Introduction

In present business climate we see that companies process large volumes of financial information on a daily basis. We see that which may include products of a sale, employee payroll, bulk of the inventory purchases, tax payments, customer bills, and a great deal of other financial actions. Also due to the large size of the data set accountants and auditors do not practically look at each transaction in detail. Instead they use sampling theory in accounting statistics methods which to look at a smaller set of the data and from that draw out results that apply to the full financial picture.

Elementary principles of sampling theory are what accountants and auditors use to choose representative samples out of large sets of data. These methods in turn help professionals do better financial statement analysis which in turn reduces audit costs, minimizes errors, and improves decision making. Today sampling is a very important element in accounting statistics’ tool kit because it allows organizations to get reliable financial info without going over each and every record.

This article covers what is included in sampling theory, which methods of sampling are present in accounting, the role that sampling plays in audit processes, also we see how statistical sampling is the base for proper financial analysis and business decisions.

Introduction to Sampling Theory

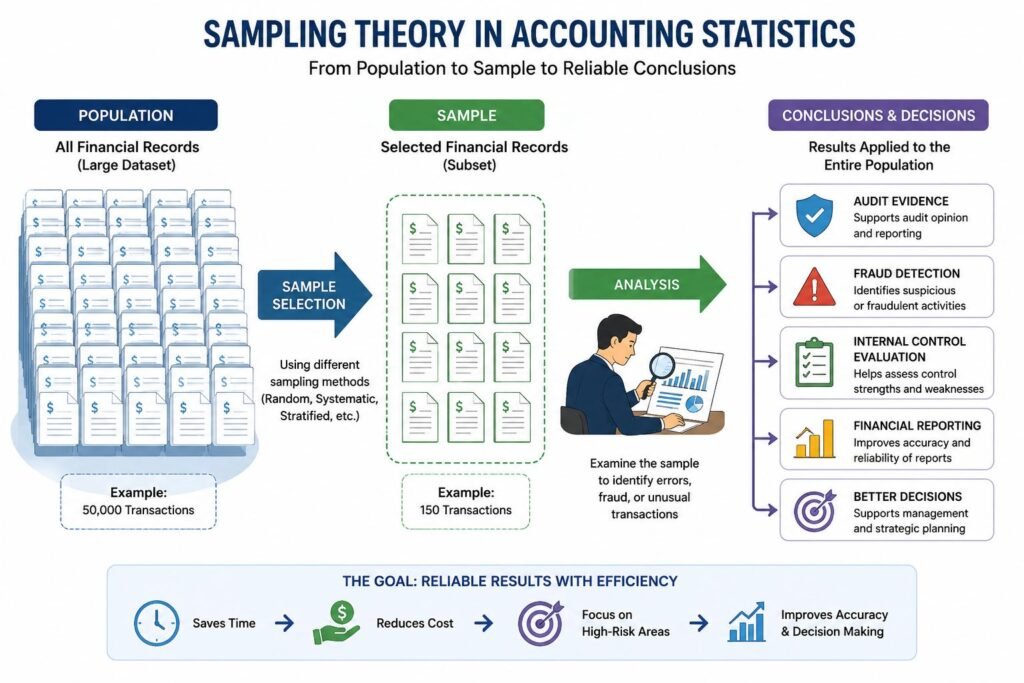

Sampling theory in accounting statistics the process which puts forward the idea of choosing a small set from a large group for the purpose of studying and analysis. In accountancy the population may include all transactions, invoices, payroll records, inventory items, or financial statements within a business.

For instance we see that some companies may have had in just one fiscal year 10s to 100s of thousands of deals. With such a large volume there is not enough time and resource to go over each one of those in detail. So rather than review all transactions in the total population which is a very broad base, accountants choose a cross section or small set of which they know to be representative of the whole. From that sample which they will analyze closely they will be able to tell if there is any error, fraud, or out of the ordinary events in the total set. Sampling theory puts forth that a well-chosen sample will reflect the full population. This allows companies to make reliable financial decisions at a faster pace and at a lower cost.

Understanding Population and Sample

To fully grasp sampling theory in accounting statistics you must understand the concepts of population and sample. A population is the full set of items or records which we are looking at in a study. In accounting that may include all sales invoices, all customer accounts, all bank transactions, or all payroll entries within a company.

A sample is a subset of the population that is put under the microscope. We take samples to make sure they are representative of the whole population. In for instance an auditor may choose 150 transactions from a set of 50,000 in the company database. What is chosen is the sample. The quality of results from sampling is very much a function of how well the sample represents the population.

Role of Sampling in Accountancy and Audit

Sampling is a key element in accounting and audit as financial data sets usually are too large for total examination. Through sampling accountants are able to perform their functions well at the same time preserve accuracy and reliability.

Sampling also has the great benefit of time which auditors use to their advantage by performing analysis on a set of chosen transactions as opposed to going over each and every record which in turn allows companies to put out reports within the required time frames.

Sampling also out does in terms of cost. What we see is that which is put through the audit process is a smaller set of records therefore businesses see a reduction in what they spend on audit procedures, labor and admin. This is very much an issue for large organizations which have millions of financial records.

Another key benefit is that of improved decision making. Accountants who are to use sampling are able to identify trends, patterns, and atypical activities in financial reports. These in turn support better strategic planning and financial management.

Sampling is also used in fraud detection. Auditors which is to say identify via analysis of a selected set of transactions large scale fraudulent activities, duplicate payments, void documentation and atypical accounting entries.

Also through the process of sampling organizations are able to conduct risk management which includes evaluation of internal controls and identification of weaknesses before they lead to serious financial issues.

In that which professional auditing does in fact present sampling as a valid method of collecting audit evidence. If the sampling procedures are well designed and we careful in their application the results may in fact be very reliable as to the health of a company’s financial records.

Types of Sampling Methods

Sampling in accountancy is mainly divided into 2 groups. We have probability sampling and non-probability sampling.

Probability Sampling

Probability sampling is a scientific approach which includes a known chance of selection for each element in the population. Also this method is of a very objective and statistical nature.

Simple Random Sampling

Simple random sampling is that which gives all items in the population an equal chance of being chosen. Also it is not uncommon for auditors to use computer software or random number generators to out of a financial database. For instance an auditor may choose 100 at random from a set of 20,000 company invoices. This method decreases the issue of selection bias and at the same time increases objectivity. But it may be difficult in very large scale populations or when we do not have full population data.

Systematic Sampling

In systematic sampling a random start is made and then every nth element is selected. For instance auditors may go over every 25th transaction in the company’s account set. This method is quicker and simpler to implement as compared to random sampling. But it does have issues when the data contains patterns which align with the sampling interval.

Stratified Sampling

Stratified sampling is broken down into strata which are subgroups of the population and from each of these we draw our samples. For example a business may put its customers into groups of small, medium, and large accounts. Then auditors will look at transactions from each group. This method improves which is that all major categories of the population are included in the sample.

Cluster Sampling

Cluster sampling which is a method of dividing the population into clusters or groups. Whole clusters are than chosen for study. For instance an auditor will choose a few company branches out which to review all financial records. This method works for companies which are present in many geographic locations as it cuts down on travel and administrative expenses.

Non-Probability Sampling

Non random sampling is based on expert judgment instead of chance.

Judgmental Sampling

In case of judgmental sampling auditors pick out what they consider to be the most important or risky transactions. An auditor may look at very large transactions or those which had issues in the past. This approach focuses auditor attention on high risk areas, but may also introduce personal bias in the selection process.

Convenience Sampling

Convenience of which is what we see in convenience sampling that which elements are the most accessible. For instance accountants may look at present records instead of getting into archived files. Although we see that this method saves time it also has issues in that it may not truly present the whole picture which in turn is an issue of its reliability.

Sampling Risk in Accounting

Sampling risk is that we may find different results as a result of studying a sample as opposed to the full population. In which auditors determine that financial reports are free of error when in fact they contain material mistakes we see one type of sampling risk. Also this may lower audit quality and misinform stakeholders.

Another case is when auditors report large issues in which there are in fact no errors present. This results in overzealous audit which in turn increases audit expenses. Managing audit risk is a primary role of accountants and auditors. For that they put in proper sample design, large enough sample size, and careful analysis.

Statistical Sampling and Non-Statistical Sampling

Accounting professionals have a choice between statistical and non-statistical sampling methods that they make is based on the audit at hand. Statistical sampling which is based on mathematical probability is used to choose and evaluate samples. It allows auditors to determine sampling risk in an objective way and to draw more scientific conclusions.

Non statistical sampling which we see to be based mostly on professional judgment and experience. Though it may be a simpler tool to use it is also more subjective. Both of these methods are used in accountancy we report that the choice between them is based on audit goals, resources at hand, and the degree of financial information complexity.

Determining Sample Size

Choosing the right sample size is at the core of sampling theory. Too small a sample may give us unreliable results, at the same time a very large sample may waste time and resources. Several factors influence sample size decisions. Population count is an important issue. In the case of large populations may see large samples required although the relationship is not always so simple.

Confidence in results also plays a role in determining sample size. As confidence levels go up we see that sample sizes go up also which is to say that auditors seek out larger samples for greater accuracy in their results. Expected error rate is also a factor. If auditors think that the population has large number of errors they may increase the sample size.

Material issues also play a role in which errors are caught out. Material issues in this context refer to the scale of errors in financial reports. Larger accounts which also may be more prone to error have a greater need for in depth analysis. Audit risk is a key issue. In high risk audit situations we see larger sample sizes as a requirement for greater reliability.

Applications of Sampling Theory in Accounting

Sampling methods are applied in many aspects of accounting and audit. One large application is in financial statement auditing. External auditors use samples to check the accuracy of revenue reports, expense accounts, payroll entries, inventory counts, and bank reconciliations.

Internal auditors use sampling to look at company operations and internal control systems. They review certain transactions which in turn help to identify weaknesses and put forth improvement recommendations.

Inventory audit is also a key function. We see that very large companies house thousands of inventory items which in turn make full physical count a challenge. Sampling in this case allows accountants to audit chosen inventory items and at the same time determine the accuracy of the total inventory records. Sampling in the area of accounts receivable is also a common practice. We see that auditors look at certain customer accounts to determine balance accuracy and to identify which may be in question.

Taxing authorities at times use sampling methods in tax investigations. Fraud experts use sampling to identify out of the ordinary actions like duplicate payments, unauthorized transactions, and false invoices.

Also in many organizations which are home to accounting departments it is through the process of sampling they which use to determine the effectiveness of computerized accounting systems and financial reporting procedures.

Benefits from Sampling Theory in Business Decision Making

Sampling theory in accounting statistics outperforms in the case of businesses and financial institutions. One big pro is that which we see in speedier reports. Also there is the option for companies to study representative samples as opposed to full sets. We also see that reports come out much quicker. What I also want to put out there is the fact that at a large scale we still have fast reporting and that is a result of using representative rather that total populations.

Sampling also improves resource allocation. Auditors and accountants may direct their resources to high risk areas which in turn may reduce the time spent on less risky transactions. Another key benefit is improved decision making. Through proper sampling techniques businesses are able to identify financial trends, operational inefficiencies, and also what may become risks.

Sampling also supports in strategic planning which in turn helps management to evaluate financial performance and forecast future business conditions. Also we see that which is put in place for reliable sampling practices improves corporate governance and also increases stakeholder confidence in financial reporting.

Limitations of Sampling Theory

Though there are many benefits to it, sampling theory also has drawbacks. One issue is that of sampling error. We only look at a section of the population which may not truly reflect the whole. Human preconceptions may also play a role in results which is especially true for non-probability sampling.

Another issue is that of complex statistics. Some sampling theory in accounting statistics require in depth stats knowledge and special software. Organizations can also become too reliant on sampling which in turn causes them to ignore important transactions that are outside of the selected sample. In some cases it is not appropriate to sample at all. For instance when fraud risk is very high auditors may have to review each transaction in detail.

Technology and Modern Sampling Practices

Technology has greatly enhanced the accuracy of sampling in audit. Today’s audit software is able to put together random samples from large financial databases in seconds. We see an increase in efficiency and reduction of human error. Data analysis tools for auditors which present to them out of the ordinary patterns, trends, and anomalies in financial reports.

Artificial intelligence is a growing element in which we see improved sample selection and more accurate detection of fraud. Some organizations are using real time audit systems which report on financial transactions all year round. These tech improvements speed up, increase reliability of, and improve the effectiveness of modern accounting practices.

Ethical Considerations in Sampling

Ethics play a very large role in accounting and audit. Auditors should see to it that they choose which samples to look at in a fair an objective manner also they should report the results truthfully not engaging in the manipulation of evidence. Professional integrity is a must as investors, regulators, creditors, and the public count on precise financial reports.

Untrue financial reports which are a result of unethical sampling methods may cause legal action, damaged image for the company, and we see loss of stakeholder confidence. Accountants and auditors must adhere to professional standards which also includes maintaining independence in the sampling process.

The Future of Sampling in Accounting

As companies produce ever greater sets of financial information, the role of sampling theory will still be very important in accounting and auditing. In the future we will see more of artificial intelligence, predictive analytics, automated auditing systems, and advanced fraud detection technologies.

Real time financial monitoring tools also will see growth which in turn will allow companies to evaluate transaction sets constantly instead of at set times. Although tech is ever changing, the fundamental tenets of sampling theory will still play a key role in sound financial analysis and business decision making.

Conclusion

Sampling theory in accounting statistics also is at the core of what accountants and auditors do. It allows them to study large sets of financial data which they wouldn’t be able to otherwise examine in detail.

Through the use of specific samples professionals are able to identify errors, assess risk, detect fraud, evaluate internal controls, and support reliable financial reporting. Elementary principles of sampling allow organizations to save time, reduce costs, and improve decision making which in turn maintains acceptable levels of accuracy. As we see financial systems becoming more complex and integrated with technology, we still have to count on sampling for use in accounting statistics and modern auditing practices.

Get more well researched information about sampling theory in accounting statistics here.