A consolidation worksheet

may have many forms. As a minimum however, the worksheet should have;

may have many forms. As a minimum however, the worksheet should have;

(a) Columns for parent and subsidiary account balance (taken from their

separate financial statements or preclosing trial balances)

separate financial statements or preclosing trial balances)

(b) Columns for elimination and adjustment and

(c) Columns for the consolidated balances.

Columns may be headed

account name, parent, subsidiary, adjustments and consolidated balances. Each

line would consist of and account name, the separate balances, adjustment, and

a cross – footed balances.

account name, parent, subsidiary, adjustments and consolidated balances. Each

line would consist of and account name, the separate balances, adjustment, and

a cross – footed balances.

Obviously, more columns may

be added as necessary for additional subsidiaries, for distinguishing between

nominal example, temporary or income statement accounts and real accounts

example balance sheet accounts, and so on.

be added as necessary for additional subsidiaries, for distinguishing between

nominal example, temporary or income statement accounts and real accounts

example balance sheet accounts, and so on.

Regardless of the form,

however, worksheet are merely tools which help the accountant should always

keep in mind that when the worksheet gets too cumbersome or too complicated, it

has failed in its main purpose and should be modified in order to retain its

usefulness.

however, worksheet are merely tools which help the accountant should always

keep in mind that when the worksheet gets too cumbersome or too complicated, it

has failed in its main purpose and should be modified in order to retain its

usefulness.

The worksheet procedure

should be an aid not a hindrance to the consolidation process. Individual worksheet

adjusting entries may vary between accountants even through the financial

statements products by them are identical. The adjusting style is an individual

matter and depends upon prior training, inclination, or personal bias.

should be an aid not a hindrance to the consolidation process. Individual worksheet

adjusting entries may vary between accountants even through the financial

statements products by them are identical. The adjusting style is an individual

matter and depends upon prior training, inclination, or personal bias.

However, there are two

basic styles:

basic styles:

(a) Make an adjustment to

record each new piece of data and let the final balance in an account be the

result of the cumulative adjustment; or

record each new piece of data and let the final balance in an account be the

result of the cumulative adjustment; or

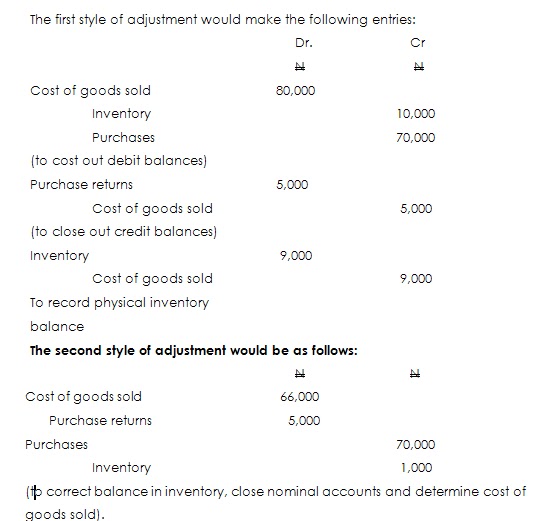

(b) Determine what the desired final balance should be and make

whatever net adjustment will accomplish the desired result. For example,

consider an inventory isN10,000;

purchasesN70,000; purchase return N5,000; and physical inventory count at

the end of the period isN9,000.

whatever net adjustment will accomplish the desired result. For example,

consider an inventory is

purchases

the end of the period is

Both adjusting entries

produce the same resulting balances. Choice of adjusting style should not

confuse anyone who understands the accounting process and the underlying

circumstances. He should be able to interpret what has been done.

produce the same resulting balances. Choice of adjusting style should not

confuse anyone who understands the accounting process and the underlying

circumstances. He should be able to interpret what has been done.

Worksheet adjustment differ

depending upon whether the nominal accounts have been closed. If they have been

closed, the Retained Earning balance already reflects the results of the

current periods activity that is, given separate financial statement nominal

account adjustments also have to be reflected in consolidated retained

earnings.

depending upon whether the nominal accounts have been closed. If they have been

closed, the Retained Earning balance already reflects the results of the

current periods activity that is, given separate financial statement nominal

account adjustments also have to be reflected in consolidated retained

earnings.

But given trial balances,

nominal adjustments will automatically be taken into consolidated retained

earnings when the nominal accounts are closed.

nominal adjustments will automatically be taken into consolidated retained

earnings when the nominal accounts are closed.