Introduction

The study of dogmas and grounded theory in accounting research is the intellectual support, which determines the way in which knowledge is developed, interpreted and applied. They offer paradigms of financial phenomena, both in scholarly investigation and in practice. Not all theories are however made and used in the same manner. Some of them are based on the ancient beliefs and the principles and others come directly out of the observed data and the real-life experience.

Two opposite methodologies that emphasize this distinction are the dogmatic theories and the grounded theory. Dogmatic approaches are based on preconceptions and accepted standards and usually in favor of consistency and tradition. Conversely, grounded theory develops out of empirical information inductively, with flexibility and context as its priorities.

This article will discuss the conceptual essence of dogmas and grounded theory in accounting research , including philosophical underpinning, implication of their methodology, and how this has impacted research in accounting. It also shows how each strategy is relevant to the creation of contextual financial structures, which are needed to deal with the sophistication of contemporary financial settings.

Understanding Theory of Accounting

A theory is a generalized body of ideas that aims at explaining, predicting or controlling behavior in a given area. Theories in accounting assist in the explanation of financial information generation, reporting and interpretation. They also give the basis to setting of standards, policy formulation, and decision-making.

There are two major types of accounting theories:

- Normative theories prescribe what should be done in accounting practices.

- Positive theories, explaining and predicting real accounting practice.

Under this larger category, there exist dogmatic and grounded theory in accounting research as two different methods of constructing and implementing theory. Although the two strive to increase the level of understanding, they are radically different in their approach of philosophical orientation and the way they are carried out.

The Nature of Dogmatic Approaches to Accounting

Definition and Characteristics

Dogmatic approaches have a foundation on previously held beliefs, principles or dogmas that are considered authoritative without being subject to constant empirical proof. These modes are usually based on tradition, consensus or regulatory frameworks.

The main peculiarities of dogmatic theories are:

- Dependence on accepted standards: They are very much dependent on historically accepted accounting standards.

- Top-down structure: Theories are created, and subsequently, they are applied to practice.

- Resistance to change: Dogmatic systems are very slow to change and it may take a lot to justify change.

- Standardization: They encourage uniformity and totality in financial reporting.

Philosophical Foundations

Dogmatic methods are based on deductive reasoning structure, in which general principles are applied to come up with particular applications. This is in line with normative thinking, where the focus is on how to teach the ideal accounting practices as opposed to describing how behavior is actually being.

As an illustration, old accounting principles like the historical cost principle have always been dogmas even in the cases when they did not entirely represent economic reality.

Role in Accounting Research

Dogmatic theories are important in:

- Standard-setting: The regulators tend to stick to the set of principles in order to remain consistent.

- Policy making: These theories are applied by governments and other institutions to establish stable financial systems.

- Professional practice: Accountants rely on standardized rules to make sure that there is compliance or comparability.

Nonetheless, dogmatic approaches can be too rigid to adjust to new economic realities, new technology, and different business settings.

Limitations of Dogmatic Approaches

Irrespective of their merits, dogmatic theories have a number of limitations:

- Lack of empirical grounding: It can be inaccurate because they are not necessarily grounded on the existing data.

- Inflexibility: Dogmatic systems may not be able to adjust to fast changing financial landscape, including digital currencies or globalized markets.

- Context insensitivity: Such solutions tend to take the applicability of uniformity without taking into consideration cultural, economic, and institutional variations.

- Risk of obsolescence: In the long term, the accounting practice will diminish in relevance due to the stay of outdated principles.

These restrictions have prompted scholars to search more active and data-driven methods like grounded theory.

Grounded Theory: Data Intensive Approach

Definition and Major Principles

A grounded theory is an inductive research approach, which formulates theories using a data that is gathered and examined systematically. It is not premised on fixed assumptions as is the case with dogmatic approaches. Rather, it lets patterns, relationships, and concepts to develop naturally out of the data.

The major tenets of grounded theory are:

- Inductive reasoning: Theory is reasoned and not forced.

- Constant comparison: Information is constantly being compared in order to find patterns and narrow concepts.

- Theoretical sampling: new knowledge is used to guide the data collection.

- Flexibility: The process of research will change as new discoveries develop.

Philosophical Foundations

Grounded theory is based on the interpretivism which focuses on explaining social phenomena based on the views of the involved people. In accounting, this refers to the study of the influence of organizational behavior, cultural situations and economic environments on financial practices.

This style is quite similar to the positive accounting theory because it aims to describe and explain real practices as opposed to defining the ideal practices.

Application of Grounded Theory in Accounting Research

The concept of grounded theory has gained significance in accounting studies especially where the conventional theories lack. Its applications include:

1. Understanding Organizational Practice

Grounded theory assists researchers in determining the implementation of accounting systems in organizations and gives them some understanding that might be missed by standardized models.

2. Exploring Behavioral Dimensions

It assists in the analysis of how financial information is viewed and applied by managers, auditors and the stakeholders in decision making.

3. Investigating New Developments

New developments, which include fintech, sustainability reporting, and digital accounting systems, are also being useful in the grounded theory.

4. Formulating Context-Specific Insights

Grounded theory allows developing custom accounting solutions by using the data on the ground, which corresponds to a particular environment.

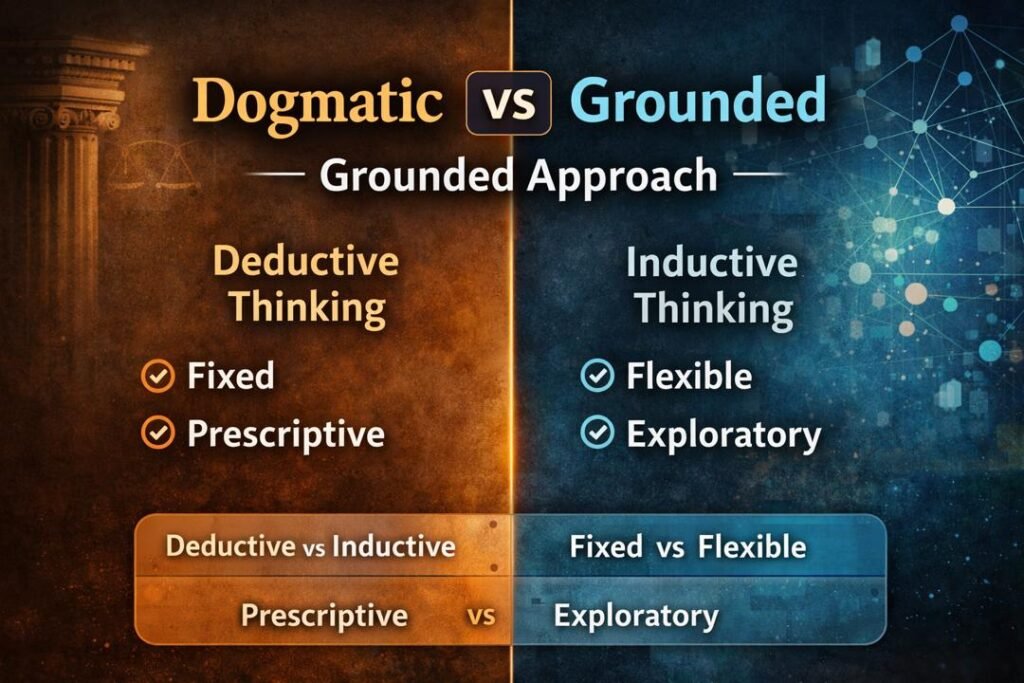

Dogmatic and Grounded Approaches, Comparison

Methodological Differences

| Aspect | Dogmatic Approach | Grounded Theory |

| Basis | Established beliefs | Empirical data |

| Reasoning | Deductive | Inductive |

| Flexibility | Low | High |

| Adaptability | Limited | Strong |

| Focus | Prescriptive | Exploratory and descriptive |

Strengths and Weaknesses

Dogmatic Strengths:

- Assures standardization and comparability.

- Gives practice guidelines.

- Promotes regulatory structures.

Dogmatic Weaknesses:

- May is irrelevant in shifting situations.

- Can suppress innovation

Grounded Theory Strengths:

- Representative of practice.

- Promotes creativity and flexibility.

- Grabs some of the context.

Grounded Theory Weaknesses:

- May lack generalizability

- Needs a lot of data gathering.

- Can be time-consuming

Influence on Accounting Research Design

The dogmatic or grounded selection largely determines the design of research.

Dogmatic Research Design:

- Starts with some predetermined hypothesis.

- Applies systematic techniques.

- Builds on other literature and models.

- Intends to have generalizable outcomes.

Grounded Research Design:

- Begins without a definite hypothesis.

- Works with flexible and iterative approaches.

- Pays attention to collection and analysis of data.

- Tries to produce novel theories.

These variations influence the manner in which researchers will formulate, collect and analyse problems.

Impact on Evidence Generation

Dogmatic Evidence Generation

Existing theories are usually backed up or supported by evidence. This may result in confirmation bias in which researchers favor data that conforms to preconceived notions.

Grounded Evidence Generation

Theory development is based on evidence. Scientists are not certain about the findings and new details may appear.

This difference shows the significance of methodological congruence in the credibility and relevance of research results.

Development of Context-Sensitive Financial Structures

Among the most important contributions of grounded theory, it is possible to identify the possibility to facilitate the formation of contextualized financial systems.

What Is a Context-Sensitive Financial Framework?

They are accounting systems and models, which aim to represent the peculiarities of a particular environment, such as:

- Economic conditions

- Cultural influences

- Regulatory requirements

- Organizational structures

Role of Dogmatic Approaches

Dogmatic theories will add to these frameworks as they give a steady base. They guarantee uniformity and parity between varieties of contexts, which is critical to global financial reporting.

Role of Grounded Theory

Grounded theory adds value to these frames by adding the real-life information and contextual knowledge. It enables them to:

- Localize the accounting practices.

- Address unique challenges

- Enhance the relevance of financial information.

Integrating both strategies

The best accounting systems usually incorporate aspects of the two systems. Where dogmatic principles are seen to offer a structure, grounded insights assure flexibility. The result of this integration would be stronger and responsive financial systems.

Practical Implications for Accounting Professionals

There are a couple of practical implications of understanding the difference between dogmatic and grounded approaches:

1. Improved Decision-Making

Balancing general principles with contextual knowledge will enable professionals to make more informed decisions.

2. Enhanced Reporting Quality

Including wisdom can enhance the quality and usefulness of financial statements.

3. Greater Flexibility

By adopting data-driven methods, organizations are better placed to adapt to evolving conditions.

4. Innovation in Practice

Grounded theory promotes trial and error and better accounting solutions are given.

Difficulties Balancing Both Approaches

Although these two approaches are complementary, it is difficult to incorporate both dogmatism and grounded approach:

- Conflict between standardization and adaptability.

- Inability to come to terms with conflicting results.

- Limitations in carrying out grounded research.

- Reluctance to change that exists in an existing system.

These issues need to be addressed through paradigm shift and cooperation among researchers, practitioners, and regulators.

Future Directions in the Research of Accounting

With the business environment continuing to change, the use of grounded theory is bound to be expanded. New trends like digital transformation, sustainability reporting, and global integration are becoming more context-sensitive and adaptive.

Meanwhile, the role of dogmatic principles cannot be neglected. They bring the stability on which dependable financial reporting and international comparability rely.

To solve intricate problems in the future, the field of accounting research has the potential to combine these two approaches, capitalizing on their respective advantages.

Conclusion

The discussion of the dogmas and grounded theory in accounting research methods shows that the process of constructing and applying accounting knowledge can vary in a variety of ways. Dogmatic theories are stable, consistent, and clear, and are required in terms of standard-setting and professional practice. But their rigidity may hinder their applicability in fluid environments.

Grounded theory, in its turn, gives us a more adaptable and empirical means of approaching the issues and addressing the intricacies of the real-life practices. It allows the innovation of new and context-sensitive solutions, especially context-responsive financial frameworks.

After all the best way to do accounting research is not to balance between dogma and grounded theory but to think through a balanced combination of the two. Researchers and practitioners can develop more robust, flexible and significant accounting systems by integrating long held principles and empirical results to address the needs of the rapidly changing world.

Get more well researched information about Dogmas and grounded theory in accounting research here.