Introduction

Financial risks affect all organizations, large and small, across all sectors, and can have a detrimental effect on financial stability and reputation. Proper safeguards will prevent major losses from fraud, theft, accounting mistakes, unauthorized transactions, or financial mistakes. Many companies are very concerned about creating revenue and boosting sales but at times overlook the systems which would safeguard the resources that they have. The safeguards are provided through internal controls, the policies and procedures put in place to ensure that financial activities are conducted in a proper manner, assets are protected, and financial reports are accurate and reliable.

In recent years, the need for internal controls has become much greater as a result of regulatory demands, technology and more sophisticated methods of fraud. Nowadays, organizations are required to be transparent, accountable and have good risk management practices. Internal controls are part of a solution that can help organizations accomplish these objectives by limiting opportunities for fraud and financial mismanagement, increasing efficiency and compliance. Companies that emphasis the development of robust control systems will be better equipped to safeguard their funds, foster investor confidence and contribute to long-term growth.

Internal Control Systems: Understanding the Systems of Internal Control.

Internal control systems are policies, procedures and practices used by an organization to protect its assets, to ensure adequate and accurate accounting of assets, to enhance the efficiency of operations and to comply with laws and regulations. These controls are throughout the organization (covering senior management to operational staff). Their role is not only to catch errors post occurrence, but to prevent issues before they even happen as well as to catch issues early when they do.

Various internal controls are used by different organizations based on the size, type of business and the level of risk. Preventive controls are intended to prevent errors and frauds from occurring, and detective controls are intended to detect errors and frauds that have occurred. Corrective controls are those that are concerned with addressing a problem that has been identified and trying to prevent it from happening again. To learn more about internal control systems, organizations can explore internationally accepted frameworks and best practice that help in the accountability and financial integrity.

A functional internal control framework fosters an attitude of responsibility and transparency in an organization. Employees know their duties, management has the right information for decision making and has confidence in the way the organization works. These controls can prevent businesses from suffering financial losses, inefficiencies and reputational damage which can be hard to overcome if they are not in place.

The objectives of Internal Controls

A key goal of internal controls is to ensure that the assets of the organization are not stolen, misused or accessed without authorization. This includes money, stocks, equipment, patents and trade secrets, and other critical assets that need to be safeguarded. Internal controls are procedures put in place to handle these assets to make sure the assets are in the hands of authorized persons and that they are monitored and documented.

An additional key goal is to ensure that financial data is accurate and reliable. Financial reporting plays a crucial role in making key decisions for investors, lenders, management teams and government agencies. Financial data errors can result in bad business decisions, fines from regulators and loss of trust from investors and stakeholders. The internal controls are designed to facilitate the proper and accurate recording of transactions, adequate documentation and review prior to the incorporation of transactions into the financial statements.

Internal controls also enhance efficiency of operations by establishing uniformity of operations and eliminating duplication of effort. Knowing what is expected of them and what they have to do makes their work more effective. Additionally, effective controls help organizations meet regulatory and compliance requirements, such as tax laws, accounting standards, and industry-specific regulations, minimizing the likelihood of penalties and legal issues.

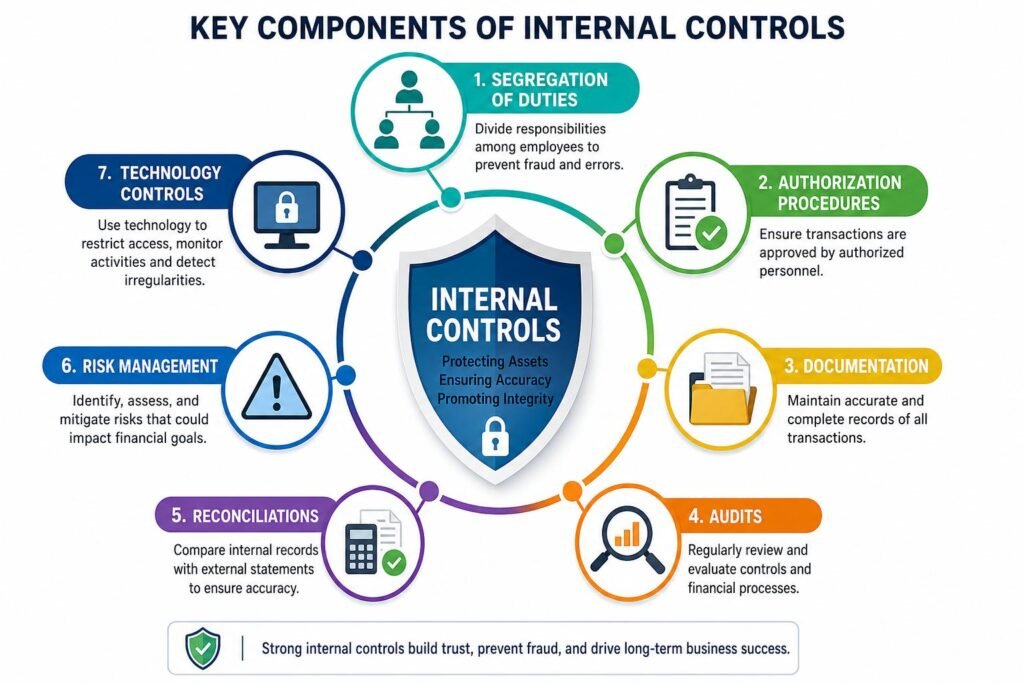

Segregation of Duties

Internal control is one of the most important principles of segregation of duties which help to minimize the opportunities for fraud and error. The idea is for the funds to be split among different people in such a way that no one worker is tasked with the entire transaction chain, from start to finish. When tasks are broken down into their components, it’s hard to carry out any fraudulent activities without being caught.

In fact, the person who approves purchases shouldn’t have access to making payments or reconciling bank statements for instance. Likewise, the cash receipts person should not be responsible for the accounting records pertaining to these cash receipts. With more than one employee involved in different parts of a transaction, there is a reduced risk of errors and intentional misconduct.

But in small businesses, due to the limited staffing, it is difficult to implement full segregation of duties. But other measures like management review, owner review and periodic external checks can offer further safeguards. In small organizations, the separation of authorization, custody and record keeping functions is necessary for good financial management, even if the functions are performed by only a few people.

The Procedures for Authorizing and the Controls for Approving

By implementing authorization procedures, financial transactions are only carried out when granted authorization from individuals with the right permissions. All organizations should have clear approval structures, defining who can approve purchases, payments, payroll changes and capital expenditures. Such processes help avoid unlawful expenditures and promote the proper utilization of the organization’s resources.

Approval controls are particularly critical in high value transactions and activities where there is a high financial risk. For large purchases or contracts, organizations may need several levels of approval to ensure that they are properly managed and if the transaction is for a larger contract, it is aligned with the strategic objectives. The same processes also help create accountability as management is able to trace back and find out from whom a transaction was originated and if there was compliance with the policies.

In recent times, accounting systems have enhanced the process of authorization with electronic workflows and digital tracking of approvals. These systems track all approvals made and create documentation which can be audited or investigated. This transparency prevents fraud and promotes financial governance in the organization.

Proper Documentation and Record Keeping

Documenting is a major part of the internal controls since it gives evidence that transaction does take place and it’s processed appropriately. An audit trail is established from documents like invoices, receipts, contracts, purchase orders, payroll records and bank statements, which helps financial reporting and accountability. Documentation is essential for organizations to prove transactions and/or provide protection during the inspection.

Good record keeping also provides for better operational continuity and efficiency. Staff can change jobs and organizations, and there are records and procedures in place to ensure the information is not lost. Unified documentation procedures facilitate training and lessen the chances of inconsistencies in monetary procedures.

Documentation is also often important for regulators and auditors to review as part of their investigation of compliance with accounting standards and laws and regulations. Having organized and complete records will help to prepare for audits and will minimize disagreements over financial transactions. Good documentation is thus directly linked to transparency of the finances and with the effectiveness of the operation.

The Role of Audits

Audits are a critical part of the process in determining the effectiveness of the internal controls and areas that need improvements. Internal audits involve employees or departments doing the auditing and external audits are done by independent parties who have no connection to the organization that are hired to give unbiased views on the financial records and reporting systems.

Auditors test and analyze if the procedures are working as they should. They review documentation, verify transactions and evaluate compliance with policies and regulations. They can have the ability to uncover weaknesses that management might not have known about, enabling organizations to beef up controls prior to the onset of significant issues.

Regular audits also deter bad behavior since employees are aware that there are chances for their financial activities to be reviewed. Organizations that do periodic audits reflect their commitment to accountability and transparency, helping to build investor, customer, employee and regulatory confidence.

Financial Accuracy and Reconciliations

Reconciliations are the process of verifying that the internal financial records matches with the external records and is consistent and accurate. One of the most frequent examples are bank reconciliations, which involve analyzing the accounting records with bank statements to find discrepancies and come up with resolutions in a timely fashion.

Reconciliation can help identify unauthorized transactions, duplicate payments, recording errors and missing payments that could be hidden. It’s important to address these issues early on to avoid financial losses and ensure the reliability of the information presented in financial reports.

While monthly recon is the norm, companies with large number of transactions might do more frequent reconciliations. Reconciliations are useful for cash management, for better financial control and to aid accurate financial reporting when they are done at the right time. An integral part of an effective internal control system.

Risk Management Practices

Risk Management is the process of recognizing, assessing and addressing events that have the potential to impact negatively an organization’s goals. There are risks to deal with, such as financial fraud, cyber-attacks, operational disruptions, regulatory changes and human error.

Internal control helps to mitigate risk, through the likelihood and impact of adverse events. There is a need to perform risk assessment periodically in the organization to identify areas which need protection and monitoring. This positive strategy provides the management with a successful use of resources and enables them to allocate resources to the most threatening issues.

Risk management is a continuous process and not a single event, it adapts to the changing dynamics in the business environment with the growth of business. Continuous risk assessments and control changes have the potential to make organizations better prepared for new challenges and financial stability.

The Use of Technology and Automated Controls

The advent of technology has revolutionized the internal controls, adding an element of automation and real-time monitoring. Restricted user access, electronic approvals, audit trails and flagging of unusual transactions for investigation are all possible features of accounting software that can limit users’ ability to access what they’re supposed to be accessing. All these features are known to boost efficiency, and minimize human error.

Additionally, automated controls facilitate segregation of duties by restricting access to certain functions according to job duties. Employees will only be able to carry out work that is appropriate to them and will not have the opportunity to do any activities that they are not supposed to. In addition, digital records provide valuable information for audits and management reviews.

As more transactions and data are conducted online, and more systems are being placed in the cloud, cyber security is an increasingly important part of internal controls. To guard against unauthorized access and cyber threats, organizations need to implement various security measures, including using robust passwords, multifactor authentication, software updates, and encryption.

Challenges in Implementing Internal Controls

Although internal controls are beneficial, companies can experience difficulties in placing the controls. The division of duties is not always possible or effective in small businesses, or may be difficult in larger businesses with several locations and departments. However, these pragmatic constraints can make implementation more complex and ingenious solutions are necessary.

Finally, employee resistance can be a problem if they don’t see the controls as a means of protection but as unnecessary bureaucracy. Management needs to make it clear that internal control is meant to assist the employees and to ensure that the business is protected and not to limit productivity. Through training and consistent communication, employees can be made aware of the importance of compliance and foster cooperation.

Another frequent issue is the cost factor. The barriers to implementation of control systems are some organizations are reluctant to invest in control systems due to implementation costs. The cost of fraud, however, is often greater than the cost of prevention, in terms of loss of reputation as well as financial loss. Internal controls are then investments in stability and not a cost to be avoided.

Best Practices for Strengthening Internal Controls

The first step towards improving internal control is to foster a culture of ethics among employees, which can start at the top with management. When leaders are seen to be responsible and honest in their conduct, employees are more likely to be responsible and accountable with policies and procedures. Ethical leadership sets expectations that prevent, reduce, and deter wrongdoing and nurture responsible financial practices.

Routine training is also a must as workers need to be familiar not only with the control devices, but also their purpose. Employees who are alert to signs of fraud and know how to report it to the appropriate person can play a major role in an organization’s fight against financial fraud.

Internal controls are monitored on an ongoing basis and evaluated periodically to keep the controls effective. Policies need to be reviewed on a regular basis, procedures need to be updated as needed and action needs to be taken swiftly on the weaknesses identified. Whistleblower programs, data analytics and performance monitoring can also offer further insights that will help to reinforce good governance and risk management.

Conclusion

Internal controls are a key element in any organization’s ability to keep fraud and financial mismanagement at bay. The principles of segregation of duties, authorization, documentation, audits, reconciliations and risk management can help to safeguard assets and enhance the trustworthiness of financial data. Effective controls can minimize financial losses, enhance operational efficiency and aid in regulatory compliance.

Lack of commitment by leadership and employees is the one thing that will hinder the success of internal controls. Those organizations that treat controls as an investment, rather than a burden on administration are more likely to realize long-term financial stability and sustainable growth. Ensuring ongoing risk assessment and risk reduction will foster a sense of responsibility and transparency within the business that will help to safeguard stakeholders and drive future success.

Get more well researched information about internal controls for fraud prevention here.