Introduction

Income Determination and Capital Maintenance is one of the key concepts of accounting as well as economics, and each science takes a different approach to it. Whereas accounting involves more organized and standardized approaches to the measurement of profit, economics involves wider definitions of income in terms of the increase or decline of wealth and utility. It is this varying opinion that influences the manner in which organizations are gauging performance, the manner in which financial statements are prepared and how sustainability is enhanced in the long run.

The core of this discussion is the accounting concepts, which give the basis of recognizing, measuring, and reporting income. But the economic interpretations criticize some of these conventions, by proposing alternative interpretations of profit and capital. This paper discusses the theory of income determination and capital maintenance with references to accounting and economic approach, whereas the concepts of capital maintenance (financial and physical) and its effects on profit measurement are also discussed.

Understanding Income Determination

Income determination can be defined as the process of quantification of the amount of profit realized by a given entity during a given period. It is vital to the stakeholders who are investors, managers, regulators and creditors because it informs the decision-making and performance assessment.

Accounting Perspective on Income

Accounting wise, the income is usually characterized as the surplus of revenues to expenses in a period of time. Such a way is informed by set principles and standards, which make it consistent and comparable across organizations.

The main characteristics of accounting income are:

- Realization principle: Revenue is recorded when it is due and it does not always happen when money is obtained.

- Principle of matching: The expenses are paired with revenues they contribute to the formation of.

- Historical cost basis: The assets and liabilities are accumulated at the initial transaction values.

- Periodicity assumption: It is based on the measurement of income over definite reporting periods i.e. quarterly or annually.

These principles render accounting income realistic and verifiable, which is not necessarily always the actual economy of an organization in financial position.

The Economic Perspective on Income

Conversely, economics describes income in a broader sense since it is the growth of the wealth of an entity over some time. This entails realized gains (i.e. sales revenue) and unrealized gains (i.e. rises in the values of assets).

Economic income may be given as:

Income=Change in net worth + Consumption

Based on this definition, there are some differences with accounting income:

- It has unrealized gains and losses.

- It emphasizes on the present value and does not look at historical prices.

- It focuses on total wealth changes but not only transactions.

Although economic income offers a bigger picture of the financial performance, it is usually hard to quantify accurately because of valuation problem and uncertainty in the market.

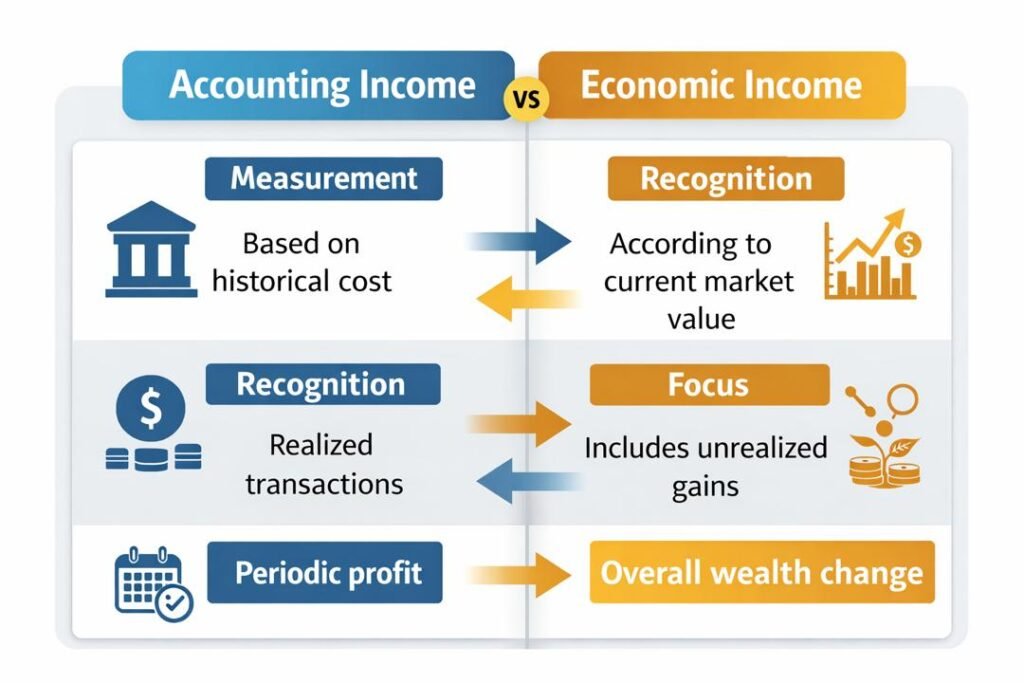

Comparison of Accounting and Economic Income

The disparities between the accounting and the economic income can be explained as follows:

| Basis | Accounting Income | Economic Income |

| Measurement | Based on historical cost | According to the existing market value |

| Recognition | Realized transactions | Incorporates unrealized gains/losses |

| Objective | Reliability and consistency | Relevance and completeness |

| Focus | Periodic performance | Overall wealth change |

Financial reporting is better using the accounting income as the information is objective and verifiable. Nevertheless, the economic income is usually believed to be more applicable to the process of making the decision because it can reflect the actual financial state of a company.

The Role of Accounting Concepts in Income Determination

The ideas of accounting are the basis of calculating the income in structured and standard ways. These ideas can guarantee the preparation of financial statements and make them interpretable by the users.

To delve deeper into these underlying principles, you may use this elaborate guide on accounting concepts, which tells us how they influence financial reporting and income measurement.

The following are some of the accounting concepts that have an impact on the determination of income:

- Accrual concept: Recognition of income: income is recognized at the time it is earned and not at the time it is received.

- Going concern concept: Assumes that the business will be operating and impacts on the valuation of assets and recognition of income.

- Concept of consistency: This will guarantee that the accounting methodology is consistent over time.

- Prudence concept: It advises against overstatements of profits by making sure that income and expenses are recognized.

Reliability and comparability are the primary concepts of these concepts, although in some instances, they can restrict the applicability of financial information.

The Concepts of Capital Maintenance

Capital maintenance is also strongly associated with determination of income because profit cannot be recognized until the capital of the business is maintained. There are two major methods: financial capital maintenance and physical capital maintenance.

Financial capital Maintenance

Maintenance of financial capital is aimed at the conservation of the monetary worth of the net assets of an entity. Following this concept, profit is not admitted until the end of a period, the financial capital is more than the capital of the start of a period.

Key Features

- Capital is determined in monetary units.

- Profit is the growth of net assets, without the contributions and distributions of the owners.

- It is either measured in nominal (without considering inflation) or real (with inflation).

Implications

- Simple to use in conventional accounting systems.

- Financial reporting and regulatory-suitable.

- May over-profits when inflation is occurring when adjustments are not made.

Maintenance of Physical Capital

Physical capital maintenance or operating capability maintenance lays emphasis on the ability of the business to maintain its physical capacity to produce goods or services.

Key Features

- The measurement of capital is in productive capacity, and not in monetary value.

- Profit is only realized when it is able to sustain the entity on the same level.

- Needs modifications on the changes of the cost of replacing assets.

Implications

- Gives a more realistic sustainable profit.

- Takes into consideration the effect of inflation on replacement of assets.

- More complicated and not easily applied to practice.

Comparison of Financial and Physical of Capital Maintenance

| Aspect | Financial Maintenance of Capitals | Physical Capital Maintenance |

| Focus | Monetary value | Productive capacity |

| Profit Recognition | Increase in net assets | Increase after maintaining capacity |

| Inflation Impact | May distort profit | Adjusts for inflation |

| Complexity | Simpler | More complex |

The reason why financial capital maintenance is widely applied is because it is very simple, whereas physical capital maintenance is a better depiction of long-term sustainability.

Profit Measurement Implications

The decision to adopt the accounting or the economic approach, the decision to adopt the financial capital maintenance or the physical capital maintenance also tremendously influences the measure of profit.

Under Accounting Perspective

- Profit is calculated on the basis of realized transactions.

- They put an emphasis on objectivity and consistency.

- May not represent true economic value.

Under Economic Perspective

- Profit entails unrealized gains and losses.

- Gives mirror image of today’s market.

- Takes a broader perspective of performance.

Under Financial Capital Maintenance

- The profit can be overstated when there is inflation.

- Concentration is on financial stability.

Under Maintenance of Physical Capital

- The sustainable earnings are reflected in profit.

- Ensures that business is able to sustain operations.

Impact Financial statement

Various theoretical views have an impact on the preparation and interpretation of financial statements.

Income Statement

- Accounting method demonstrates realized incomes.

- Economic approach would consist of the adjustment in asset values.

Balance Sheet

- History cost is used in accounting.

- Economic school of thought prefers current value.

Changes in Equity Statement

- Captures maintenance of capital adjustments.

- Reports whether profit has been made after capital preservation.

Such variances may contribute to performance variation in the reported performance, which impacts on the decision making of the stakeholders.

Performance Evaluation

Income determination is essential in determining performance of an organization.

Accounting-Based Evaluation

- Concentrates on profitability ratios (e.g. net profit margin).

- Values consistency, comparability.

- External reporting suitable.

Economic-Based Evaluation

- Considers wealth creation.

- Takes into account value-based measures.

- Helpful in making internal decisions.

One of the most effective methods of providing a more balanced evaluation of performance is a mixture of the two approaches.

Long-Term Sustainability

Since the business aims at making money, sustainability hinges on the capacity of the business to sustain its capital.

Role of Capital Maintenance

- Makes sure that profit is not given away to the detriment of capital.

- Facilitates round the clock operations.

- Secures interests of the stakeholders.

Accounting vs. Economic Perspectives

- Accounting methodology guarantees stability and reliability.

- Economic approach encourages effective distribution of resources.

Maintenance and Sustainability of Physical Capitals

Maintenance of physical capital is particularly critical towards being sustainable at a long term as it guarantees the business of being in a position to operate at its current capacity regardless of inflation and the change of economic conditions.

Integrating the Perspectives to make better decisions

Practically, neither a financial perspective nor a financial accounting is enough. The combination of the two approaches is common in organizations so as to have a more holistic view of income and performance.

Benefits of Integration

- Integrates relevancy and reliability.

- Improves the quality of decision-making.

- Takes a long-term perspective to financial health.

Practical Applications

- Financial reporting using accounting income.

- Strategic planning on economic income.

- Adjustment to inflation where required to make sure that profits are measured correctly.

Conclusion

Determining income is not an easy task that can be viewed through the prism of accounting and economy. Whereas accounting will offer a more reliable and organized system of measuring the profit, economic interpretations will offer a wider and more pertinent perspective of financial performance.

The concepts of capital maintenance also enhance the concept of profit, whereby the income is only determined after the capital of the business is maintained. Financial capital maintenance is monetary value oriented and physical capital maintenance is operationally oriented and long term sustainability-oriented.

Finally, financial statements, performance analysis, and sustainability are concerned with the way one chooses perspective and capital maintenance strategy. Having a combination of Income determination and capital maintenance knowledge enables organizations to arrive at a more precise and significant evaluation of their financial outcomes to make superior decisions and succeed in the long term.

Get more well researched information about the Income Determination and Capital Maintenance here.