced Statistical Power: Small scale studies may not report on significant financial relationships.

- Difficulty Meeting Assumptions: In some cases small data sets do not meet the assumptions required.

Challenges in Large Sample Testing

Large scale sets present issues although they have their benefits.

- Data Management: Large scale financial databases require effective management.

- Higher Costs: Gathering and analysis of large data sets may raise research costs.

- Complex Analysis: Advanced statistical techniques require specialized knowledge.

- Risk of Misinterpretation: Large scale studies may report statistical significance which in practice is not important.

Best Practices for Researchers

Accounting researchers should put into practice which is best to use in terms of statistical testing.

Understand the Nature of the Data

Researchers should look at the type of data which is either numerical, categorical, normally distributed or skewed.

Conduct Preliminary Analysis

Descriptive statistics help to identify trends and note outlying data before which we apply statistical tests.

Use Appropriate Software

Statistical tools improve accuracy of calculations and reduce errors.

Avoid Overgeneralization

Researchers must avoid in drawing wide sweeping conclusions from very small samples.

Interpret Results Carefully

Statistical results should be put in the context of business practicality.

Role of Technology in Statistical Testing

Today technology is a growing base for data analysis in modern accounting research.

Software applications assist researchers with:

- Data organization

- Statistical calculations

- Visualization

- Forecasting

- Risk analysis

Technological progress has made large scale testing which is a part of accountants and financial analysts work more accessible and efficient.

Conclusion

Small Sample vs Large Sample testing in accounting research are elements of what is being done. What is chosen between them is based on the research question, data availability, population features, and statistical assumptions. Small in size samples are useful at times when we have a small data set or when we are looking at very specific financial issues. We see that techniques like the t test and non-parametric tests are what researchers use to get value out of very small data sets.

Large scale studies benefit from wide representation, great reliability and high statistical power. In terms of methods we see the use of z tests, ANOVA, and regression analysis which are very common in large scale accounting research.

Understanding the distinction between small and large sample testing is key for students, accountants, and researchers in which they may choose the right statistical tools for their research which in turn reports accurate results. Also proper choice of statistics improves financial reporting, auditing, forecasting and decision making. In today’s business settings success of accounting research is a result of choosing proper statistical methods that support sound financial analysis and interpretations.

Get more well researched information about Small Sample vs Large Sample Testing in Accounting Research here.