Introduction

Learning the essential elements of financial statements is a basic understanding in the interpretation and the preparation of credible accounting reports. Financial statement is not just a combination of numbers, but it is organized information that is constructed on known elements, recognition requirements and measurement foundations. These factors are assets, liabilities, equity, income, and expenses that are the basis of accounting under the internationally recognized accounting standards like the framework of core elements of financial statements formulated by the International Accounting Standards Board (IASB).

This article discusses these five elements at length, how they are classified, their recognition criteria, and how they are measured. It also examines the way they relate in the accounting equation and affect the statement of financial position and the income statement.

Overview of Financial Statements Elements

The international financial reporting standards (IFRS) are the standards that govern financial reporting in the whole world and are monitored by the IASB. Financial statement elements are defined in the IFRS Conceptual Framework, which gives guidance on financial statements recognition and measurement.

They are the five main factors namely:

- Assets

- Liabilities

- Equity

- Income

- Expenses

These factors can be broken down into two major categories:

- Assets, Liabilities, Equity: statement of financial position elements.

- Income Elements: Income, Expenses.

They all create a comprehensive picture of the financial performance and financial position of an entity.

1. Assets

Definition

An asset is a current economic resource within the entity due to the occurrence of the past. An economic resource is a right which can generate economical privileges.

Key Characteristics

All items that qualify as an asset include:

- The entity controls it.

- It developed out of an earlier exchange or experience.

- It will create economic gains in the future.

Classification of Assets

The assets are normally categorized as:

Current Assets

They are supposed to be fulfilled or used up in one operating cycle or 12 months period. Examples include:

- Cash and cash equivalents

- Inventory

- Trade receivables

- Short-term investments

Non-Current Assets

These offer long term gains in the form of benefits exceeding one year. Examples include:

- Equipment, plant, and property (PPE).

- Intangible assets

- Long-term investments

- Goodwill

Recognition Criteria

An asset is recognized in the financial statements when:

- It is likely that tributes will come to the entity in the future.

- The value or price is something that can be measured.

Consider the example where a company acquires equipment and the firm identifies the asset since:

- It controls the equipment.

- The acquisition has taken place.

- The cost is measurable.

- The future benefits will be created by the equipment.

Measurement Bases for Assets

The assets can be measured on various bases:

- Historical Cost: Original cost.

- Fair Value: Fair market value.

- Value in Use: Future cash flows of anticipated cash flows.

- Current Cost: This is the amount that is needed to replace the asset.

Reported financial position and profitability are greatly influenced by the selection of a measurement base.

2. Liabilities

Definition

A liability is the current commitment of the entity to give an economic resource through the occurrence of past events.

Key Features

A liability exists when:

- The entity is under an existing commitment (legal or constructive).

- The duty is a result of an earlier occasion.

- The relocation of the economic resources will be needed in the settlement.

Liabilities classification

Current Liabilities

However within one year or operating cycle:

- Trade payables

- Short-term loans

- Accrued expenses

- Taxes payable

Non-Current Liabilities

Due after more than one year:

- Long-term loans

- Bonds payable

- Lease obligations

- Deferred tax liabilities

Recognition Criteria

A liability is considered as recognized when:

- There is present obligation.

- The likelihood of outflow of resources.

- The quantity could be quantified accurately.

On a case in point, when a company takes goods on credit, a liability (accounts payable) is recorded since the company has a duty to pay the supplier.

Measurement Bases

The liabilities can be determined as:

- Historical Cost: The amount obtained on exchange of the obligation.

- Amortized Cost: Amortized plus interest and repayments.

- Fair Value: Obligation market value.

- Present Value: Finding of discounted value of future discounted payments.

3. Equity

Definition

The equity is the remaining interest of the assets of the entity after the exclusion of liabilities.

Mathematically:

Equity = Assets – Liabilities

Equity shows the owners right of the business.

Components of Equity

- Share capital

- Retained earnings

- Reserves

- Other comprehensive income

Nature of Equity

Equity is not an obligation to transfer resources presently, as is the case with liabilities. It is the residual interest.

Changes in Equity

Equity increases through:

- Owner contributions

- Profit generation

Equity decreases through:

- Losses

- Dividends

- Owner withdrawals

Equity also connects the statement of financial position and the statement of income since profit or losses are directly related to retained earnings.

4. Income

Definition

The increases or decreases in income are described by changes that occur in assets or liabilities which cause changes in equity, without considering the contributions made by the owners.

Types of Income

- Revenue: Income, which emerges as a result of normal operations (e.g., sales, services).

- Gains: Other increases in the benefits of the economy (sale of assets, revaluation gains).

Recognition Criteria

Income is recognized when:

- There is a growth in economic benefits.

- It can be measured reliably.

Revenue recognition is based upon performance obligations- this is normally when the control of goods or services is transferred to the customer.

Measurement of Income

The income is usually determined at:

- Consideration received or receivable (fair value).

Proper measurement insures the determination of the profits properly.

5. Expenses

Definition

Expenses are decreases in assets or Increases in liabilities which leads to a decrease in equity, other than distributions to owners.

Types of Expenses

- Cost of sales

- Salaries and wages

- Depreciation

- Rent and utilities

- Interest expense

Recognition Criteria

Expenses are recognized as the time:

- It has a decline in economic gains.

- The amount that can be quantified.

The matching principle tends to drive the recognition of expenses and to only record the expense during the same period as the associated revenue.

Measurement of Expenses

Expenses are measured at:

- Historical cost (i.e., the cost of acquiring goods sold).

- Specified cost (e.g. depreciation).

- Fair value (where there is a remeasurement case).

Interaction Within the Equation of Accounting

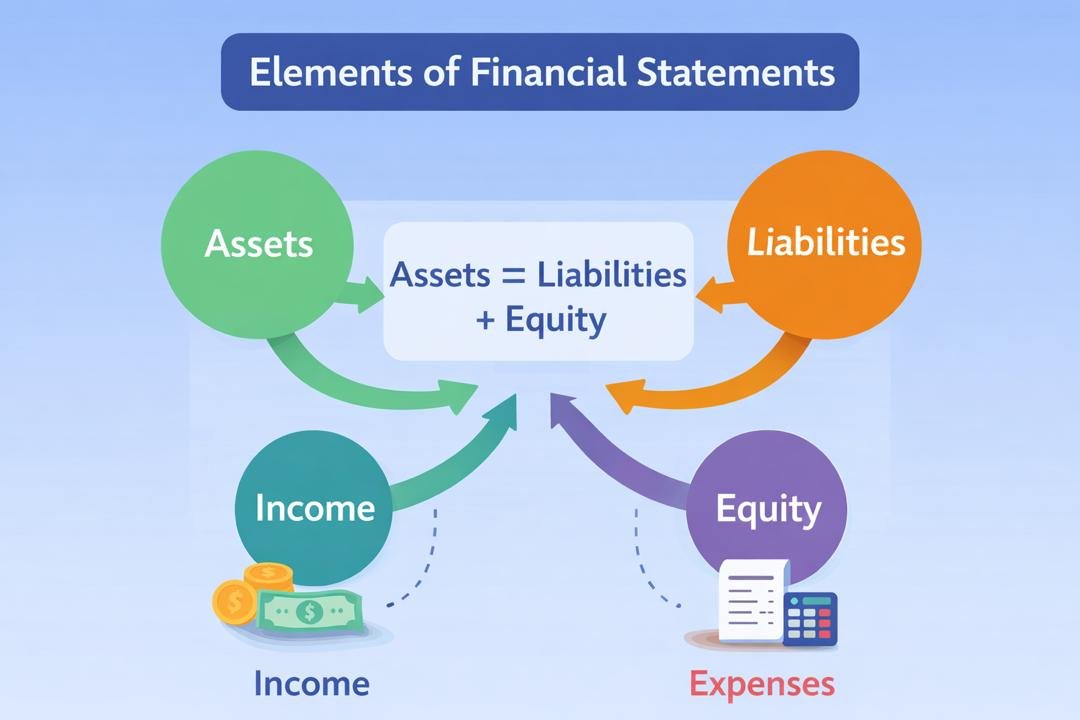

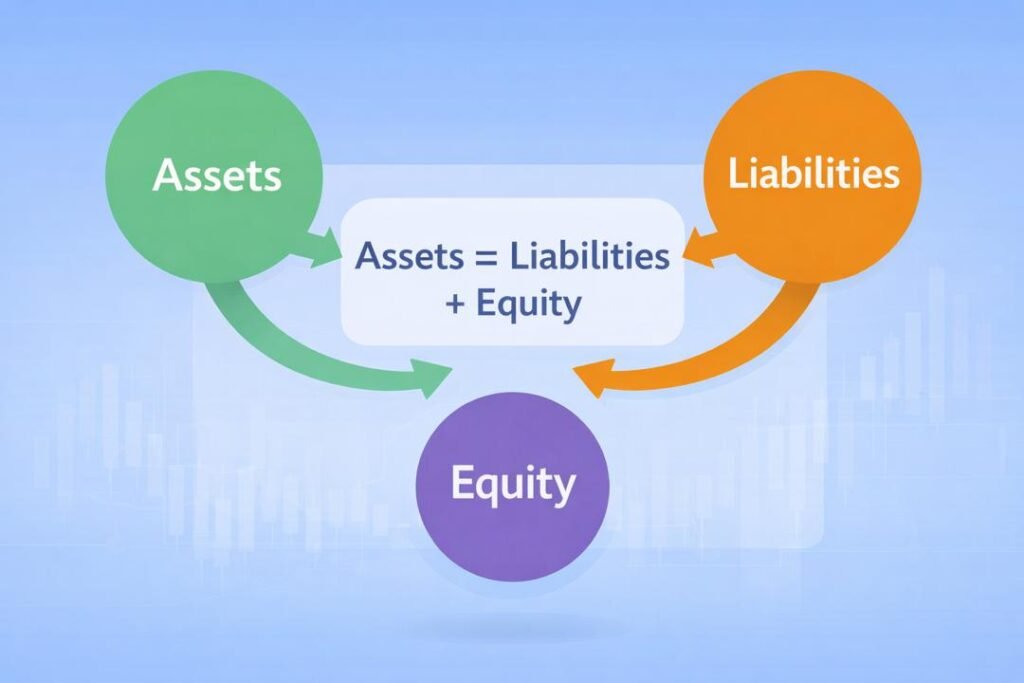

These five elements are interrelated based on the basic accounting formula:

Assets = Liabilities + Equity

Equity is eventually influenced by income and expenses.

How the Elements Interact

When income is earned:

- Assets grow (e.g. cash or receivables).

- Growth in equity (by retained earnings).

When expenses are incurred:

- The assets reduce or the liabilities grow.

- Equity decreases.

Therefore, income and expenses describe the equity changes between two reporting periods.

Statement of Financial Position

It is stated in the statement of financial position (balance sheet):

- Assets

- Liabilities

- Equity

It shows the financial position of the entity at a given date.

Structure

Assets:

- Current

- Non-current

Liabilities:

- Current

- Non-current

Equity:

- Share capital

- Retained earnings

- Reserves

The decision on measurements (historical cost and fair value) has a great impact on reported totals.

Income Statement

The income statement shows the financial performance in a certain period of time.

Format:

- Revenue

- Less: Expenses

- Equals: Profit or Loss

Profit makes equity, loss makes equity.

The income statement determines how activities changed the economic resources over the period.

The Difference between Recognition and Measurement

Recognition will dictate whether an item will be recorded in financial statements.The amount at which it is manifested is determined by measurement.

Only an item that satisfies the following criteria cannot be recognized as an asset:

- Measurement is unreliable.

- This is not likely to give future economic benefits.

As an example, internally generated goodwill is not usually recognized since it cannot be measured reliably.

Importance of Consistency and Reliability

Financial statements integrity is subject to:

- Consistent classification.

- Reliable measurement.

- Effective use of recognition criteria.

The inaccurate identification may skew financial ratios and deceive investors as well as compromise decision-making.

Practical Illustration

Consider a company that:

- Invested N5, 000,000 cash in business.

- Asset (cash) increases.

- Equity increases.

- Purchases equipment worth N2, 000,000.

- Cash decreases.

- Equipment increases.

- Earns revenue of N1, 000,000 on credit.

- Receivables increase.

- Income increases.

- Equity increases.

- Pays salaries of N300, 000.

- Cash decreases.

- Expense increases.

- Equity decreases.

The accounting equation is maintained by the fact that every transaction involves at least two elements.

Conclusion

Financial reporting has the structure of the core components of financial statements which include assets, liabilities, equity, income and expenses. Transparency, comparability, and reliability are ensured because they are properly classified, recognized, and measured.

Financial position is described as assets and liabilities. Performance is explained in terms of income and expenses. Equity reconciles the two statements, which represent the cumulative effect of transactions.

Recognition prevents the inclusion of irrelevant and measurable reliable items in financial statements. The numerical value of those elements is ascertained by measurement. The combination of them forms the statement of financial position and income statement which makes the stakeholders have significant information on the financial health and efficiency of an entity.

Accountants, auditors, investors and financial analysts need to have a good grasp of these factors. The financial reporting would be unable to be coherent and decision-useful without a clear understanding of how they although interact within the accounting equation.

Get more well researched information about Elements of Financial Statements here.