Introduction

One of the most important aspects of the academic and professional field, accounting is no exception. It provides the conceptualization of research educates practice and has an impact on innovation. Theory is not just a mere abstraction in accounting since it does have implications in the development of the financial information, interpretation and use in practice. Inductive vs deductive approaches in accounting are the two major approaches that prevail in the development of theories.

Hypotheses and analysis are used in deductive reasoning to test theories whereas in inductive reasoning, analysis and observations are used to construct the theories. The inductive vs deductive approaches in accounting have played very critical roles in building and practice of accounting in history. But the question is how to answer it – which approach to accounting innovation do either of them more likely instigate?

The article is a critical reflection of the two theory development approaches inductive and deductive, which explains their process, power, and weaknesses. It also addresses how these methods may result in accounting innovation, research methods and evidence-based practice.

Understanding Inductive and Deductive Approaches

Inductive Approach to Theory Development

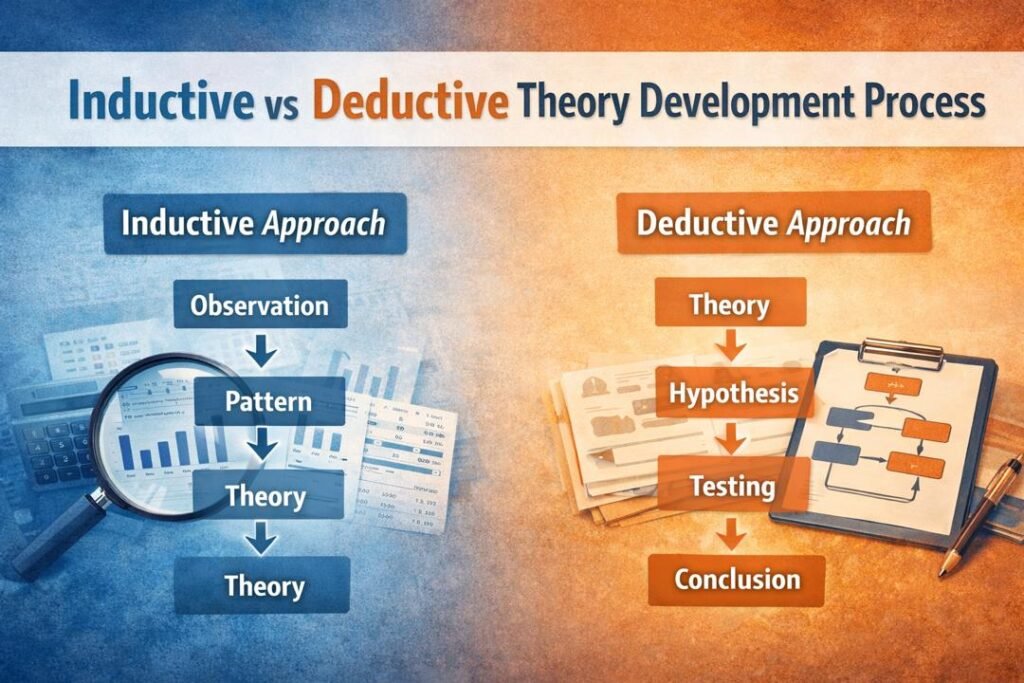

Inductive approach begins with observation. The information scientists extract in the field of study is then modeled and an overall theory developed. It is a transition between certain instances to generalizations.

Intuition in reasoning is a usual phenomenon in accounting due to the practical experiences. Accountants can observe typical financial reporting activities in firms and use the results to develop novel principles or models, indicatively.

The following process usually involves inductive reasoning:

- Studying real world phenomena.

- Identification of trends or patterns.

- Creating the tentative hypotheses.

- Generalization of theories.

Induction is an exploratory process. It comes in particularly handy when you lack enough existing theories or when there are certain new financial practices being practiced and need to be clarified.

Deductive Approach to Theory Development

This is the case with the deductive approach. It starts with a theory or general rule which already exists and then disputes it with the assistance of certain observations. The researcher formulates hypotheses on the basis of the theory and presents them to empirical data in order to either disprove or prove them.

Deductive reasoning is quite a popular way of carrying out empirical studies in the area of accounting. Here is one example, a researcher can start with a theory that describes the reaction of companies to regulatory change and use financial information to test the theory.

Its deductive process usually involves:

- Hypothesis Established theory Identification.

- Formulating hypotheses

- Collecting evidence to prove the hypotheses wrong.

- Accepting or rejecting the theory.

Deduction is arranged and organized. It is centered on rational coherence and is usually connected with quantitative types of research.

Key Differences between Induction and Deduction Approaches

Although both methods are concerned with the development and enhancement of theories, there is a major difference between the orientation and implementation.

| Aspect | Inductive Approach | Deductive Approach |

| Direction | Specific to general | General to specific |

| Starting Point | Observations | Theory |

| Nature | Exploratory | Confirmatory |

| Methodology | Qualitative, flexible | Quantitative, structured |

| Outcome | New theory development | Theory testing |

The differences bring out the fact that inductive and deductive approaches cannot be treated as mutually exclusive. In fact, they are complementary to one another in the overall knowledge production.

Strengths of the Inductive Approach

1. Promotes Discovery and Innovation

Inductive reasoning is one that is especially helpful in the creation of new ideas. This is due to the fact that it is based on observations in the real world and hence enables the researcher to bring to light patterns that might not be captured by the current theories.

This is very vital in accounting in order to innovate. With the change in the financial environment because of the globalization, new technologies, and change in regulations, new accounting practices arise and call new theoretical foundations.

2. Reflects Practices in the Real World

Actual accounting practices are closely related to inductive theories. This renders them very applicable and viable. They can absorb the intricacies and subtleties of financial behavior that can be missed by pure theory.

3. Flexibility

The inductive method is flexible. This makes it appropriate in answering an emerging problem like sustainability reporting or digital accounting systems because researchers are able to change their course of action as new information arises.

Limitations of the Inductive Approach

1. Lack of Generalizability

A major drawback of induction is that the results of a given observation cannot be generalized. This may restrict the generalizability of the theories produced.

2. Risk of Bias

Since inductive reasoning is very dependent on observations, it may be affected by bias of the researcher. Misinterpretation of information will result in inaccurate conclusions.

3. Time-Consuming

Gathering and assessing an enormous volume of data to determine patterns may be time consuming, particularly in complicated accounting settings.

Strengths of the Deductive Approach

1. Logical Consistency

The deductive reasoning is used to make sure that the conclusions drawn are based on a theory that is established. This augments the reliability and credibility of the research results.

2. Facilitating Testing and validation

Deduction enables the researcher to test theories rigorously based on the empirical data. This is necessary in the refinement of the existing accounting structures and their accuracy.

3. Efficiency

Due to its initial solid theoretical framework, the deductive method is usually more organized and effective than induction. Scientists are able to directly test particular hypotheses.

Limitations of the Deductive Approach

1. Reliance on Current Theories

Deductive reasoning is based on the correctness of current theories. When the theory behind it is wrong, the inferences made on it might also be wrong.

2. Limited Innovation

Due to the testing aspect of deduction as opposed to discovery, deduction might not give rise to completely new ideas. This may inhibit its innovation as a driver.

3. Rigidity

Flexibility can be constrained by the tendency of deduction. Scientists can fail to notice unforeseen results due to their preoccupation with the testing of pre-determined hypotheses.

Inductive and Deductive Approaches in Accounting Research

In many studies of accounting, an inductive approach is combined with a deductive approach.

- Qualitative studies that involve inductive research are usually applied in case studies and interviews where scholars investigate the manner in which accounting practice develops within real-life settings.

- Quantitative studies are mainly deductive in nature, and they involve the application of statistical tests to prove hypothesis regarding financial behavior.

As an illustration, an investigator into the topic of corporate reporting may initially rely on inductive approaches to discern the new trends in sustainability reports. Thereafter, they could use deductive approaches to test hypotheses on the effect of such disclosures on investor decision-making.

Such combination shows that the two methodologies are not competitors but they are complementary in developing theories.

The Role of Inductive and Deductive Approaches in Accounting Innovation

Accounting innovation is a new process, practice, and technology that enhance the usefulness, transparency, and efficiency of financial information. Inductive and deductive methods play a part in the process in their own way.

Looking to learn more about the current developments in modern practices? Visit this contentious debate on the definition of accounting innovation and its theoretical basis.

Inductive Approach and Accounting Innovation

One of the forces of innovation in accounting is inductive reasoning. Through changes in the real world, research and practitioners can find new challenges and opportunities.

For instance:

- The trend of using the digital accounting system has resulted in the emergence of the new approaches to the financial reporting.

- Environmental accounting practices have emerged as a result of the issues of sustainability.

With these innovations, observation is frequently the starting point in place of theory. Through inductive reasoning, the accounting experts are able to react to the emerging trends and create new models which are responsive to the prevailing realities.

Deductive Approach and Accounting Innovation

Induction provides birth to new ideas whereas deduction is instrumental in validating and refining the ideas.

After creating a new accounting practice, deductive reasoning is employed in order to:

- Test its effectiveness

- Consider its effect on the financial report.

- Adhere to the regulatory standards.

This makes innovations creative, as well as reliable and consistent.

Innovation in Accounting, Methodologies of Research, and Evidence-Based Practice

Accounting Innovation and Theory Development

Theory development is closely related to accounting innovation. The new practices may not be credible and consistent without a solid theoretical basis.

Roles in Research Methodology

Inductive and deductive research methods are frequently used together in accounting:

- Inductive reasoning is supported by qualitative methods (e.g. interviews, case studies) that would reveal detailed and rich understanding of accounting practices.

- Deductive reasoning is assisted by quantitative methods (e.g., statistical analysis) in order to test hypotheses and prove theories.

This combination enables the researcher not only to investigate new concepts but also to prove their correctness.

Evidence-Based Practice in Accounting

Evidence-based practice refers to the act of basing decisions on factual data as opposed to generalized or traditional information. This process is done by both inductive and deductive methods:

- Induction gives the first-time evidence through determining the patterns and trends.

- Deduction tests confirm and prove this evidence making it reliable.

As an example, a new accounting method can be built on the practices that have been observed (induction) and then tested on various organizations to ensure that it is an effective one (deduction).

Which Strategy Drives Accounting Innovation?

Whether inductive or deductive are the approaches that lead to accounting innovation, the question does not have a simple answer. The two are all important, although their roles vary.

Induction as the Major Engine of Innovation

Innovation can have a starting point in inductive reasoning. It allows one to find new thoughts by concentrating on observable phenomena. A number of accounting innovations would not arise without induction.

The Refining Force of Deduction

Deductive reasoning will prove to be effective in ensuring that innovations are tested, proved and improved. It converts the creative concepts into trustworthy practices that are capable of mass adoption.

Complementary Relationship

Inductive and deductive methods do not compete, but are involved in an endless cycle:

- Theory is the result of observation (induction)

- Theory results in testing (deduction)

- Testing creates testing and observation.

This is a cycle of needed accounting innovation.

Conclusion

Inductive vs deductive approaches in accounting play an important role in the development of theory. Induction encourages creativity and discovery through the construction of theories based on observation of the real world whereas deduction guarantees rigor and reliability through testing these theories through organized analysis.

Inductive reasoning is the main source of new ideas in the context of accounting innovation, and deductive reasoning is the one that gives the required validation and refinement. The combination develops a dynamic and iterative process, which spurs the development of accounting practices.

Finally, there is no better way to develop theory, and to innovate, than to combine induction and deduction. Through a combination of both the exploratory and confirmatory approaches, the accounting scientists and practitioners can come up with theories that are novel and strong enough to guarantee that the field keeps on adapting to the dynamic financial landscape.

Get more well researched information about Inductive vs Deductive Approaches in Accounting here.