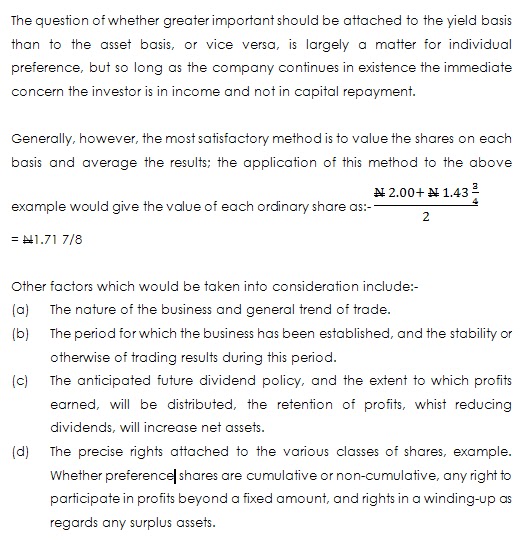

Preference shareholders are concerned with the maintenance of profits

worth a view to ensuring regular payment of the fixed dividends rather than

with the value assets. The question of capital repayment on liquidation is

usually deemed to be of secondary importance to dividend maintenance.

worth a view to ensuring regular payment of the fixed dividends rather than

with the value assets. The question of capital repayment on liquidation is

usually deemed to be of secondary importance to dividend maintenance.

Similarly to preference shareholders, ordinary Shareholders are not

greatly concerned with the actual value of assets but are interested primarily

in dividend possibilities. As regards possibilities, ordinary shareholders may

be divided into two classes: –

greatly concerned with the actual value of assets but are interested primarily

in dividend possibilities. As regards possibilities, ordinary shareholders may

be divided into two classes: –

(a) Those that are to receive

the largest possible dividends and to let the future look after itself, these

shareholders usually criticize a too prudent policy which seems to them to

benefit the preference shareholders (by making possible the payment of

preference dividends out of reserves in years when trading losses are incurred

much more than themselves.

the largest possible dividends and to let the future look after itself, these

shareholders usually criticize a too prudent policy which seems to them to

benefit the preference shareholders (by making possible the payment of

preference dividends out of reserves in years when trading losses are incurred

much more than themselves.

(b) Those who take longer view

that the setting aside of ample reserves is of the greatest benefit to the

company as a whole and thus, ultimately, to themselves.

that the setting aside of ample reserves is of the greatest benefit to the

company as a whole and thus, ultimately, to themselves.

The examination of the accounts from the point of view of a shareholder

or prospective shareholder raises questions of share valuation.

or prospective shareholder raises questions of share valuation.

Two methods of computing the value of shares are commonly employed:

(1) The yield or profit basis

Where this basis is employed it is first necessary to determine the rate

of interest which an investor would consider to be a seasonal yield on an investment

in a share of the class concerned. This rate be based on the current rate of

interest on gilt-edged securities as increased to compensate for the degree of

risk involved and adjusted in view of the class of share concerned; or

alternatively the current return on investments in other business of the same

types and size, and in which the risks are similar, may be taken as a basis and

adjusted for any special circumstances.

of interest which an investor would consider to be a seasonal yield on an investment

in a share of the class concerned. This rate be based on the current rate of

interest on gilt-edged securities as increased to compensate for the degree of

risk involved and adjusted in view of the class of share concerned; or

alternatively the current return on investments in other business of the same

types and size, and in which the risks are similar, may be taken as a basis and

adjusted for any special circumstances.

Where preference shares are being valued, it is generally necessary

merely to compare the fixed dividend there on with the current yield to compare

the fixed dividend there on with the current yield rate.

merely to compare the fixed dividend there on with the current yield to compare

the fixed dividend there on with the current yield rate.

In the case of ordinary shares, however, it is necessary to estimate the

future maintainable annual profits which will be available for distribution to

the ordinary shareholders after the payment of preference dividends; these

profits will then be capitalized by computing the capital sum interest on which

at the ascertained yield rate will be equal to the net annual profit.

future maintainable annual profits which will be available for distribution to

the ordinary shareholders after the payment of preference dividends; these

profits will then be capitalized by computing the capital sum interest on which

at the ascertained yield rate will be equal to the net annual profit.

This capital sum represents the total value basis is adopted the super

profits resulting from good – will are included in the estimated annual

profits, and thus he capital value of super profits) and consequently no

further adjustment for goodwill is necessary.

profits resulting from good – will are included in the estimated annual

profits, and thus he capital value of super profits) and consequently no

further adjustment for goodwill is necessary.

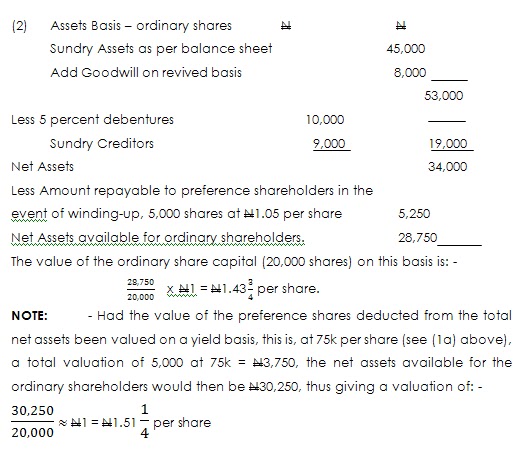

(2) The assets or equity basis

Generally this basis can be employed only in connection with ordinary

shares (unless the preferences shares have a right to participate equally with

the ordinary shares in any surplus assets on liquidation and are not

preferential as to capital, but this is not usually the case).

shares (unless the preferences shares have a right to participate equally with

the ordinary shares in any surplus assets on liquidation and are not

preferential as to capital, but this is not usually the case).

All the assets, including goodwill, must be valued and totaled, and from

this total are deducted the liabilities to creditors, debenture-holders and

other non-shareholders, thus giving the total net assets. The value of the preference

share capital is then deducted to give the net assets available for the

ordinary shares, and for this purpose it is considered that the value of the

preference share capital is to be taken at the amount repayable in a

winding-up, although some authorities consider that when winding-up is not

contemplated the value on yield basis should be taken.

this total are deducted the liabilities to creditors, debenture-holders and

other non-shareholders, thus giving the total net assets. The value of the preference

share capital is then deducted to give the net assets available for the

ordinary shares, and for this purpose it is considered that the value of the

preference share capital is to be taken at the amount repayable in a

winding-up, although some authorities consider that when winding-up is not

contemplated the value on yield basis should be taken.

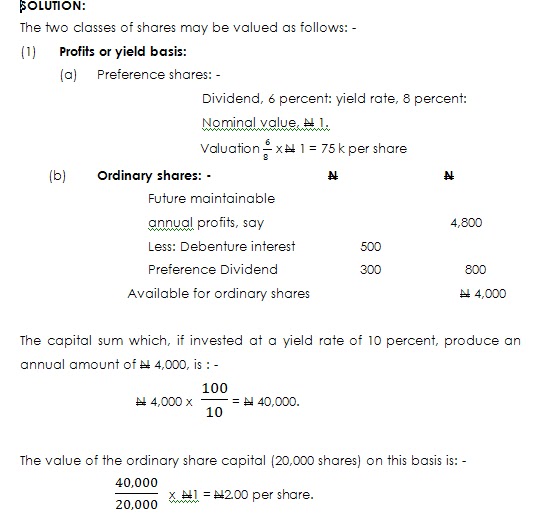

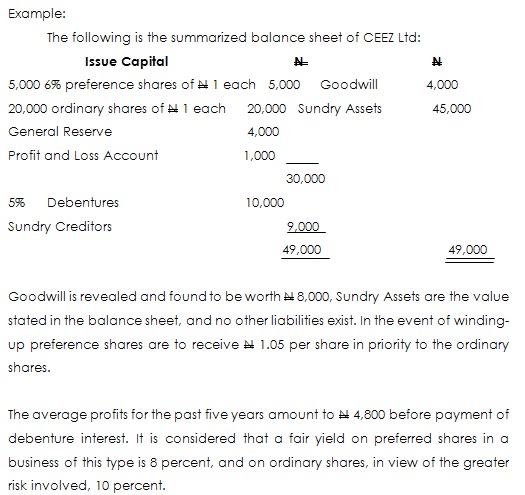

REQUIRED: Determine the value of each

share using the two main methods of valuing shares.

share using the two main methods of valuing shares.