Introduction

Mastering double-entry system, as a small business owner, student of accountancy, or a person that wants to get a hold of how financial records work is a key concept you must grasp. It supports accuracy, transparency and also helps in the early detection of errors which may otherwise blow up into large scale problems.

The double entry system’s appeal is in its ease and logic each financial transaction affects at least two accounts. This dual action creates a self-contained system which in turn produces reliable and full financial reports.

To see how this plays out in practice we will go through the concept step by step which includes rules for debits and credits, common transaction entries, and how errors are identified and we also look at a deeper breakdown of the double entry system as we go through the article.

Understanding the Double-Entry System

Definition and Core Principle

In the double entry system every transaction is recorded in at least two accounts. We post to one account which goes up (debit) and another which goes down (credit) thus the accounting equation is always kept in balance:.

Assets = Liabilities + Equity

This principle forms the base of what we do in accounting. Outwardly every transaction has to fit into this balance which is what makes the double entry system so effective.

Reason It Matters

Without that system in place financial records would become very quickly untrustworthy. For example of not recording an increase in revenue from a cash sale your books will not reflect the true performance of your business. The double entry system corrects for this by including a corresponding entry for each action.

Understanding Debits and Credits

In many cases the most important element of mastering double entry system is to see how debits and credits play out. What is less known is that which of these terms applies in a given situation is not as simple as a general “increase” or “decrease”. Rather it is based on the type of account we are dealing with.

The Five Main Account Types

- Assets: which a company owns (cash, equipment, inventory).

- Liabilities: Outstandings (loans, accounts payable).

- Equity: Owners share of the business.

- Revenue: Income earned

- Expenses: Costs incurred Expenses Outlays of money for which the company is responsible.

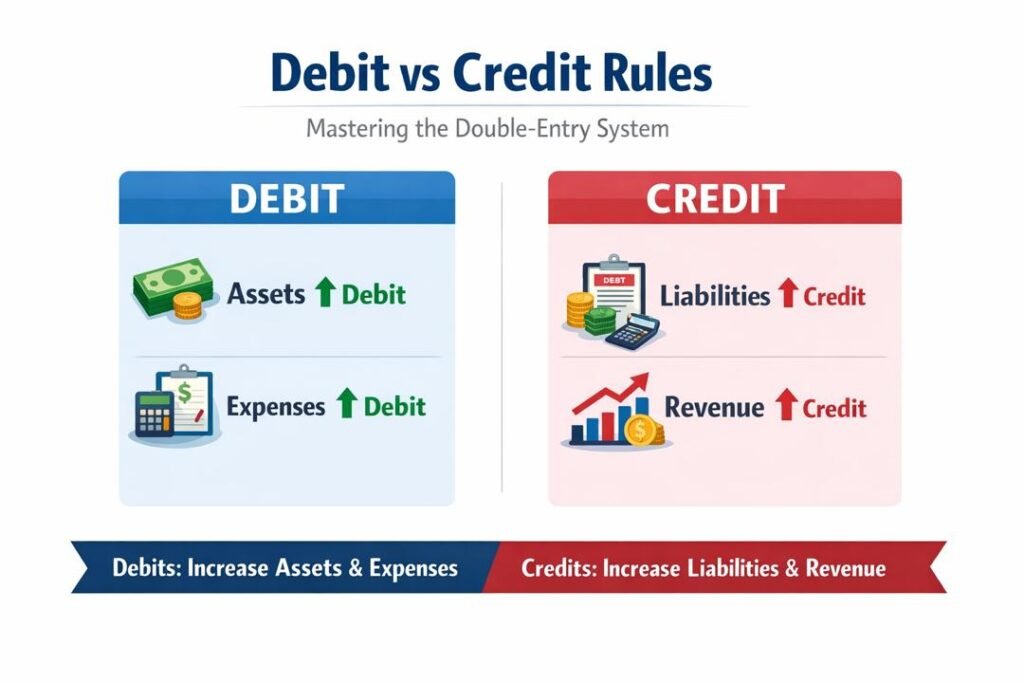

Debit and Credit Rules (Explained Simply)

- Assets: Record with a debit and for a credit reduces.

- Liabilities: Increase by credit and decrease by debit.

- Equity: Add with credit and reduce with debit.

- Revenue: Increase by a credit and decrease by a debit.

- Expenses: Add with a debit and reduce with a credit.

A Simple Way to Remember

- Debits increase the business’s assets and expenses.

- Credits to what a business owes or has (liabilities, equity and revenue).

Application of Double Entry System

Let’s take a look at the structure of the double entry system in which we record transactions.

Example 1: Founding a Business.

You put in ₦500,000 of your own money into your business.

- Debit: Cash (Asset) $500,000.

- Credit: Capital (Equity) $500,000.

Explanation: Summary

Your business reports an increase in cash (asset growth) and at the same time your ownership stake (equity) goes up.

Example 2: Purchasing Equipment for Cash.

You bought equipment for ₦100,000 in full price.

- Debit: Assets (Equipment) ₦100,000.

- Credit: Cash (Asset) ₦100k.

Explanation: Exposition

One piece of equipment goes up while at the same time cash goes down.

Example 3: Making a Transaction.

You sell your products for ₦50, 000 in cash.

- Debit: Cash (Asset) ₦50k.

- Credit: Revenue of ₦50, 000.

Explanation:

Cash increases, and income is recognized.

Example 4: Covering Costs.

You pay rent of ₦20,000.

- Debit: Payment of rent of ₦20, 000.

- Credit: N20, 000

Explanation:

Expenses increase, while cash decreases.

Example 5: Using credit which also includes buying present and paying for it later.

You go out and buy goods that which you are to pay for at a later date in the amount of ₦30,000.

- Debit: Inventory (Asset) $30,000.

- Credit: Accounts payable (Liability) ₦30,000.

Explanation:

You get inventory but at the same time take on a liability.

The Role of the Accounting Equation

In the double entry system of accounting the accounting equation is always balanced.

Let’s revisit an example: Here is another example of:

Transaction: Buy out of pocket for ₦100,000.

Before: Sure, please provide the text you would like me to paraphrase.

- Assets = ₦500,000

- Liabilities = ₦0

- Equity = ₦500,000

After: Post:

- Assets ₦500,000 (cash down, equipment up).

- Liabilities = ₦0

- Equity = ₦500,000

The balance remains intact.

Journals and Ledgers: At What Point Do We Record.

The Journal (Book of Original Entry)

All transactions are put into a journal. Per entry which includes:.

- Date

- Accounts affected

- Debit and credit amounts

- Description

The Ledger

After which point journal entries are put into the ledger in which each account is given an entry of its own.

For example: For instance:.

- Cash account

- Revenue account

- Expense account

This helps track balances over time.

Trial Balance: Evaluating Accuracy.

At the close of an accounting period we prepare a trial balance which:

Total Debits = Total Credits

If so they are mathematical right.

Also it is not to say that all errors are removed one may still be present.

Common Errors in the Double-Entry System

In spite of having a structured system errors do happen which we do better to understand for the purpose of detection and correction.

1. Error of Omissions

A transaction is completely left out.

Example: Omitting to record a sale.

2. Error of Commission

Mistakes of which to do which I will not rephrase as it is a legal term “Errors of Commission” typically refers to a decision by a tribunal or administrative body which is found to be in error. Recording into the wrong account, the right amount

3. Error of Principle

Violating accounting rules

Example: Recording a fixed asset as a revenue item.

4. Compensating Errors

Two errors cancel each other out.

5. Errors of Transposition

Digits are out of order (e.g. ₦54,000 instead of ₦45,000)

How the Double Entry System Prevents Errors.

The system provides several checkpoints: The system has many checkpoints:.

- Balance Sheet Report: If there is a difference between debits and credits an error exists.

- Suspense Account: Used for when differences are not at once apparent.

- Reconciliation: Reviewing records against external sources (e.g. bank statements).

- Logical Analysis: Analyzing whether entries make sense.

Advantages of the Double-Entry System

- Performance Accuracy: Ensuring all transactions are recorded.

- Fault Detection: Makes it easier to identify mistakes.

- Financial transparency: Provides a complete financial picture.

- Prevention of fraud: Difficult to manipulate records without detection.

- Normalization: Widely accepted across the world.

Limitations of the Double-Entry System

Although very good at what it does the system is not perfect.

- Complexity: Beginners may find it confusing.

- Time out of the question: Requires careful recording of every transaction.

- Cannot detect all mistakes: Some mistakes (such as omission) go by undetected.

Practical Guide to Proficiency in the Double Entry System

- Get to know the account types first: Before you memorize the rules, see how the accounts act.

- Practice often: Work through examples daily.

- Use memory aids: For example: For instance:

DEA-LER

- Dividends, Expenses, Assets in the red

- Liabilities, Equity, Revenue go up.

- Go over the entries again: Always review your work.

- Use accounting software: Tools which do that is Excel or accounting applications.

Real-Life Application

The double-entry system is used in: In the double entry system which is used in:.

- Small businesses

- Corporations

- Banks

- Government institutions

In this system all financial reports, balance sheets, income statements, and cash flow statements depend.

From Transactions to Financial Statements

The process flows as follows: The process goes as follows:

- Record transactions in journals Record into journals.

- Post to ledger accounts, post to account books.

- Prepare trial balance Prepare trial account balance.

- Adjust entries Amend entries.

- Create financial statements Create financial reports.

- Each step is based on the double entry principle.

Conclusion

The double entry system is not the only accounting tool that is not enough to call it what it is, it is the base of modern financial reporting. Through which each transaction is recorded in at least two places it also serves as a control which produces reliable results.

Once you understand the debits and credits you will find the system to be less daunting and more logical. Through consistent practice you are able to confidently post transactions, catch errors, and keep financial records in balance.

Mastering the double-entry system also improves your bookkeeping skills which in turn gives you a better picture of how businesses do in terms of finance. For students, entrepreneurs and professionals alike this info is a must have to do well in the world of accountancy. The double-entry system also builds discipline and accountability in financial management. It encourages careful thinking, reduces the risk of oversight, and supports better decision-making.

Get more well researched information about Mastering the Double-Entry System here.