Introduction

Accounting is not just some numbers recording, but it is a systematic organization that is aimed at guaranteeing the accuracy, reliability and transparency in reporting of financial statements. Preparation of the trial balance, reconciliation of the bank statements, and proper classification of the capital and revenue items are among the most significant control and classification mechanisms in accounting. These are checks that serve as protective measures in the accounting cycle and they assist organizations to identify mistakes, fraud and present financial statements in accordance to the developed standards including the International Financial Reporting Standards (IFRS).

This article discusses these three important mechanisms in more detail, their purpose, procedures and their significance in ensuring financial integrity.

Trial Balance: Purpose and Preparation

Meaning of Trial Balance

A trial balance is a document which is prepared at the close of an accounting period and gives an accounting statement of all ledger account balances; the debit and credit. It mainly aims at ensuring that the mathematical aspect of the double-entry bookkeeping system is accurate.

With the double-entry system, two or more accounts are involved in any transaction, and a balance of debits and credits must be achieved. The trial balance determines the existence of this equality with the entry of journals to ledger accounts.

Trial Balance Objectives

The trial balance preparation can be used in a number of ways:

- Accuracy in arithmetic Testing: It ascertains that there are equal debit balances in total credit balances.

- Financial Statements Basis: Trial balance forms the basis of preparing income statement and statement of financial position.

- Detection of Certain Errors: Even though it is not able to detect every type of error, it aids in the detection of mistakes that include unequal postings, arithmetic mistakes, etc.

- Summary of Ledger Accounts: It provides a summary of all the balances in the account at a given date.

Format of a Trial Balance

An average balance sheet contains:

- Account names

- Ledger folio (optional)

- Debit column

- Credit column

At the statement bottom, total debits should be equal to total credits.

Steps in Preparing of a Trial Balance

The steps will include the following:

- Document transactions in books.

- Record the journal entries onto ledger accounts.

- Balance each ledger account.

- Record the accounts and the balances.

- Individual debit balances and credit balances.

- Equal both columns and assure equality.

In case of mismatch in totals, an investigation is required in order to identify and rectify errors.

Trial balance has limitations, as demonstrated below.

A trial balance is not able to identify all the errors though it is important. Examples include:

- Omissions (one that is not recorded at all)

- Mistakes of commission (sending to inappropriate account, but with appropriate amount)

- Mistakes of principle (expense should not be classified as an asset)

- The compensation of errors (two errors that act in opposite directions)

Therefore, it is a way of improving reliability but it is not a perfect assurance of accuracy.

Bank Reconciliation Statement

Meaning and Purpose

A bank reconciliation statement (BRS) is a document that is created to balance out the balance presented in cash book of the company with the balance presented in a bank statement. The discrepancies usually occur due to timing or mistake in recording.

The main effect of bank reconciliation is to have the company records of cash correct and in agreement with the bank records.

Causes of Differences

The discrepancies between cash book and bank statement can be as a result of:

- Outstanding Cheques: Cheques, which are not yet presented.

- Deposits in Transit: Deposits that are registered in the book of cash and are yet to be credited by the bank.

- Bank Charges: Fees taken off by the bank without warning.

- Direct Deposits or Standing Orders: Transactions conducted on the bank account.

- Dishonoured Cheques: Cheques returned unpaid.

- Errors: Errors in the bank statement or the cash book.

Bank reconciliation is important because it assists banks in managing their financial performance by detecting errors during their operations.

Bank reconciliation as a part of financial control is important:

- Fields out fraud and illegal transactions.

- Determines flaws in recording.

- Provider of proper cash reporting.

- Enhances internal control mechanisms.

- Has credibility amongst stakeholders.

Frequent reconciliation, typically once a month is a good practice in managing finances.

Bank Reconciliation Statement Preparation Procedure

The steps that are followed are usually the following ones:

- Obtain the bank statement.

- Check every item in the cash book against the bank statement.

- Identify unmatched items.

- Record omissions to the cash book e.g. bank charges or interest.

- Make the reconciliation statement with provision of outstanding cheques and transit deposits.

- Ensure that the adjusted bank balance is equal to the adjusted cash book balance.

Bank Reconciliation Statement Form

It can begin with either the following:

- The balance according to cash book, or

- The balance according to bank statement.

There is then an addition of adjustments or deductions to reach the respective balance.

Role in Enhancing Financial Accuracy

Bank reconciliation forms an internal audit system. It minimizes the possibility of poor cash management and gives confidence that financial books are a true reflection of bank activity. Reconciliation can be done automatically in modern accounting systems although professional review is critical.

Revenue and expenditure are classified as detailed below:

Proper categorization of receipts and expenditures is essential in proper financial reporting. Mismatch may distort the profits and present falseness of financial position.

Classification of Revenue and Expenditure

Capital Receipts

Capital reception are the money that is received but do not belong to the normal business income. In general, they lead to either:

- A liability (e. e.g. loan received), or

- A decrease in assets (e.g. sale of fixed asset).

Examples include:

- Issuance of shares proceeds.

- Long-term loans received

- Sale of machinery

These receipts are found in the statement of financial position.

Revenue Receipts

Normal business operations give rise to revenue receipts. They add to revenue and profits.

Examples include:

- Sales revenue

- Commission received

- Rent income

- Interest income

Income statement records the revenue receipts.

Capital and Revenue Expenditure

Capital Expenditure

The capital expenditure is one made to acquire or to improve the long-term assets. It has advantages not only within a single accounting period.

Examples include:

- Acquiring buildings or equipment.

- Installing cost of machinery.

- Major renovations

This capital expenditure is classified as an asset and it is depreciated.

Revenue Expenditure

Revenue spending is associated with daily running costs. It only gives advantage to the present accounting period.

Examples include:

- Salaries and wages

- Rent and utilities

- Repairs and maintenance

- Office supplies

Income statement charges are made to revenue expenditure.

Major Differences in Capital and Revenue Items

| Basis | Capital | Revenue |

| Nature | Long-term benefit | Short-term benefit |

| Frequency | Non-recurring | Recurring |

| Accounting Treatment | Recorded as asset | Recorded as expense |

| Impact | Affects financial position | Affects profit |

Importance of Proper Classification

Proper classification guarantees:

- Correct profit measurement

- Reasonable reporting of assets and liabilities.

- Adherence to the accounting standards.

- Sound financial analysis.

- Avoidance of Profit manipulation.

As an illustration, the inclusion of a capital expenditure as revenue expenditure understates profit and value of assets. On the other hand, the capitalization of revenue expenditure inflates the profits.

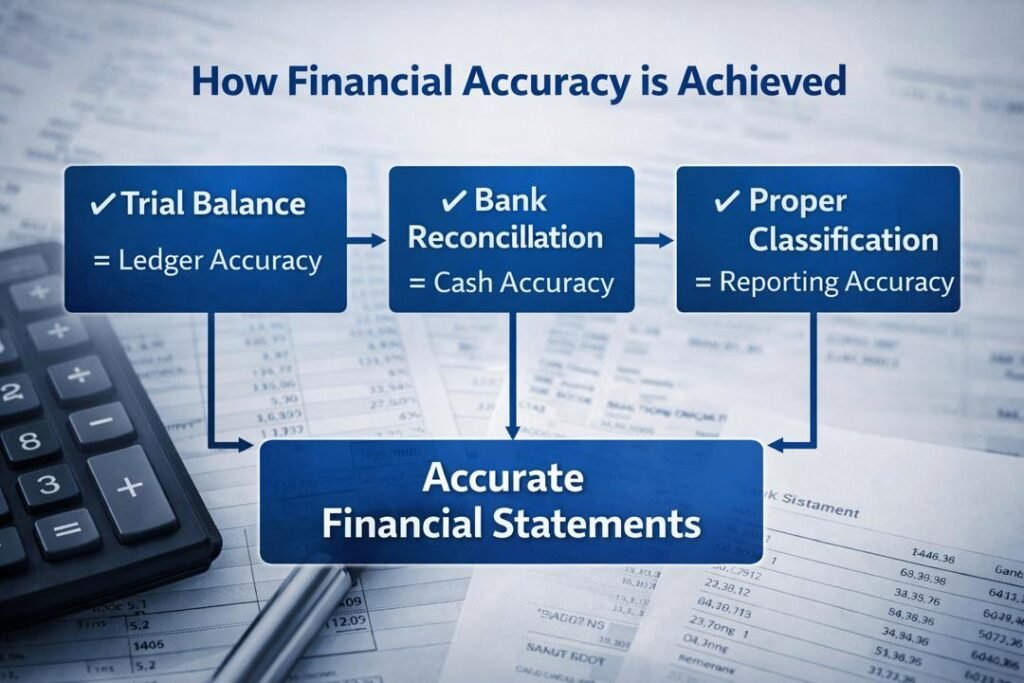

Integration of the Three Mechanisms

The trial balance preparation, bank reconciliation with the correct classification of revenue and capital items can be said to complement each other in increasing the accountability.

- The trial balance guarantees the accuracy of the ledgers.

- Balance check of the cash is ensured.

- Reporting accuracy is guaranteed through classification.

They constitute an effective internal control structure.

Financial statements should provide a true and fair view in compliance with the IFRS and other accounting systems. These mechanisms facilitate such an objective by reducing error and enabling proper recognition and measures.

Internal Control and Detection of Errors

These mechanisms play a major role in internal control systems by:

- Early detection of discrepancies.

- Reducing risk of fraud

- Promoting accounts review.

- Promoting accountability

For example:

- A trial balance imbalance is an indication of posting errors.

- Unauthorized withdrawals can be detected through a bank reconciliation.

- Wrong classification could reveal the intention to manipulate profit.

Therefore, they are not just accounting processes but they are also governance mechanisms.

Compliance with Accounting Standards

Global standards focus on proper measurement, recognition and reporting. Right classification guarantees compliance to:

- Matching principle

- Accrual concept

- Prudence concept

- Materiality principle

The inability to implement such mechanisms may lead to statements of induced financial reports, the fines, and the loss of trust in the stakeholders.

Conclusion

A trial balance, bank statement reconciliation and categorizing the items of capital and revenues are some of the pillars of financial control. Each of the mechanisms deals with another factor of accuracy:

- The lent and received account confirms the consistency of the ledgers.

- Bank reconciliation ensures the reliability of cash.

- The classification provides adequate financial presentation.

They work together to strengthen the internal control systems, increase transparency and adherence to accounting standards. These processes cannot be overlooked in a world where the financial integrity is paramount to the confidence of investors and sustainability of business.

Finally, good accounting requires more than documentation of transactions, but good control procedures and good classification principles. Organizations that keep repeating such mechanisms are in a better-position to generate credible financial statements, the errors are detected early and stakeholder confidence is safeguarded.

Get more well researched information about Trial Balance and Bank Reconciliation here.