Introduction

As a discipline and profession, accounting has been based a lot on theory underpinning its practices, interpretations, and innovations. These levels of theory in accounting do not all belong to the same level, but instead are found in a stratified or hierarchical structure, which indicates different levels of abstraction and the extent to which they can be used. This multi-layered approach is critical in understanding the way in which accounting knowledge is constructed, experimented and implemented in the real world.

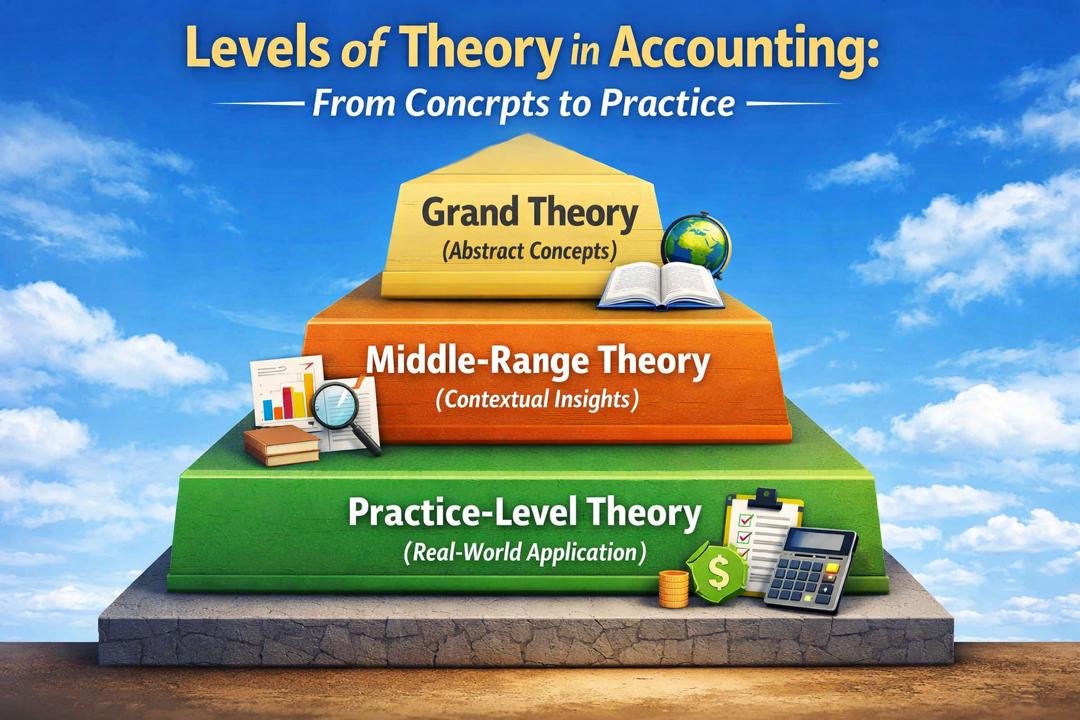

Central to this discussion is the hierarchical structure of the levels of theory in accounting that classifies theories into three main levels; a grand theory, middle range theories, and practice level theories. All levels contribute towards accounting research and practice in a unique but linked way. Although the grand theories offer generalized concepts, the middle-range theories are more specific and particularized on the concepts, whereas practice-level theories transform the concepts into practical standards to be applied in day-to-day activities.

This article discusses these levels of theory in accounting in detail, their nature, purpose and interaction process. It also shows how this chain of command is improving not only the intellectual investigation but also the practical decision-making, making accounting a vibrant and a relevant profession.

Understanding the Hierarchical Structure of Theories

Hierarchical structure of theories actually means that theoretical knowledge can be organized according to its level of abstraction, scope and viability. This is not a specific structure to the field of accounting; this is a familiar structure in numerous fields, such as sociology, economics and management. In the case of accounting, however, it is especially important because of the dual character of the discipline as a science and as a profession.

Three principal levels make up the hierarchy:

- Grand Theories: Extremely abstract and broad based.

- Middle-range Theories: Situation and level-specific.

- Practice-Level Theories – Direct and practical.

All levels have a specific purpose, yet they are linked in such a way that they enable the circulation of knowledge between abstract ideas and real-world uses and vice versa via feedback and improvement.

Grand Theories in Accounting

Definition and Characteristics

The highest and most abstract levels of the hierarchy are the grand theories. Their goal is to offer a general conceptual approach to the whole accounting. These theories are not specific to any particular practice or situation, rather, they are concerned with basic principles, assumptions and philosophical underpinnings.

Important features of grand theories are

- High level of abstraction

- Widespread applicability.

- Pay attention to the basic concepts.

- Minimal relevance to practice.

Examples in Accounting

Grand theories in the accounting field are commonly conceptual theories or normative theories. As an example, the theories which constitute the objectives of financial reporting like the provision of useful information to the stakeholders are in this category. Equally, conceptual frameworks by the usual setting bodies work to set the principles of accounting practices.

The questions that these theories answer include:

- What is accounting?

- Who are the key consumers of financial information?

- What are the useful qualities of information?

Role in Accounting Research and Practice

Grand theories are those theories on which all the other levels of theory are based. They inform the standards development process, impact the policy-making process, and affect the direction of academic research.

But because they are abstract they cannot be applied directly to day to day accounting operations. Instead, they give a philosophical and conceptual prism out of which more particular theories can be crafted.

Middle-Range Theories in Accounting

Definition and Characteristics

Middle-range theories are those between the grand theories and practice level theories. They are abstract rather than practice-level theories, but less abstract than grand theories. These theories specialize in some areas of accounting and seek to describe relationships or phenomena in a given context.

The main features are:

- With average abstraction.

- Context-specific focus

- Empirical testability

- More relevance to real life situations.

Examples in Accounting

Middle-range accounting theories tend to be the result of empirical studies. Examples include:

- Theory of positive accounting: A theory of accounting explaining and predicting practices.

- Agency theory: The study of the relationship between agents and principals.

- Earnings management theories: Theories that examine the manipulation of financial reports by managers.

These theories answer such questions as:

- Why do companies adopt particular accounting practices?

- What is the effect of incentives on financial reporting behavior?

- How does it relate to the reliability of financial information?

Role in Bridging Theory and Practice

Middle-range theories are very important in closing the gap between theories and practice. They generalize the general formulations of grand theories and use them in particular contexts to make them more useful and refutable.

Giving a case in point, a grand theory may provide insight into the significance of transparency in financial reporting, whereas a middle-range theory would examine the effects of the transparency on corporate governance structures or regulatory settings.

The level of theory is especially useful to researchers, because they can develop hypotheses that can be empirically tested. It also gives enlightenment to practitioners on the factors which affect the accounting results.

Practical Level Theories in Accounting

Definition and Characteristics

The most practical level in the hierarchy is the practice-level theories. They concentrate on certain processes, methods and rules applied in daily accounting activities.

The important features are:

- Low level of abstraction

- High degree of specificity

- The immediate relevance to practice.

- Frequently written in regulations and standards.

Examples in Accounting

Accounting standards, policies, and procedures reflect practice-level theories. Examples include:

- Revenue recognition guidelines.

- Methods and calculation of depreciation.

- Ways of valuing inventory.

- Auditing procedures

The theories answer such practical questions as:

- In which transaction should revenue be recognized?

- How should an asset be depreciated?

- The preparation and presentation of financial statements?

Role in Professional Practice

The accounting profession cannot work without practice level theories. They also give structured and practical direction or advice that would guarantee uniformity, dependability, and similarity in financial reporting.

Accountants, auditors and financial analysts apply these theories directly in their daily work. Practice-level theories are operational and task-oriented in contrast to grand and middle-range theories, which are more conceptual.

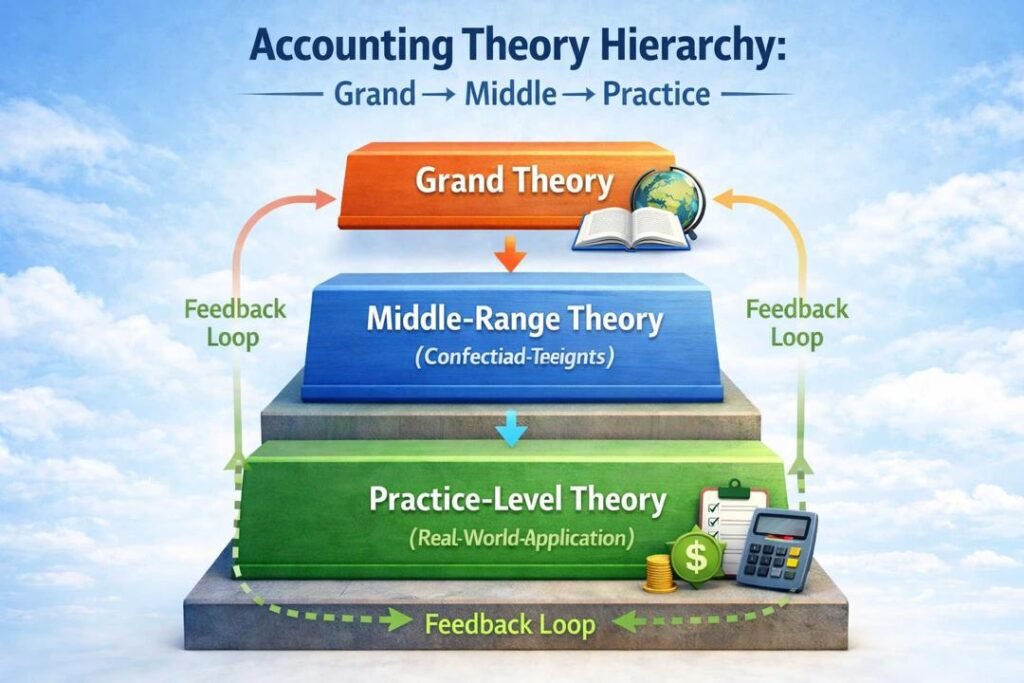

Interactions between the Three Levels

Top-Down Influence

The three levels of theory are not connected in a linear way and are dynamic and interdependent. Among the important elements of this interaction, there is the top-down impact of grand theories on the practice-level theories.

Grand theories form the basic principles which help in developing middle range theories. In their turn, middle-range theories narrow down these principles and transform them into more practice-specific frameworks, which, in their turn, are later used as informants of practice-level theories.

For example:

- A grand theory focuses on the role of faithful reporting of financial reporting.

- A middle-range theory is a study that investigates the relationship between managerial incentives and reporting accuracy.

- A practice level theory sets up certain guidelines on how financial transactions are to be identified and quantified.

Bottom-Up Feedback

The reciprocal effect is also involved. Middle-range and grand theories can be refined or changed based on the practice-level experiences and empirical data.

An example is when practitioners are faced with challenges or inconsistencies in the implementation of some of the standards, researchers might explore such problems, and as a result, generate new middle-range theories. These observations could eventually affect the development of the grand theories.

Continuous Evolution

The two-way communication is a way of ensuring that accounting theories are pertinent and receptive to business environment changes. It also encourages the aspect of learning and enhancement in the discipline.

Relevance to Accounting Research

Enhancing Theoretical Development

The systematic method of theory construction and organization of knowledge on accounting research is offered by the hierarchical structure of theories. It allows researchers to:

- Determine loopholes in the current theories.

- Develop new hypotheses

- Test the relationships through empirical data.

Knowing the various degrees of theory, the researchers may place their work at the right place and improve the discipline.

Promoting Interdisciplinary Research

The middle-range theories in specific are the ones that help interdisciplinary research by means of integrating the ideas of economies, psychology as well as sociology. This makes accounting research rich and offers a more detailed picture of financial phenomena.

Improving Research Relevance

The theory and practice interplay make the research to be relevant to the real world problems. Using experience at the practice level, the researcher is able to come up with theories that deal with the practical issues and aid in better decision-making.

Relevance to Professional Practice

Guiding Decision-Making

The hierarchical nature of theories can assist practitioners in making informed decisions because it gives them a clear guide on how to comprehend accounting principles and practices.

- Grand theories provide theoretical support.

- Middle-range theories offer context-focused information.

- Practice-level theories provide practical advice.

Ensuring Reliability and Consistency

Higher-level frameworks that underpin practice-level theories would bring consistency and reliability in financial reporting. This is vital in keeping the stakeholders with trust and confidence.

Adapting to Change

The active relationship between the levels of theory makes the accounting profession to keep abreast with the changes in the business environment. The theories can be modified and brought up to date to deal with emerging issues as new challenges come about.

Challenges and Limitations

The hierarchical nature of the theories in accounting is not without its problems despite the benefits it has.

1. Complexity

Multi-level structure of the hierarchy may make it hard to learn the relationship between the various theories that the practitioners have to understand. This can result in lack of linkage between theory and practice.

2. Rigidity

In other instances, practice-level theories can be inflexible because of the requirements by the regulations, which restrict their capability to adapt. This may be disruptive to innovation and responsiveness.

3. Gaps between Levels

The levels of theory may also contain gaps between them especially where the middle-range theories are not instrumental in bridging the gap between the abstract and the practical.

Conclusion

The levels of theory in accounting offers a whole picture on how knowledge is formulated, structured and put into practice in the field. This structure recognizes the roles and contributions of each level by setting a difference between the grand theories, middle-range theories, and the practice-level theories.

Grand theories provide general conceptual basis, middle range theories give context specific information and practice level theories translate the concepts to practical guidelines. They provide an integrated system that promotes academic research and professional practice.

The interplay between these levels makes accounting an active and a developing profession, and it can solve complex financial problems and adapt to new conditions. Through the importance and use of this hierarchy, accountants are able to improve the quality, relevance, and impact of their work through its appreciation.

Finally, it is the power of accounting as a profession to combine theory and practice in such a hierarchical system, so that the abstract concepts are supported by the reality, and the practical activities are addressed by the sound theory.

Get more well researched information about Levels of Theory in Accounting here.