Limited liability companies

are liable to pay company tax on their profit. In addition, the company must

account to the board of internal revenue for income tax on the following:

are liable to pay company tax on their profit. In addition, the company must

account to the board of internal revenue for income tax on the following:

(a) Dividends paid out of profits

(b) Other distribution of profit and

(c) Interest payment and annual charges

Company tax is not charged

in dividend received by a company because these dividend have been taxed at

source (company paying the dividend). Withdrawing tax is a form of income tax

paid by individuals and companies on dividends they receive from shares they

invested their money in.

in dividend received by a company because these dividend have been taxed at

source (company paying the dividend). Withdrawing tax is a form of income tax

paid by individuals and companies on dividends they receive from shares they

invested their money in.

The following should be

borne in mind in company taxation:

borne in mind in company taxation:

1. Financial

year – This means the accounting period. This is the financial year of the

board if internal revenue.

year – This means the accounting period. This is the financial year of the

board if internal revenue.

If we go by accounting

periods that are segment like this- 1st April-March 31st 1993, 1994.

periods that are segment like this- 1st April-March 31st 1993, 1994.

If we have two segment as above

making one financial year we can compute our income tax using the next example.

making one financial year we can compute our income tax using the next example.

Financial year 1990 – 40%

Financial year 1991 – 35%

The assessment will be as

follows:

follows:

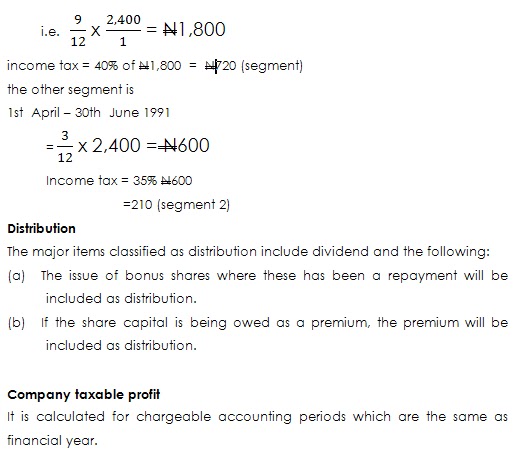

1st July 1990 – March 31, 1991 (9 months)

Assume that XYZ Company Ltd

made an accounting profit ofN663,000

for the year ended 30th June, 1985. The computation of the company’s tax profit

is as shown after deducting expenses and all deductibles.

made an accounting profit of

for the year ended 30th June, 1985. The computation of the company’s tax profit

is as shown after deducting expenses and all deductibles.

Accounting profit year

ended 30/6/85 663,000

ended 30/6/85 663,000

Add back:

Depreciation 62,000

Sundry disallowable

(example entertainment)

3,000 65,800

3,000 65,800

Company tax profit

728,800

728,800

Again deduct capital

allowances ofN85,500, then you have

company tax allowance of

allowances of

company tax allowance of

=

Note

(1) Accounting

profit and company profit are both deducted after debenture interest its paid.

profit and company profit are both deducted after debenture interest its paid.

(2) Depreciation

is a deduction in computing accounting profit but in computing company tax

profit, capital allowance is substituted.

is a deduction in computing accounting profit but in computing company tax

profit, capital allowance is substituted.