Introduction

The concept of theory in accounting is a fundamental idea that is often misunderstood or oversimplified in academic and professional discussions. Theory is often thought to be an abstract concept that is of little relevance in practice, but this is the last thing that people think about, particularly in such areas as accounting. It is critical to comprehend the general meaning of theory since theory is a cornerstone on which knowledge is developed, tested, and applied.

Concept of theory in accounting does not just constitute a set of assumptions as it is an organized set of ideas that define how financial information is recognized, measured and reported. It assists in making of decisions, allows consistency and makes the financial statements to be meaningful and reliable. This article discusses the essence of theory, its features and framework, and its importance in the accounting practice and research.

To have a more thorough understanding of what is meant by this concept, you can canvass this step-by-step guide as to the general definition of theory and the application of theory in various fields.

What is Theory?

A theory is essentially an organized explanation of phenomena, which is founded on observation, evidence as well as logical reasoning. It is not merely ideas or guesses, but it presents a systematic framework, which assists us to perceive the relationships between various variables or concepts.

The overall definition of theory may be summarized as the following:

- A complex of mutually connected ideas and suggestions.

- Theories are meant to describe and forecast phenomena.

- According to facts and reasonable arguments.

- Open to experimentation and improvement.

Theories unlike opinions are formulated in a rigorous way that includes observation, formulations of hypothesis, testing, and validation. They offer a credible foundation of knowledge on the dynamics of complex systems and informed decision-making.

Key Theory Characteristics

In order to realize the very concept of the theory, it is significant to consider the features by which the concept is outlined. These characteristics make theory separate out of the casual assumptions or unverified beliefs.

1. Systematic Structure

A theory is not arbitrary, it is structured in a rational and consistent way. The ideas in a theory are linked together to create a systematic process in explaining a certain phenomenon.

2. Based on Evidence

Theories are based on empirical evidence. They are derived out of observation, experiment and analysis and are made as much a reality as possible.

3. Predictive Capability

Prediction of outcomes is one of the most significant characteristics of a theory. A good theory is not only an explanation of what has occurred-it is also an assist in prediction of what could occur given some conditions.

4. Testability

Theories must be testable. This implies that they can be tested using research and experimentation. A theory may be adjusted or substituted in case new evidence refutes it.

5. Generalization

Theories are dynamic enough to be applicable in a wide range of situations. Although they might not be applicable to each and every case, they do give broad principles that can be extensively applied.

6. Dynamic Nature

Theories do not remain the same; they change. Theories are modified at every new information to enhance their precision and applicability.

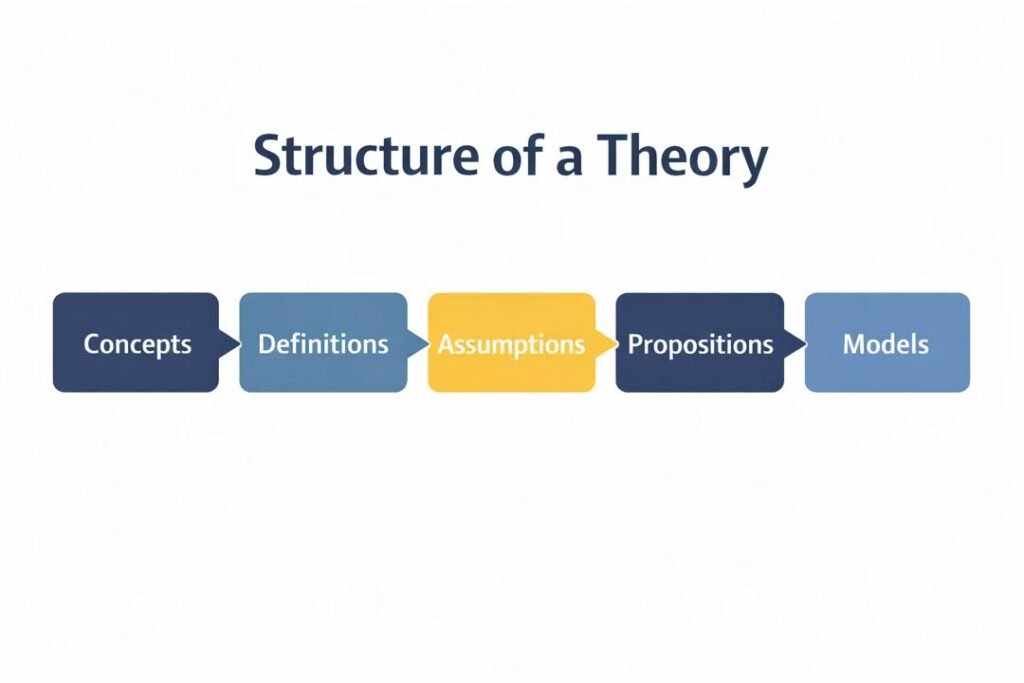

Structure of a Theory

A properly formulated theory usually has a number of essential elements:

- Concepts: Theories are made up of concepts. They are the basic concepts or variables in question.

- Definitions: Clarity will guarantee that the concepts are understood in the same way. Theories may lose their meaning without specific definitions.

- Assumptions: Assumptions are propositions made that are considered to be true in the theory. They give a point of departure of analysis.

- Propositions: Propositions express the connections amongst concepts. As an example, a proposal can be made on how one variable, on the increase, is related to a change in another.

- Models: Models are simplified versions of reality that explain the mechanism of action of a theory. They are used to comprehend and practice theoretical knowledge.

Role of Theory Knowledge Development

Theories have a dominant place in knowledge development in all fields. They are the basis of research, study and practice.

1. Organizing Knowledge

Theories are useful in organizing large volumes of information in the form of a unified entity. Complex phenomena can be easily understood.

2. Guiding Research

The theories are used by the researchers to develop hypotheses and design studies. Research would be shapeless without the theory.

3. Explaining Phenomena

Theories give reasons as to how things occur as they do. This is critical in knowing about background reasons and interconnections.

4. Supporting Decision-Making

Professionally, theories have directives in decision-making as they provide effective guidelines to make judgments.

5. Encouraging Innovation

Theories promote research and innovations since they help in identifying gaps and limitations. They stretch the limits of knowledge.

Understanding Accounting Theory

The concept of theory in accounting represents a specific application of the overall notion of theory. It pays attention to the principles and assumptions that would inform the preparation and presentation of financial statements.

Simply, accounting theory would offer a guideline to answering some of the most important questions like:

- What ought to be included in financial statements?

- What should be the metrics of transactions?

- At what time do you consider revenue or expenses?

- What is the presentation of financial information to be?

These questions are important since they influence the way businesses report on their financial performance and position.

Importance of Accounting Theory

The accounting profession is supported by accounting theory. Its significance can be described in a number of significant aspects:

Ensuring Consistency

The accounting theory encourages the uniformity of financial reporting. It offers standardized principles thus rendering the financial statements of various organizations comparable.

Enhancing Reliability

Theoretical systems make the financial information to be accurate and reliable. This creates confidence to the stakeholders like investors, creditors and regulators.

Guiding Professional Judgment

Accountants are in a position to deal with situations that involve making judgments. The accounting theory offers a set of rules that assist practitioners in making adequate choices.

Helping with Policy Formulation

Accounting theory helps regulatory authorities to come up with accounting standards and policies. These standards provide that financial reporting is legal and ethical.

Facilitating Communication

Communication takes place through financial statements. The accounting theory makes this communication meaningful, clear and consistent.

Theoretical Frameworks in Accounting

A theoretical framework in accounting is a systematic framework that describes concepts and principles of financial reporting. It is used as a guide to the setting of accounting standards and practices.

The major components of an accounting theoretical model are:

- Financial reporting objectives.

- Useful information qualitative properties.

- Meaning of the elements of the financial statement (assets, liabilities, equity, etc.)

- Criteria of recognition and measurement.

These aspects make sure that financial data is relevant, reliable and comparable.

Role of Theory in Accounting Practice

The concept of theory in accounting is not a mere academic one. It has real-life applications in normal accounting practices.

- Financial Reporting: Theories inform the preparation of financial statements and in this way, they ensure that there is adherence to the set standards.

- Auditing: Auditors use the accounting theory to evaluate the fair presentation of the financial statements.

- Taxation: The theories are important in determining the recognition of income and expenses to be taxed.

- Management Decision-Making: According to the theory, managers utilize the information in accounting to make strategic decisions.

Theory and Prediction in Accounting

The predictive ability of theory is one of its most useful elements. In accounting, this means:

- Predicting financial performance.

- Projection of future cash flows.

- Evaluation of risks and uncertainty.

As an example, the theories associated with revenue recognition can be used to determine when the income is earned and reported. This plays an important role in decision-making and planning.

Challenges and Criticisms of Theory

Although it is important, theory does not lack problems:

- Complexity: Theories are often complicated and hard to grasp particularly by beginners.

- Limitations: There are no situations that can be explained by all the theories. Exceptions and special cases always exist.

- Changes in Environment: Existing theories can become irrelevant to the changes in the economy and in technology.

- Subjectivity: This is because there will be elements of judgment in some areas of theory and this may result in varied interpretations.

Nevertheless, these issues do not undermine the importance of theory; on the contrary, they emphasize the necessity of constant improvement and changes.

The Evolution of Accounting Theory

The theory of accounting has been changed considerably. The accounting that was practiced early had the basis of basic record-keeping in mind and the current accounting has complicated structures and regulations.

Key developments include:

- Implementation of standard principles of accounting.

- Conceptual framework development.

- Highlighting more on transparency and accountability.

- Adoption of technology in accounting procedures.

This development shows how theory has been a dynamic field that is flexible to meet the evolving demands.

Relevance of Theory in Modern Accounting

The accounting theory is more relevant than ever in the world we live in today that is globalized and technologically advanced.

- Global Standards: International accounting standards are based on theories that allow business to operate internationally.

- Advancements in technology: The more accounting systems get automated, the more theory would guarantee that technology is implemented in the right way.

- Ethical Considerations: Ethical theories establish a basis on how accounting should make ethical decisions.

- Data Interpretation: As the amount of financial information keeps growing, theory assists in the interpretation and analysis of information.

Conclusion

It is vital to know what theory means in general to be able to value its importance in the academic and professional setting. Theory is not an abstract concept only. It is an influential instrument that systematizes knowledge, interprets phenomena and informs decision-making.

Theory is a foundation of accounting. It guarantees uniformity, dependability and clarity of the financial reporting. It informs the use of professional judgment, aids in policy development, and offers the research and innovation framework.

The significance of the concept of theory in accounting will be increased as the business environment keeps changing. The knowledge and implementation of theoretical principles can help accountants and other stakeholders to make wise decisions, preserve trust, and positively influence the financial system, helping it to stand and develop.

Finally, theory is filling the knowledge-practice gap and, thus, is an unavoidable part of accounting as well as other areas.

Get more well researched information about the Concept of Theory in Accounting here.