Understanding production and costs is a key part of Economics, and it helps us see how businesses operate, make money, and make decisions. Let’s break it down in a simple way.

Types of Production

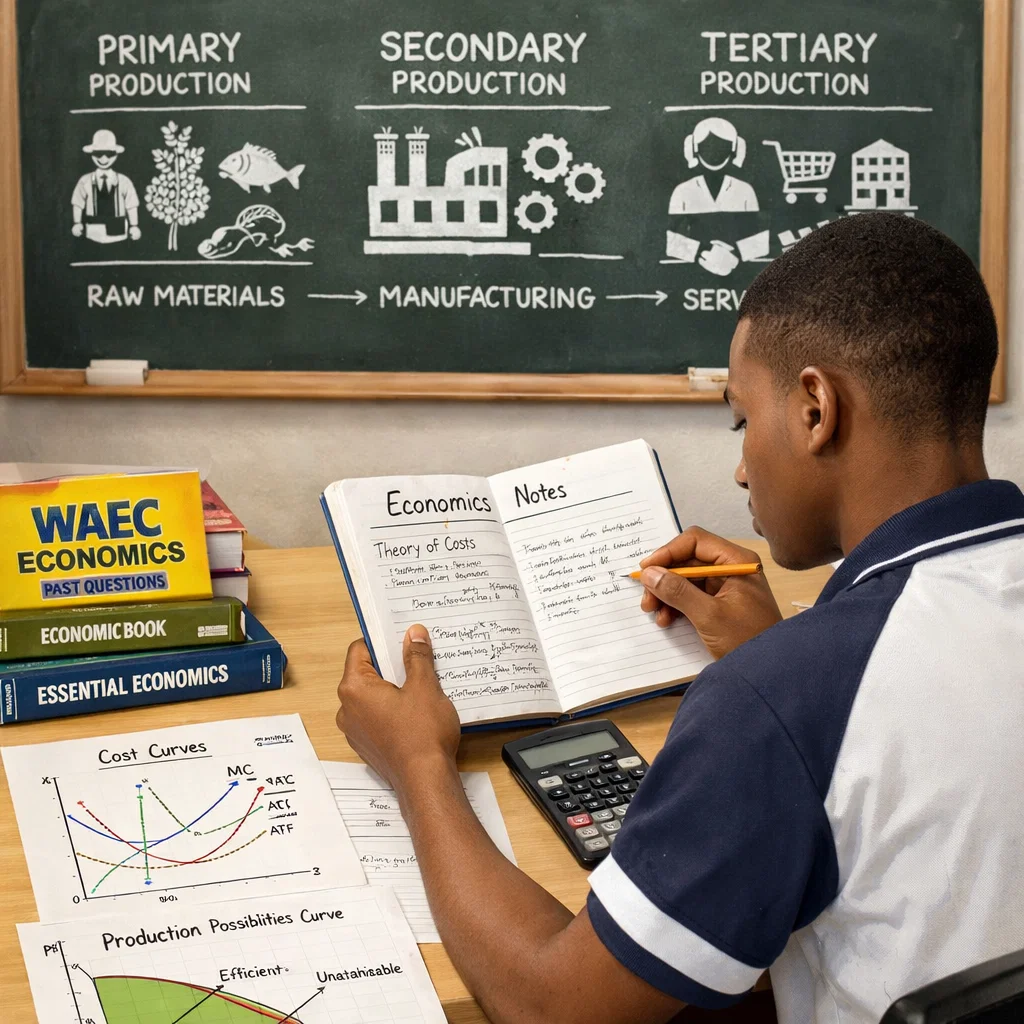

Production is the process of creating goods and services that people need or want. Economists divide production into three main types:

- Primary Production

This is the extraction of natural resources from the environment. Examples include farming, fishing, mining, and forestry. Basically, anything that comes directly from nature falls into this category. - Secondary Production

This involves turning raw materials from the primary sector into finished goods. For example, turning cocoa beans into chocolate or iron ore into steel. This sector is also called manufacturing. - Tertiary Production

This is the provision of services instead of goods. Examples include teaching, banking, transportation, and healthcare. The tertiary sector helps distribute goods and makes life easier, but it doesn’t produce physical items.

Short Run vs Long Run Costs

Businesses face different costs depending on how long they plan to produce:

- Short Run Costs

In the short run, at least one factor of production (like land, machinery, or buildings) is fixed. Businesses can only change some inputs, usually labor. Costs in the short run include:- Fixed Costs (FC): Costs that don’t change, like rent or salaries.

- Variable Costs (VC): Costs that change with production, like raw materials or wages for extra workers.

- Long Run Costs

In the long run, all factors of production can be changed. Businesses can expand, buy new machines, or move locations. There are no fixed costs in the long run, and firms can achieve economies of scale, where producing more can lower the cost per unit.

Marginal, Average, and Total Costs/Revenue

To make good decisions, firms must understand how costs and revenue behave as they produce more.

- Total Cost (TC)

Total cost is the sum of all costs a business incurs to produce a certain quantity of goods. TC=FC+VC - Average Cost (AC)

Average cost is the cost per unit of output. It tells businesses how much it costs to make each product. AC=QTCwhere Q = quantity produced - Marginal Cost (MC)

Marginal cost is the extra cost of producing one more unit of output. It’s important for deciding how much to produce. MC=ΔQΔTC - Revenue

Revenue is the money a firm earns from selling its goods or services.- Total Revenue (TR): Total money earned. TR=Price×Quantity

- Average Revenue (AR): Revenue per unit sold. AR=QTR

- Marginal Revenue (MR): Extra revenue from selling one more unit. MR=ΔQΔTR

Conclusion

Understanding production and costs helps WAEC students see how businesses decide what to produce, how much to produce, and how to make profits. Knowing the difference between primary, secondary, and tertiary production, short run vs long run costs, and marginal, average, and total costs/revenue is essential for both exams and real-life business decisions.

Master these concepts, and you’ll not only ace your WAEC Economics paper but also have a solid foundation for understanding how the economy works!