Definition and Explanation

The book in which accounts are maintained is called a ledger. Generally, one account is open on each page of this book, but if transactions relating to a particular account are numerous, it may extend to more than one page. Ledger is known as the destination of entries in journal but it must be remembered that transactions cannot be recorded directly in the ledger; they must be routed through journal. This is illustrated below;

Uses of a Ledger

The main use of a ledger account is that after each transaction is available at a glance from the last column, so much time and labour is saved.

Types or forms of ledger accounts

There are two forms namely;

- Standard form

- Self-balancing form

Standard form of ledger account

To understand clearly as to how to write the accounts in ledger; the standard form of an account is given below with two separate transactions.

| Date | Particulars | Amount | Date | Particulars | Amount |

| 2005 | N | 2005 | N | ||

| Dec. 17 | Cash A/c | 1,200 | Dec. 17 | Purchases A/c | 2,000 |

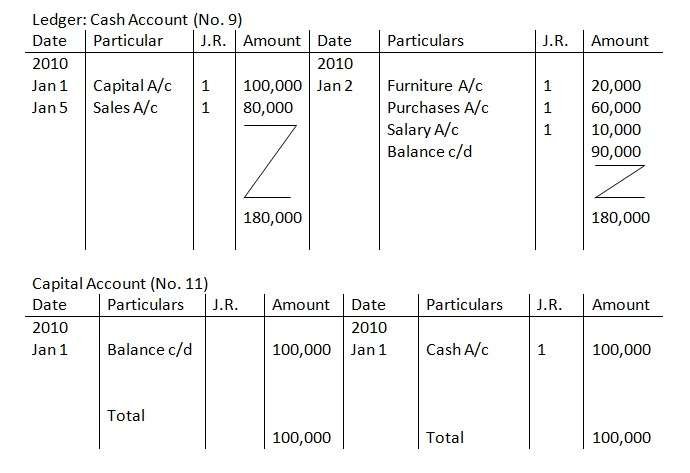

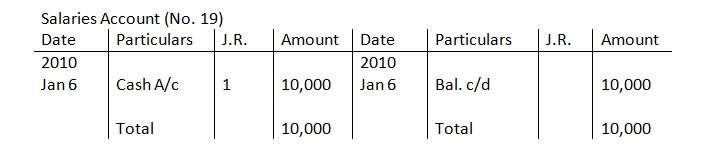

Example

Enter the following transactions in journal and post them into ledger

2010

Jan 1 Mr. Paul started business with cash N100,000

Jan 2 He purchased furniture for N20,000

Jan 3 He purchased goods for N60,000

Jan 5 He sold goods for cash N80,000

Jan 6 He paid salaries N10,000

Self Balancing Form of Ledger

In practice, the standard form of the ledger account is not used. But it is usually used for examination purposes. The advantage of the self balancing ledger is that the balance of the account after each transaction is available at a glance from the last column. So much time and labour is saved.

Extra Super Vidalista If you are looking for some thing that surely features for ED, take a look at out this wonderful product today! At our an awful lot large vidalistas doublepills site.