Introduction

Financial reporting is important in enabling investors, managers, regulators and other stakeholders to make sound economic decisions. To be used as an effective purpose of financial information, it should have some properties that render financial information useful and reliable. The qualitative characteristics of accounting information explains the features that make financial information contained in financial statements more useful. These features comprise an important component of the conceptual framework prepared by the International Accounting Standards Board (IASB), which informs presentation and preparation of financial reports all over the globe.

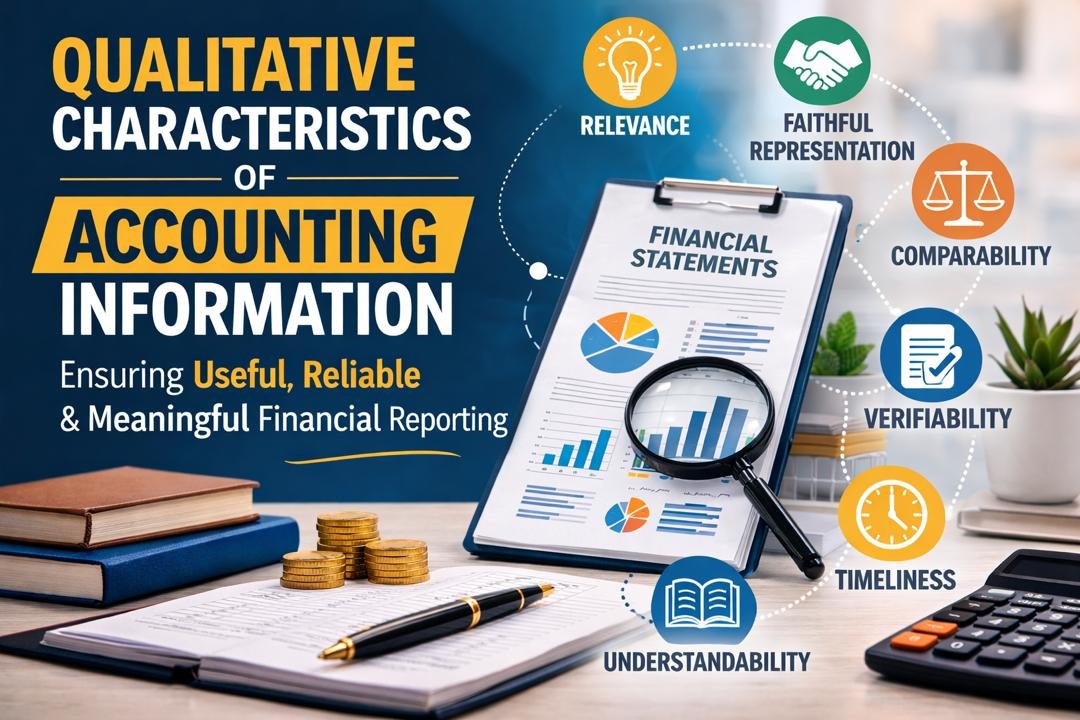

The usefulness of the accounting information is not considered as a simple presence; accounting information has to be represented in a form that will allow the users to comprehend it, compare, and depend on it to make their decisions. IASB states that there are two underlying qualitative characteristics of accounting information, namely relevance and faithfulness, and four supplementary characteristics, including comparability, verifiability, timeliness, and understandability. These together are the qualities that make financial reports informative and reliable of financial performance and position of an entity.

The article examines the essential qualitative characteristics of accounting information, the way they operate as part of the IASB conceptual framework, and shows their real-life significance in financial reporting.

The IASB Conceptual Framework

The idea framework given by the International Accounting standards board gives the theoretical tool through which accounting standards are created and the preparation of the financial statements. It establishes what financial reporting is, what the elements of a financial statement are, as well as the qualitative characteristics that render accounting information helpful.

The IASB feels that the original purpose of financial reporting is to contain financial information that can be useful to both current and prospective investors, lenders, and other creditors in making decisions on allocating resources to an organization. These users greatly depend upon financial statements to determine profitability, liquidity, solvency and whether a business could produce future cash flows.

The conceptual framework puts a lot of stress on the fact that information should be of a particular quality to achieve this goal. These standards are referred to as the qualitative features of accounting information.

Fundamental Qualitative Characteristics

Relevance and faithful representation are the qualitative characteristics that are given by the IASB. Without these two attributes, financial information would not be helpful in the decision making process.

Relevance

Relevance is the capacity of financial information to affect the decision of the users. Information is said to be relevant when it possesses predictive value, confirmatory value or both.

Predictive value refers to the fact that financial information can assist users to predict the future. As an illustration, shareholders can use historical revenue growth to project the profitability in the future. Confirmatory value is a scenario in which the past expectations are validated or rectified by financial information. As an example, in the case of a company realizing more than expected profits, the investors can reconsider their expectations regarding how this company would perform in the future. Relevance is also associated with materiality. The materiality of information is determined when omission or misstatement may affect the decisions of the users. That is, financial reports should only contain information that may influence decision-making.

As an illustration, when a big company inadvertently misrepresents a very minor amount of expenses, this might not have a great impact on the decision of users. The misreporting of large liabilities or revenue amounts would however be very material and would lead to misleading investors. Practically, accountants should critically decide what information becomes material and make it available in financial statements in the most accurate way.

Faithful Representation

Whereas relevance holds that information will have the ability to influence the decisions, faithful representation holds that the information will be a true picture of the economic reality of transactions. Accurate representation compels financial information to be full, unbiased and devoid of errors.

Completeness implies that all the required information to comprehend a transaction is contained. As an illustration, when a company records an asset, he/she should also provide pertinent information about the cost, depreciation pattern and useful life of the asset.

Neutrality refers to the fact that the information about finance must not be one-sided. Accountants should be objective in the presentation of data instead of using figures to make the company look better and more profitable or financially sound.

Lack of error does not imply that we will have perfect accuracy in all estimations. Rather, it implies the absence of any mistakes in the procedure involved into the creation of the information, as well as the clarity of the explanation of the estimates.

Faithful reporting is especially relevant in cases where accounting estimates are made like depreciation, impairment of assets or provisions of dubious debts. Such estimates should be made on grounds that are reasonable and have credible evidence.

Enhancing Qualitative Characteristics

After information meets the basic requirements of being relevant and faithfully representing, the IASB recognizes four other attributes that make information useful. They are comparability, verifiability, timeliness, and understandability.

1. Comparability

Comparability helps the users to recognize similarities and differences among financial statements of other companies or among financial statements of the same company but in different periods.

Companies in the same industry are usually compared by investors to identify the one that would give them a better investment. As an illustration, they can compare profit margins, the ratio of the returns on equity or ratios of liquidity between competing companies. Comparability when companies operate under similar accounting standards and methods, then comparability is attained. Introduction of International Financial Reporting Standards (IFRS) across the globe has greatly enhanced the comparability of companies in various countries in which they are involved.

Comparability contains the element of consistency. With the same accounting policies employed in a company across different periods, users can be able to tell the changes in the financial performance more precisely. In case of any change in accounting methods, the firm will be required to announce the change and the effects of the change.

Financial statements would be hard to compare since without comparability, financial statement users could not know whether the differences in financial performances are due to actual performance or merely due to different accounting methods.

2. Verifiability

Verifiability implies that the same conclusions may be made about financial information presented by independent observers. It guarantees that the information is true to the events happening in the economy which it alleges to capture.

Verification can be either direct or indirect. Direct verification refers to verifying an amount by direct observation, which includes physical inventory count. An indirect verification is one that confirms the verifications and calculations in which a reported figure is based on.

Auditing is very important in improving verifiability. The independent auditors analyze the financial statements with an aim of determining whether reporting has been done on the basis of accepted accounting principles and whether the information provided is sound.

As an illustration, the auditors can check the amount of revenues by inspecting invoices, contracts, and payment documents. In case the reported figures are backed by the evidence, users will be more confident in the financial statements.

3. Timeliness

Timeliness is defined as the financial information that is given to the users in time before they become useless in making their decisions. Too late information can be irrelevant anymore.

As an example, investors use quarterly and annual financial reports to assess the performance of the companies. When a company postpones publishing of its financial statements over a number of months, the information may be outdated and less valuable. Quick reporting helps the stakeholders to react promptly to any change in the financial position of a company. Financial reporting is usually subject to strict deadlines by the regulators to guarantee that the information is availed to the users in time.

Nevertheless, accuracy and timeliness usually have a trade-off. Preparation of the financial reports in a hurry can lead to more chances of mistakes and too much delay will only lessen the usefulness of information. The accountants are expected to balance these two considerations.

4. Understandability

Understandability implies that financial information ought to be put in simple and straightforward form to facilitate easy understanding of the information by the users.

Individuals have different levels of financial knowledge when it comes to use of the financial statements. Although the user should possess a reasonable level of knowledge in business and accounting, intricate information must be displayed in a manner that is understandable.

This means that one arranges information in a logical manner writes in simple terms and makes explanatory notes where the need arises. Clearance can be also improved by using graphs, tables and summaries.

But understandability should not be interpreted to mean that financial information is being oversimplified. There are certain transactions that are complex to begin with and it would be wrong to leave them out just to be able to present reports that are easily comprehended.

Thus, it is aimed at presenting rather than removing complex information.

Practical Implications in Financial Reporting

The qualitative nature of the characteristics which are provided by the IASB has far-reaching implications to the practice of preparing financial statements and their interpretation.

To start with, they direct accountants in choosing suitable approaches and policies towards accounting. Where there are several acceptable ways of accounting treatment, it is necessary to select the way that gives rise to more pertinent and accurate information.

Second, such attributes affect the degree of disclosure of financial statements. The companies should furnish adequate information to make it complete and transparent, have notes explaining accounting policies, estimates, and assumptions.

Third, they enhance the validity of financial reporting. Faithful representation of financial information when it is relevant, comparably, verifiably, timely and understandably makes users more likely to trust it.

Fourth, the attributes favour internationalization of accounting practices. As more and more people worldwide use IFRS, the IASB conceptual framework has offered a universal set of principles which will direct the financial reporting in various jurisdictions.

To illustrate, when multinational corporations are involved in more than one country, the preparation of financial statements is obligatory to meet the international standards. These reports are qualitative and thus can be useful to international investors and regulatory bodies.

Lastly, the features assist in avoiding financial manipulation and misrepresentations. By companies following these principles, it is harder to manipulate financial information with the aim of personal or corporate profit.

Challenges in Achieving Qualitative Characteristics

Though the qualitative characteristics present an understandable framework of how to create beneficial financial information, they may be difficult to do in reality.

Accounting estimates are used as a major challenge. A lot of items in financial statements including asset values and future liabilities provision are subjective. Such estimations should strike the right balance between relevancy and faithfulness.

The cost constraint is another problem. The process of preparing and presenting financial information is an expensive one since it entails data collection, data analysis and auditing. The IASB conceptual framework points to the fact that benefits of the provision of information must be more than the costs of producing information.

There is also the addition of globalization and the alteration of technology which accounts to the complexity of the financial transactions. The environment of accounting requires the accountants to keep changing their reporting practices so that they remain relevant, reliable, and transparent.

In spite of these issues, the qualitative characteristics are the key principles of upholding the integrity of financial reporting.

Conclusion

Qualitative characteristics of accounting information is a key aspect in the assurance that financial reports are used as they are supposed to be. These features are found in the IASB conceptual framework where they give a systematic method of assessing the usefulness of the financial information.

The useful accounting information is based on relevance and faithful representation, which means that information affects decision and is representative of the economic reality. Financial reports can also be enhanced in terms of characteristics, such as comparability, verifiability, timeliness, and understandability, which also increase the usefulness of financial reports as they can be easier to analyze, confirm, and interpret. These attributes combine to enhance the credibility, transparency and reliability of financial reporting. They also contribute to the internationalization of the standard accounting practices and assist the stakeholders in making sound economic decisions.

The qualitative characteristics of accounting information need to be observed in a more complex financial context, as only under these conditions one can preserve the confidence to financial reporting and make sure that financial statements help to draw a significant conclusion about the performance and the financial position of an organization.

Get more well researched information about Qualitative Characteristics of Accounting Information here.