Introduction

Accounting for Investments are crucial in the contemporary business activities, as they enable organizations to increase their wealth, diversify their sources of income, and also have strategic ties with other organizations. Regardless of the type of investment an enterprise makes in shares, bonds, and other financial instruments, how they are treated in the financial statements has a big impact on the financial statements and decision making of the company.

Learning accounting for investments is a key aspect to be known by various investors, accountants and business managers. Such techniques define the recognition, measurement, and reporting of investments, which eventually affect the profitability, asset valuation, and financial well-being. This paper addresses the three accounting strategies namely cost, equity and fair value and the valuation methods and financial consequences of the accounting strategies.

We shall disaggregate these methods of investments and give insights on how businesses represent investment activities in financial statements in this guide. To further intoxicate into this subject, consider this resourceful material on accounting of investments.

The concepts of Investments in Accounting

Investments in accounting are assets that are purchased by the company with a view of earning revenue or increase in value. Such investments may be in various forms and they may include:

- Equity securities (shares in other companies).

- Debt securities (bonds and debentures).

- Financial instruments (Mutual funds and others).

The accounting treatment is mostly based on the degree of control or influence by the investor on the investee. This decides the accounting method that is the most suitable.

Classification of Investments

We should first know the classifications of investments before we go on to the accounting techniques:

1. Short-Term Investments

These are also referred to as marketable securities and are meant to be kept not more than a year. They are very liquid and can be readily converted into cash.

2. Long-Term Investments

They are retained over a period of over one year and they can involve shares of subsidiaries, associates or business partners.

3. Equity vs Debt Investments.

- Equity investments are a company ownership.

- Debt investments are the loans that are given to other parties.

All classifications have an effect on the accounting and measurement of the investment.

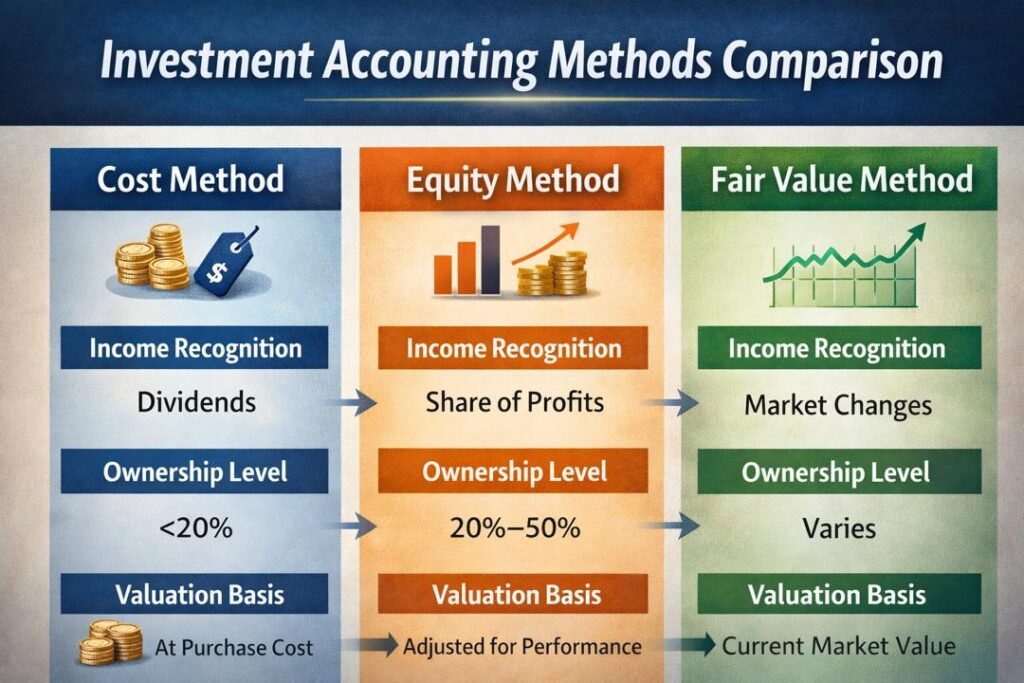

Accounting Methods for Investments

The three main accounting methods of investments are:

- Cost Method

- Equity Method

- Fair Value Method

Both approaches are used in the various conditions and carried out with different implication to the financial reporting.

The Cost Method

Overview

The cost method is applied whenever the investor has minor or no substantial control over the investee, which is usually less than 20% of the voting shares.

Recognition and Measurement

- Investments are reported at the cost of purchase.

- Income: Income is only realized when dividends are received.

- The investment value does not change except in case of impairment.

Example

When a company buys the stock of another company with a value of 10,000 and pays a dividend of 500, then it is only the dividend which is taken as income. The investment is still at 10,000.

Advantages

- Easy and simple to use.

- Reduces the variation of financial statements.

Disadvantages

- Lacks no changes in market value.

- May Over/understate actual investment value.

The Equity Method

Overview

Equity method is applied when the investor holds a great sway in the investee, normally, a percentage of 20 to 50 of voting shares.

Recognition and Measurement

- The initial recording of investment is at cost.

- The carrying amount is adjusted to reflect the amount of profits or losses the investor is entitled to in the investee.

- Dividends decrease carrying value of the investment.

Example

When a firm owns 30 per cent of another firm that generates an income of 100,000 the investor enters the 30,000 as an income. Assuming that dividends of $10,000 are earned, the value of investment will be reduced.

Key Features

- Is more economically reflective.

- Matches the income of investment with performance of the investment.

Advantages

- Gives a realistic perspective of the investment performance.

- Improves comparability of the financial statements.

Disadvantages

- Complex to use compared to the cost method.

- Needs to have access to information on the investments.

The Fair Value Method

Overview

The fair value approach is applied when the investments are actively exchanged in the financial markets or when the accounting standards presuppose valuation of the investments in the markets.

Recognition and Measurement

- Investments are reported at fair market value.

- Value changes are identified in profit or loss or other comprehensive income based on the classification.

Types Fair Value Classification

1. Trading Securities

The adjustments of value are entered in profit or loss.

2. Available-for-Sale Securities

Other comprehensive income records changes.

Example

Suppose a deposit of value 10,000 to start with grows to 12,000:

- The gain is a gain of $2,000 that is reported in the financial statements.

Advantages

- Represents the prevailing market conditions.

- Gives information in a timely manner.

Disadvantages

- Can bring in earning volatility.

- Needs quality market information.

Investment Techniques of valuation

Proper valuation is essential for accurate financial reporting. The typical methods of valuation are:

1. Market Approach: Uses the prevailing market prices to calculate the worth of investments.

2. Income Approach: The basis of estimation is based on future cash flows which are supposed to occur and which are discounted to the present value.

3. Cost Approach: Takes into account the initial cost, which has been depreciated or impaired.

Both methods are in compliance with various accounting methods and provide accounting uniformity in reporting.

Recognition Investment Income

The income of investments may be in different forms:

- Dividends on equity investments.

- Interest from debt securities

- Profits or losses due to changes in fair value.

The income recognition is based on accounting method applied:

| Method | Income Recognition |

| Cost | Dividends only |

| Equity | Share of profits/losses |

| Fair Value | Value in the market varies + income. |

Effect on Financial Statements

1. Income Statement

The accounting method has a direct influence on the reported income:

- Cost Method: Predictable, but can underreport revenues.

- Equity Method: Represents portion of profits.

- Fair Value Method: Unrealized gains/losses are included.

2. Balance Sheet

Investment valuation has an impact on the total assets:

- Cost method maintains assets unchanged.

- Equity approach modifies according to performance.

- Fair value is a reflection of current market value.

3. Cash Flow Statement

- The dividends and interest are captured as cash inflows.

- The investing activities are recorded as investment purchases and sales.

Financial Impact of Investment Accounting Approaches

Profitability

- Fair value method may increase volatility in profits

- Equity method equates profit to performance.

- Cost method can facilitate earnings but decrease transparency.

Financial Position

- Fair value gives current value of assets.

- Cost Method approach can be misleading regarding financial strength.

- Equity approach gives a fair perspective.

Decision-Making

Proper investment accounting will assist in supporting:

- Better investment decisions

- Improved financial analysis

- Enhanced stakeholder confidence

Impairment of Investments

When it can be established that the value of the investment is declining, then the investments should be impaired.

Indicators of Impairment

- Significant market decline

- Lack of finances of the investee.

- Adverse economic conditions

Accounting Treatment

- Write down the amount that is invested to recoverable amount.

- Realize loss in profit or loss.

The impairment makes sure that the value of assets is not overstated in the financial statements.

Disclosure Requirements

Accounting regulations mean that companies will be obliged to reveal:

- Accounting policies used

- Fair value measurements

- Gains and losses

- Risk exposures

These reports enhance transparency and assist users to know the financial implications of investments.

Comparison Investment Accounting Methods

| Feature | Cost Method | Equity Method | Fair Value Method |

| Ownership Level | <20% | 20%–50% | Varies |

| Income Recognition | Dividends | Share of profit | Market changes |

| Complexity | Low | Medium | High |

| Accuracy | Low | High | Very High |

| Volatility | Low | Moderate | High |

Challenges in Investment Accounting

Nevertheless, companies have a number of issues regardless of the developed methods:

1. Market Volatility: Fair value measurements are influenced by variances in prices.

2. Data Availability: Equity method entails thorough financial information of investors.

3. Judgment and Estimates: There are a lot of assumptions and estimations in valuation.

4. Regulatory Compliance: Businesses have to comply with such accounting standards as IFRS or GAAP.

Importance of Choosing the Appropriate Approach

It is important to choose the right accounting method since it:

- Gives a true picture of the investment.

- Compliant with accounting standards.

- Gives correct financial data.

- Helps in strategic decision solving of business.

A wrong approach will deceive the stakeholders and misrepresent the performance in terms of finances.

Role of Accounting Standards

International accounting standards like IFRS and US GAAP direct investment accounting in that they:

- Defining classification criteria

- Establishing measurement rules

- Uniformity among companies.

These standards promote comparability and reliability in the financial reporting.

Conclusion

Accounting for investments is a critical part of financial reporting that impacts business reporting of financial status and performance. Each of the cost method of valuation, equity method and fair value method has a distinct approach to investment valuation and revenue recognition.

Knowledge of accounting procedures of investments helps businesses to properly report on their financial operations, make quality choices and be transparent to their stakeholders. Although the cost method will be easier, the equity method will be more realistic in terms of influence and the fair value method will ensure the latest valuation.

Finally, the decision on the method will be determined by the degree of ownership, the type of investment and accepted accounting standards. Through proper valuation methods and use of the right approach, firms are able to properly control and record their investments which will help in achieving a long term success in the financial statements.

Get more well researched information about Accounting for investments here.