Introduction

Accounting is more than a system of documenting financial transactions, it is a field that has theoretical frameworks that are used to influence the manner in which organizations report, interpret and communicate financial information. These models, which are also known as key accounting theories, form the intellectual basis of explaining corporate behavior, reporting in financial market and accountability mechanisms. Accounting would not be the same without them as it would be inconsistent, directionless, and purposeless.

In this article, the general accountancy related theories are brought together in an integrated format such as the agency theory, the stakeholder theory, and the decision-usefulness theory among others. It discusses the contribution made by each of the theories to our knowledge about the dynamics of an organization, financial reporting, and governance and their relevance in the modern business world that is complex.

Understanding Theories of Accounting

Accounting theories are systematics of rules and guidelines that direct the accounting practices. They assist in the justification of why some accounting techniques are applied and the manner in which financial information is to be interpreted. The theories are critical in the formulation of accounting standards, enhancing transparency, as well as, comparability among organizations.

In a bid to examine further into the understanding of the key accounting theories, it is essential to note how each theory discusses certain areas on financial reporting and accountability of an organization.

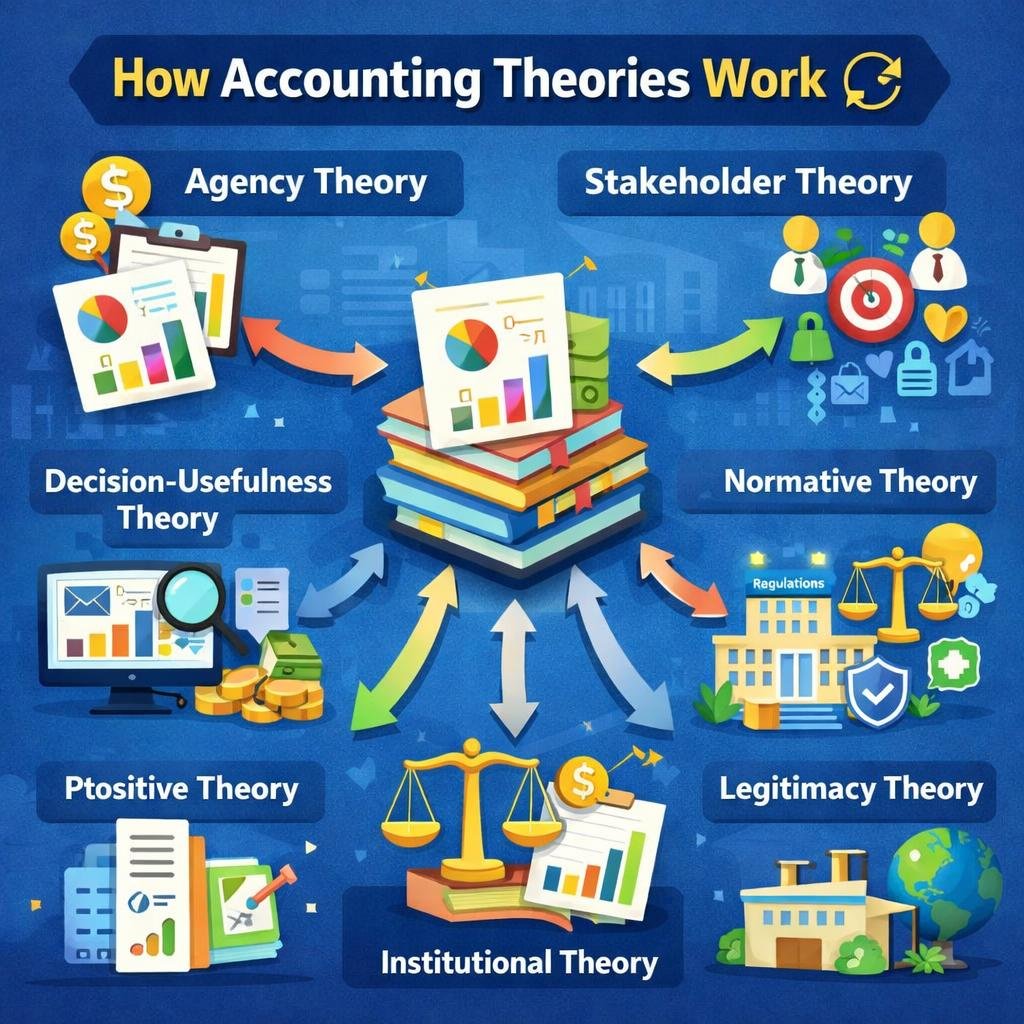

Agency Theory

Overview

One of the most significant theories in the accounting and corporate governance is the agency theory. It addresses the association between the principal (shareholders or owners) and the agents (managers or executives). According to the theory, it is the assumption that agents are not always acting in the best interests of principals, and that conflict arises between the agents and principals, which is referred to as agency problems.

Key Concepts

- Asymmetry of information: Shareholders do not always have as much information as managers.

- Moral hazard: If the action taken by the managers favors them at the expense of the owners.

- The agency costs: Agency costs involve expenditure on monitoring agents and principal interests and aligning them.

Contribution to Accounting

The agency theory has become very important in determining financial reporting practices. It emphasizes the need for:

- Clear and trustworthy financial reports.

- Independent audits

- Internal controls and governing mechanisms.

Information asymmetry will be minimized as accounting systems are meant to give confidence to the investors that the management is behaving responsibly.

The Relevance in Modern Business

The agency theory is especially applicable in the modern business world in the following way:

- The loss of ownership and control in big companies.

- Stricter oversight on the part of regulators and investors.

- The significance of corporate governance systems.

Agency theory is behind such mechanisms as performance-based pay, board control, and disclosure policies.

Stakeholder Theory

Overview

Stakeholder theory is a theory that broadens the accounting to shareholders to include parties that the activities of an organization affect. These are stakeholders such as the employees, the customers, suppliers, governments, and the general community.

Key Concepts

- There are various stakeholders in organizations.

- Value creation does not concern just financial returns.

- Decision-making is based upon ethical considerations.

Contribution to Accounting

The impact of the stakeholder theory on the accounting evolution has been the promotion of:

- Sustainability reporting

- Corporate social responsibility (CSR) reporting.

- Standards of integrated reporting.

These are practices that extend beyond the conventional financial statements to contain environmental, social, and governance (ESG) data.

Relevance in Modern Business

In recent years, the role of the stakeholder theory has been increasing as a result of:

- Greater demand of corporate disclosure.

- The increasing environmental and social sensitivity.

- Regulatory and lobby pressure.

Organizations are now supposed to be accountable not only to the shareholders but also to the entire society. This has seen the implementation of wider reporting standards that capture the interest of the stakeholders.

Decision-Usefulness Theory

Overview

The decision-usefulness theory is concerned with the main goal of accounting, which is to offer useful information that can be used in making decisions. It stresses the fact that financial reports are supposed to assist users to make sound economic decisions.

Key Concepts

- Relevance and reliability of the financial information.

- Comparability and timeliness.

- It is user-centric (investors, creditors, analysts) oriented.

Contribution to Accounting

The theory has played a great role in the development of current accounting standards. It has given rise to the formulation of frameworks that give importance to:

- Fair value measurement

- Future indicative information.

- Risks and uncertainties disclosure.

The purpose of accounting bodies in the design of standards is to increase the utility of the financial information to the decision-makers.

Relevance in Modern Business

Decision-usefulness theory has become more critically important in a rapidly changing and information-driven economy. To invest, investors need to have the right and timely information to:

- Assess company performance

- Check on investment opportunities.

- Manage risk

It is also the theory which advocates the use of technology in accounting, i.e. real-time reporting and data analytics.

Positive Accounting Theory

Overview

The theory of positive accounting attempts to explain and predict real accounting practice and not to prescribe best accounting practices. It looks at the reasons why companies adopt certain accounting techniques and the ways economic incentives affect the decision of the company.

Key Concepts

- Banking decisions appeal to self-interest.

- Companies are reactive to the regulatory and market pressures.

- Contractual relationships have an effect on reporting choices.

Contribution to Accounting

Positive accounting theory assists researchers and practitioners to realize:

- Behavior of earnings management.

- Regulatory implications on the reporting practices.

- The correlation between accounting and economic performance.

It also gives a true picture of accounting as a mechanism which is manipulated by incentives and limitations.

Relevance in Modern Business

The theory is especially applied to the analysis of:

- Corporate scandals and bad financial reporting.

- Impacts of new accounting standards.

- Strategic financial reporting decisions.

It is through the knowledge of what drives accounting decisions that the stakeholders will be in a position to interpret the financial statements.

Normative Accounting Theory

Overview

Normative theory of accounting dwells into what accounting practices must be. It offers suggestions that depend on sound logic and judgment.

Key Concepts

- Ideal accounting standards

- Ethical considerations

- Prescriptive frameworks

Contribution to Accounting

The normative theory has helped in:

- The invention of theoretical models.

- Arguments between fair value and historical cost.

- Accounting practice ethics.

It is a basis of setting standards that seek to enhance quality of financial reporting.

Relevance in Modern Business

The normative theory is relevant in:

- Leading standard-setting organizations.

- Proceed with issues cropping up like sustainability reporting.

- Encouraging accountancy ethics.

It makes sure that accounting is developed according to the fluctuating demands of the society.

Institutional Theory

Overview

The institutional theory investigates the impact of social, cultural, and regulatory settings on the organizational practices such as accounting.

Key Concepts

- Organizations are aligned to the outside forces.

- Practices are even normative and tradition-based.

- One of the major behavior drivers is the legitimacy.

Contribution to Accounting

Institutional theory describes the reason why firms will embrace specific accounting practices including:

- Adherence to international standards.

- Implementation of sustainability reporting.

- Installing governance structures.

The practices do not necessarily emerge due to economic need only but also the need to acquire legitimacy.

Relevance in Modern Business

Institutional theory has become more significant due to globalization. Organizations have to successfully negotiate:

- Various regulatory settings.

- Cultural expectations

- Economic accounting standards

The convergence in accounting practices among countries can be explained using this theory.

Legitimacy Theory

Overview

According to the legitimacy theory, organizations aim to act within the framework of expectations of society. They sustain or recover their legitimacy through accounting disclosures.

Key Concepts

- Social contract between the society and organizations.

- The means of legitimacy upon disclosure.

- Reputation management

Contribution to Accounting

The legitimacy theory has affected:

- Social and environmental disclosures.

- Crisis reporting tactics.

- Voluntary reporting practice.

Firms tend to share more information to show their dedication to the values of the society.

Relevance in Modern Business

The legitimacy theory is very pertinent in a time of increased publicity. Organizations must:

- Action against environmental issues.

- Respond to social issues

- Maintain public trust

Any lack of this may lead to reputational losses and financial implications.

Integrating the Theories

Although the key accounting theories have different insights, their integration is their real worth. These two materials combined give a deep insight into accounting practices and organizational behavior.

- Agency theory is a theory of conflict and system of governance.

- The stakeholder theory expands responsibility.

- Decision-usefulness theory: is concerned with the quality of information.

- Positive and normative theories provide the descriptive and prescriptive views.

- The institutional and legitimacy theories emphasize the external factors.

Taking these views together, accountants and policy makers can design better systems that would strike a balance between economic efficiency, ethical implications and expectations by the society.

Implications for Corporate Governance

The accounting theories are important in the corporate governance as they:

- Increasing accountability and transparency.

- Helping to make effective decisions.

- Minimizing conflict of interest.

These theoretical frameworks form the basis of governance systems including audit, boards of directors and disclosure requirements. They make sure that organizations act in a responsible and optimal manner to the stakeholders.

Challenges and Future Directions

Despite their relevance, accounting theories have a number of challenges:

- Clearly, accelerating technological shifts.

- There is growth in the complexity of financial instruments.

- The changing stakeholder expectations.

Continual evolutions in accounting theory will tend to concentrate on:

- Artificial intelligence and data analytics.

- Sustainability and ESG reporting.

- Increased focus on international standardization.

Such innovations will necessitate the constant improvement of the existing theories and the creation of new theories.

Conclusion

The significance of accounting tools as a communication, accountability, and decision-making instrument makes the research of significant accounting-related theories an indispensable part of the research. Since agency theory is centered on the concept of governance and the stakeholder theory emphasizes the concept of broader responsibility, both schools of thought help in the comprehension of financial reporting and organizational behavior in a deeper way.

These key accounting theories are extremely applicable in the current dynamic business world. They shape the creation of accounting standards, educate the corporate governance practices and assist organizations in maneuvering through the complicated economic and social environments. The combination of these points of views will help to make accounting develop and fulfill the demands of the fast-evolving world.

Finally, key accounting theories is not merely an academic concept but practical and helps to define how organizations behave, report and add value to society.

Get more well researched information about the key accounting theories here.