Introduction

Accounting is not only a process of documenting financial transactions, but rather a systematic system that has theories to explain, anticipate and shape how financial information should be prepared and utilized. Normative vs positive accounting theories are some of the most important theoretical frameworks in accounting. These two methods have a difference of basic purpose, philosophy, and application which are critical in the development of the accounting standards and practices.

It is important that accountants, policymakers, and business people should understand the differences between normative vs positive accounting theories. Whereas normative theories are concerned with the prescriptions of the ideal accounting practices, positive theories are concerned with the description and predicting actual accounting behavior. The paper looks into their philosophical premises, methods dissimilarities, and their practical implication on standard-setting, financial reporting, and decision-making.

Understanding Normative Accounting Theory

The normative accounting theory is prescriptive in nature. It is interested in the way things ought to be done in accounting, not how they are being done. This practice is based on value judgments and aims at defining the ideal standards of financial reporting.

Philosophical Underpinnings

The normative theory relies on deduction. It starts with broad principles or objectives, e.g. fairness, transparency, or usefulness, and derives particular accounting rules out of them. This method can be seen as an expression of morality and the social norms.

A typical example illustration is that a normative theorist would contend that financial statements must reflect a true and fair picture of financial position of a company. Based on this principle, they would suggest certain measurement and disclosure techniques that serve this purpose in an optimal way.

Key Characteristics

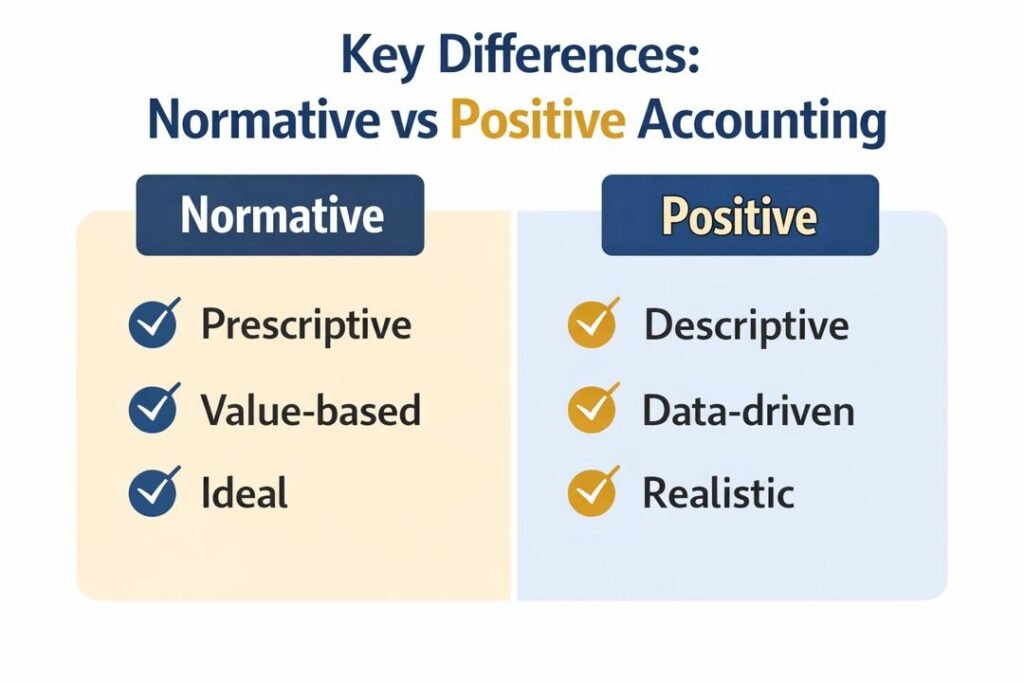

- Prescriptive Nature: Normative theories prescribe the accounting practices that should be.

- Value-Based Judgments: They include moral and subjective factors, including equity and topicality.

- Goal-Oriented Approach: Theories are developed to fulfill certain goals such as enhancing the usefulness of decisions.

- Idealistic Perspective: They also tend to come up with standards that do not necessarily coincide with the existing practices.

Examples of Normative Approaches

The normative theories have past lessons in accounting standards. An example is that the initial conceptual frameworks focused on ideal bases of measurement like the current cost accounting or fair value accounting, and this was on what was deemed to be the most significant to the users.

Understanding Positive Accounting Theory

Positive accounting theory (PAT) is, conversely, descriptive and predictive. It is concerned with why accountants and firms adopt specific accounting techniques and why they should act in a specific way in various situations.

Philosophical Underpinnings

The positive theory is based on observation and scientific methodology. It is based on evidence and data analysis as opposed to subjective approach. This is aimed at generalizing accounting behavior.

Positive accounting theory is also closely related to economic theories and implies that human beings are self-interested. It tends to analyze the relationship between incentives, contracts, and market forces and accounting decisions.

Key Characteristics

- Descriptive Nature: It describes how accounting is carried out in reality.

- Predictive Capability: It predicts the reaction of the firms to the shift in the regulation or economic conditions.

- Objective and Empirical: It is based on the visible data and statistical examination.

- Behavioral Focus: It discusses the reasons of accounting choices.

Examples of Positive Accounting Theory

One such example is the bonus plan hypothesis, which holds that in instances where a manager is paid based on profits, then they tend to stick to accounting practices that can inflate the reported earnings. Equally, the debt covenant hypothesis is based on the assumption that companies that are near breaching debt contracts will use accounting procedures that increase financial ratios.

Key Differences between the Normative and Positive Accounting Theories

The differences between normative and positive accounting theories may be reflected on a number of levels:

Purpose and Objective

- Normative Theory: It looks at what accounting should be.

- Positive Theory: It is concerned with what exists and why, as to the accounting practices.

Normative theory is supposed to enhance accounting practices, whereas positive theory attempts to explain and foretell it.

Methodological Approach

- Normative: There is deductive reasoning and logical argument.

- Positive: Employs inductive logic, empiric data and statistical techniques.

Normative methods are also not usually empirically validated, as positive methods are based on testable hypotheses.

Role of Values

- Normative: Takes into account the subjective values and ethical aspects.

- Positive: It does not use value judgments, but is objective in its analysis.

This difference brings out the philosophical gap of idealism and realism.

Nature of Conclusions

- Normative: It generates prescriptions and recommendations.

- Positive: Produces descriptions and predictions.

Practical Orientation

- Normative: Focused on the betterment of the accounting standards.

- Positive: Leans towards the explanation of behavior.

Interrelationship between Normative and Positive Theories

Normative and positive accounting theories do not imply each other, although they differ greatly. On the contrary, they are mutually complementary in terms of practice.

The vision of what accounting must accomplish and directions are given by normative theories, whereas positive theories give hints on what is possible and what conducts. An example is that in the formulation of new standards, regulating bodies can use normative principles to provide a basis of objectives, but apply positive research to predict how companies will react.

This interaction makes the accounting standards conceptually sound and practical.

Implications on Standard-Setting

Normative Influence on Standard-Setting

The normative theories are central to accounting standards development. Conceptual frameworks usually describe the goals and qualitative nature of financial reporting, and are typically used by the setting of standards.

These frameworks are also normative in nature, in that way that they describe what financial reporting ought to accomplish. As an illustration, such concepts as relevance, reliability and comparability are premised on normative judgments.

Positive Impact on setting of standards

The positive accounting theory can help in this aspect since it gives evidence regarding the reaction of firms to proposed standards. This assists regulators in predicting unwanted effects or unintentional impacts, e.g., management of earnings or avoidance of regulation.

As an example, when a new standard is forecasted to decrease the reported profits, the positive theory can forecast that firms will probably resist the implementation or avoid it.

Combined Impact

To be an effective standard-setter there must be a balance between normative ideals and positive realities. When one side of the argument is overlooked, either action will result in irrelevant or useless regulations.

Financial Reporting Implications

Normative Perspective

Based on normative perspective, financial reporting is supposed to bring useful information to the stakeholders so that they make informed decisions. This involves open disclosures, uniform measurement procedures and ethical practices.

The normative theories embrace practices that improve the quality and reliability of the financial information.

Positive Perspective

The positive accounting theory focuses on the actual financial statement preparation of firms. It is aware of the fact that managers can be motivated to do things that distort earnings or choose accounting approaches that will be favorable to them.

This view makes the stakeholders more aware of the possibility of bias in financial reports and interprets information more critically.

Real-World Application

Practically, financial reporting is a case of a mixture of the two methods. Although standards are set on the basis of normative principles, reality tends to follow the predictions in the positive theory.

Implications for Decision-Making

For Managers

Accounting information assists managers in making decisions that are strategic. Normative theories lead them to optimal practices and positive theories assist them in the realization of the impacts of various accounting decisions.

To give an example, a manager can assume a specific accounting approach not only due to being advised but also because it will be consistent with incentives or legal requirements of a contract.

For Investors

Financial statements are used by investors to determine the performance of companies. The knowledge of the positive accounting theory enables them to realize possible biases and modify their analyses.

Instead, normative theory will assure them that standards seek to offer useful and reliable information.

For Regulators

Regulators need to have a balance between the ideal and reality. The normative theories assist in the definition of goals, whereas the positive theories offer information about the issues which arise during the implementation process.

Criticisms of Normative and Positive Accounting Theories

Normative Theory has been subject to criticism.

- Lack of Empirical Support: Normative theories have been criticized as being highly abstract and lack of real-life evidence.

- Subjectivity: The use of value judgments may cause conflict and contradictions.

- Practical Limitations: Theoretical perfection can be hard to work with in the real-world.

The Positive Accounting Theory has several criticisms.

- Ethical Neutrality: Positive theory does not answer the question on whether practices are good or bad.

- Excessive emphasis on Self-Interest: It presupposes that people are always in their self-interest and this does not always work out.

- Limited Prescriptive Value: It does not offer any direction on how to better the accounting practices.

Practical Examples in the Real World Accounting

Example 1: Revenue Recognition

The recognition of revenue is governed by a rule that applies to a company that has not yet begun to generate significant revenue but has already billed its product or service. The rule is as follows; as soon as a company has billed its product or service before generating significant revenue, the rule applies to them, implying that the recognition of revenue should occur.

Normative theory would dictate the way revenue should be identified so that there is precision and equity. Positive theory would look at the actual method of revenue recognition used in companies and why the companies decide to use a specific method.

Example 2: Depreciation Methods

Normative approaches could suggest the best and most suitable approach to use in regards to asset utilization whereas the positive theory would examine why companies would adopt approaches that would maximize tax benefits or reported profits.

Example 3: Financial Disclosure

Normative theory promotes full disclosure to increase transparency. Positive theory examines how companies make decisions in relation to the information they will disclose depending on the cost and benefits.

Conclusion

The difference between the normative vs positive accounting theories is the key to the formation and utilization of accounting practices. Normative theories give the perfect outline of what accounting ought to do and have values, goals, and morals. Positive theories on the other side provide the real picture or account of explaining and forecasting the actual performance in the accounting scene.

Collectively, the theories produce a moderate solution to accounting. The normative theory keeps the standards relevant and focused to the societal expectations whereas the positive theory keeps them feasible and based on reality.

In contemporary accounting, none of the two ways can be used as a standalone approach. The combination of the two perspectives is necessary to achieve the proper financial reporting, standard-setting, and decision-making. Through the realization of the differences and complementarities, professionals will be able to navigate better in the complexities of accounting and help to create more transparent and reliable financial systems.

Get more well researched information about the Normative vs Positive Accounting Theories here.