Introduction

The contemporary business world is highly dynamic, and financial decision-making cannot be based on a simple bookkeeping or even individual accounting skills. It requires an in-depth knowledge of how various concepts of accounting are interrelated and impact each other and this can be done by Integrating accounting concepts for financial decision-making. To the basic concepts of accounting to the complex financial reporting methods, accounting offers a well-organized system through which businesses are able to gauge their performance, manage resources, as well as future planning.

The most important accounting principles are at the center of this framework and they act as the basis of recording, analyzing and interpreting financial information. These principles can be potent decision-making tools when incorporated with income theories, asset management strategies, and financial reporting practices.

To investigate further, you may consider this comprehensive guide to the key accounting principles which would give you the background information of how accounting principles influence financial reporting.

This article is a synthesis of these fundamental components into a concise framework that shows the interaction of these components in a real business environment and how Integrating accounting concepts for financial decision-making can be very vital.

Understanding the Key Accounting Principles

Accounting principles are standardized rules that are used to bring uniformity, reliability and comparability in financial reporting. These principles are the foundation of the accounting systems and are key to the generation of meaningful financial information.

Among the principles are:

1. Accrual Principle

Accrual principle is the idea that revenues and expenses should be charged when it is earned or incurred and not when cash is received or paid. This makes sure that financial statements are a true representation of the economic activity of a business.

Practical implication:

An organization that sells products in December, but the payment is made in January will need to record the revenue in December. This enables managers to effectively determine performance within the right time.

2. Consistency Principle

The same accounting methods should be applied over time by businesses unless a justifiable change is reported. This increases inter-period comparability.

Practical implication:

When a firm depreciates its assets using the straight-line technique, it may create financial trends which when changed to another technique without justification may cause distortion to the decision-maker.

3. Prudence (Conservatism) Principle

This principle encourages one to be cautious in making estimates, and make sure that assets and income are not overstated and liabilities and expenses are not understated.

Practical implication:

The losses accrued are known at an early stage whereas gains are restricted to the time they are definite. This helps to guard against over-optimistic financial reporting by stakeholders.

4. Going Concern Principle

The financial statements are prepared under the assumptions that the business will still be in operation in the future that can be predicted.

Practical implication:

Investment and financing decisions are affected by the valuation of assets when they are valued based on the ongoing use and not the liquidation value.

Income Theories and Application in the decision-making process

The measurement of income is the key to assessment of business performance. The various theories have different views on how income is to be calculated and interpreted.

1. Accounting Income vs. Economic Income.

- The accounting income is pegged on the historical cost and realized transactions.

- Economic income takes into account the fluctuations of the market value of assets and liabilities.

Application:

A business can record good accounting revenues and its assets decrease in value. Decision-makers that use accounting income only can fail to see the risks behind the scenes.

2. Permanent Income Theory

This theory draws a line between the short-run and long-run sources of income. It is used by businesses to evaluate profitability in the long-term.

Application:

The sale of an asset would not be considered a recurrent income in the future.

3. Capital Maintenance Concept

This theory is concerned at keeping the capital base of a business intact and then identifying profit.

Application:

When inflation raises the replacement cost of assets, then a firm has to consider this when reporting profits, and therefore, capital will be maintained.

Asset Management and Its Strategic Importance

Assets are the economic resources that propel businesses. A good management of the assets can guarantee maximum use and value creation over the long-term.

1. Classification of Assets

The assets can be generally divided into:

- Current assets (cash, inventory, receivables)

- Non-current assets (property, plant, equipment and intangible assets)

Decision-making impact:

Management of current assets is crucial to the liquidity analysis and strategic investment in non-current assets is crucial to long-term growth.

2. Asset Valuation and Depreciation.

Depreciation is the allocation of the cost of the physical assets during their useful life. Various techniques, including straight-line or reducing balance have impacts on reported profits.

Example:

A business with accelerated depreciation will experience less profit during the initial years, but would have tax savings. This may affect the investment and financing policies.

3. Working Capital Management

Effective management of working capital makes sure that a business is able to cover its short term liabilities.

Key components:

- Inventory control

- Receivables management

- Payables optimization

Application:

A firm that decreases its inventory holding period will have cash available to either grow or pay off debts.

Financial Reporting Practices

Financial reporting converts accounting information into a structured format that can be utilized by the stakeholders in their decision making.

1. Financial Statements

The main financial statements are:

- Income Statement: Reflects the profitability in a time span.

- Balance Sheet: Shows financial status at a given time.

- Cash Flow Statement: Monitors cash flows in and out.

All the statements give us individual insights, yet they are related to each other.

2. Qualitative Characteristics of Financial Information.

To make financial reports helpful, they should be:

- Relevant

- Reliable

- Comparable

- Understandable

Application:

These characteristics are used by investors to compare the performance and determine investment choices.

3. Regulatory Frameworks

The accounting standards provide standardization of reporting. Adherence improves trustworthiness and provides international comparisons.

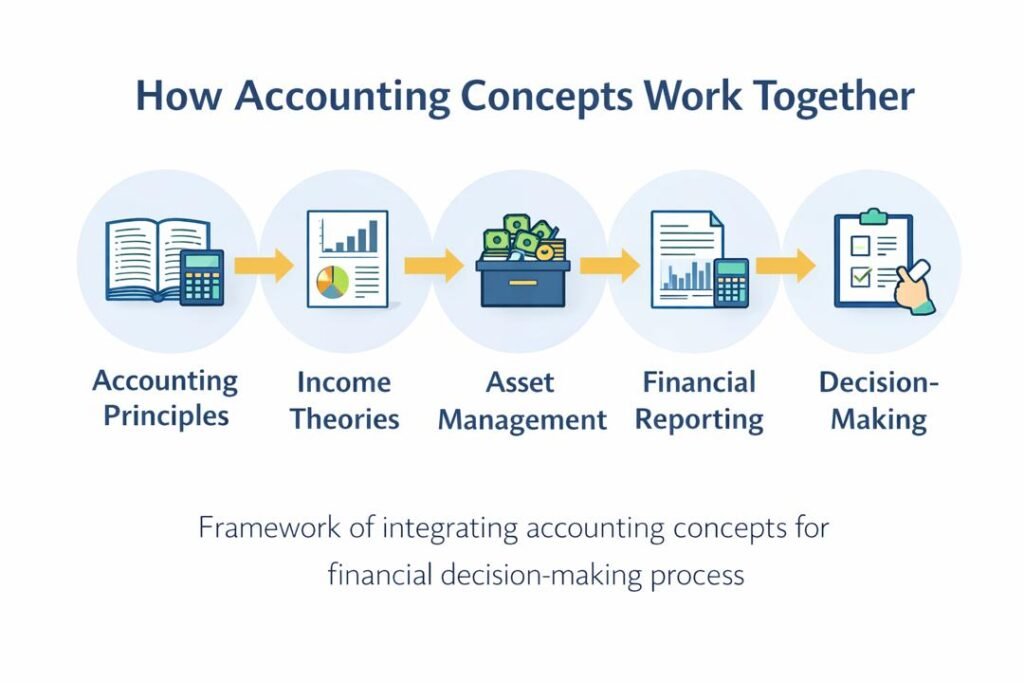

Combining Concepts: An Interconnected Framework

It is important to get to know each concept separately and the real beauty is in having them all come together in a single structure.

1. Linking Principles.

To determine the income of a given company, it is necessary to link the income measurement with the principles. The accrual principle has a direct effect on the measurement of income as it dictates the time of recognizing the revenues and expenses. This is to guarantee that income is based on actual business activity and not timing of cash flow.

2. Relating Asset Management and Profitability.

These asset management choices, including the depreciation policies and investment choices, have an impact on the balance sheet and the income statement.

Example:

Choosing a depreciation method impacts:

- Reported profit

- Tax liability

- Asset valuation

3. Matching Financial Reporting and Decision Needs.

The financial reports should be in line with the interests of the stakeholders such as the managers, investors and creditors.

Example:

A lender can be interested in the liquidity ratios that are based on the balance sheet whereas an investor can be interested in the profitability trends that may be based on the income statement.

Applied Case: A Business Case

Think of a manufacturing firm that is considering investing in new machinery.

Step 1: Accounting Principles.

The accrual principle is applied in the company to estimate future revenues that the machine will bring and compares it with the costs.

Step 2: Income Impact Evaluation.

The company differentiates between using the income theories:

- Short-term profits as a result of greater production.

- Sustainability of profits in the long run.

Step 3: Implications of Assets.

The equipment is then listed as a non-current asset and it is depreciated against the useful life. The method of depreciation that is selected influences the profit and tax.

Step 4: Financial Statement Analysis.

The investment impacts:

- Balance sheet (increase in assets)

- Income statement (depreciation expense)

- Cash flow statement (initial cash outlay)

Step 5: Decision-making.

A combination of these factors will enable the company to know whether the investment will increase profitability and financial stability.

Integrated Accounting Knowledge in strategic decision-making

1. Budgeting and Forecasting

Financial projections of a business can be made with the help of integrated accounting concepts.

Example:

To project revenue, one should know accrual accounting, and the cost projections will rely on the depreciation of the assets and behavior of costs.

2. Investment Decisions

Companies analyze the opportunities of investment by considering:

- Expected returns

- Risk factors

- Effects on financial statements.

3. Performance Evaluation

Financial ratios are accounting data that help managers to evaluate performance.

Key ratios:

- Profitability ratios

- Liquidity ratios

- Efficiency ratios

4. Risk Management

The information on accounting can be used to find financial risks, including:

- Liquidity shortages

- Asset impairment

- Overstated income

Difficulties in Implementing Accounting Concepts

Although it is important, there are challenges of integrating accounting concepts.

1. Complexity: Accounting systems may be complicated, and special expertise is needed.

2. Judgment and Estimates: Estimates are likely to cause some uncertainty in many accounting decisions.

3. Changing Standards: The accounting standards are subject to regular changes which means that one has to constantly learn and adapt.

Best Practices to ensure effective integration.

To ensure the accounting knowledge is maximized, businesses should:

1. Invest in Training: Make sure that employees are aware of the concepts and practicals.

2. Use Technology: The accounting software can facilitate processes and enhance accuracy.

3. Maintain Transparency: Effective reporting uncovers confidence with stakeholders.

4. Take a Whole Person Approach: Look at the interdependence of accounting factors not as individual analyses.

Conclusion

Integrating accounting concepts for financial decision-making is critical. Incorporating essential accounting principles, theories of income, asset management plans, and financial reporting methods, businesses will have the ability to access the overall picture of their financial situation and performance.

Such a combined strategy enables those who decide to:

- Evaluate profitability accurately

- Manage resources efficiently

- Mitigate risks

- Strategize to expand in the long run.

Finally, the shift between theory and practice is in the possibility to relate these concepts and use them in practice. Effective use of accounting will make it more than a record keeping tool, it will make it a strategic asset that leads to informed decisions and long term success.

Get more well researched information about Integrating accounting concepts for financial decision-making here.