Introduction

Small business enterprises especially sole traders usually maintain minimal accounting records. They could keep records that are not full, i.e. incomplete records. Though the approach might seem easy and ease of use in small operations, it poses difficulties in formulating formal financial statements. However, accountants have devised methods of restoring financial information by Preparing Accounts from Incomplete Records and reliable reporting.

This paper provides technical tutorial on the preparation of financial statements, namely trading accounts, profit or loss accounts, and statements of financial position, with incomplete records. It further discusses some of the important adjustments like accruals, prepayments, depreciation and closing inventory that make the financial statements of the business to be true to the performance and financial position of the business.

Understanding Incomplete Records

Preparing Accounts from Incomplete Records involves an accounting system in which the entirety of transactions is not documented under the procedure of the double-entry method of bookkeeping. Most sole traders only document simple details which include cash receipts, cash payments and personal drawings. Accounts such as sales ledger, purchases ledger and expense accounts might be not maintained to the fullest.

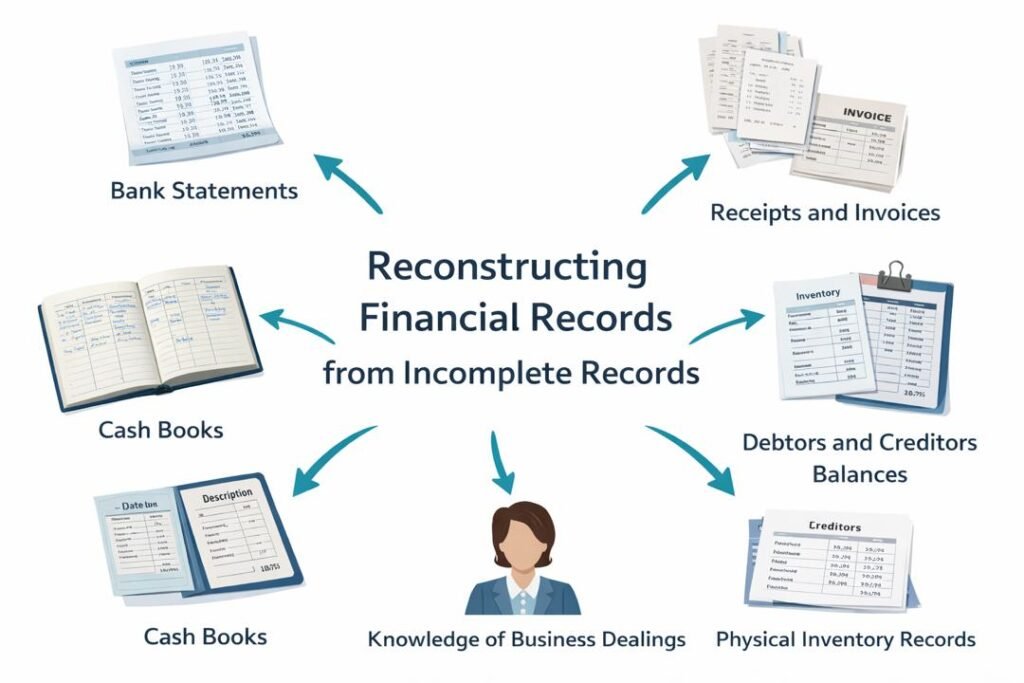

Due to these gaps, an accountant is required to recreate financial information based on the evidence at his disposal like:

- Bank statements

- Cash books

- Receipts and invoices

- Debtors and creditors balances

- Physical inventory records

- Having individual knowledge on business dealings.

These sources can enable the accountants to make approximations and reconstruct the required accounts.

Characteristics of the Single-Entry System

The single entry system has a few features:

- Inadequate recordings of transactions: Cash and selected items are only recorded.

- Lack of full entry bookkeeping: Entries of debit and credit are not always kept.

- Profit difficulty in establishing profit in a direct manner: Profit is not easy to compute as income and expense accounts are not complete.

- Depending upon statement of affairs: A statement of affairs (like a balance sheet) is normally utilized to estimate the capital of the owner and calculate profit.

Irrespective of these constraints, financial statements can be rebuilt by the accountants using a systematic analysis.

Restructuring Financial Statements using incomplete Records

Preparing Accounts from Incomplete Records is typically done using the following steps:

- Decision of opening capital by statement of affairs.

- Arithmetic missing values like credit sales or purchases.

- Prepare the trading account.

- Prepare profit or loss account.

- Make the statement of financial position.

Every step is based on available data to work out credible results.

The Preparation of Trading Account

Gross profit or gross loss of the business can be determined using the trading account. It is primarily concerned with purchasing and selling of commodities.

To find out more about the work of trading accounts when calculating gross profit and the cost of goods sold, you can read the article.

A trading account with a skeleton consists of the following:

Debit side

- Opening inventory

- Purchases

- Direct costs (carriage inward, wages, etc.).

Credit side

- Sales

- Closing inventory

Formula for Gross Profit

Gross Profit = Sales -Cost of Goods Sold.

The cost of Goods Sold is computed as:

Opening Inventory

- Purchases

- Direct Expenses

Closing Inventory

When sales are more than the cost of goods sold, then gross profit is obtained. When the cost is greater than the sales, then the outcome will be the gross loss.

Determining Missing Figures

Incomplete records do not include some figures like credit sales or purchases. They are therefore rebuilt by accountants through control accounts.

Debtors Control Account

This assists in the calculation of credit sales.

Opening Debtors

- Credit Sales

-Cash Received

-Returns Inward

-Bad Debts

= Closing Debtors

Credit sales can be calculated by manipulation of the equation.

Creditors Control Account

This assists in deciding credit purchases.

Opening Creditors

- Credit Purchases

-Cash Paid

-Returns Outward

= Closing Creditors

Under this technique accountants use an estimate figure to occupy missing purchase figures necessary to populate trading account.

Profit or Loss Account Preparation

Upon establishing the gross profit, the next thing is to prepare the profit or loss account. Using the statement, net profit or net loss is determined taking into consideration operating expenses and other incomes.

Common Expenses Included

- Salaries and wages

- Rent

- Utilities

- Insurance

- Advertising

- Depreciation

- Bad debts

Formula for Net Profit

Net Profit = Gross Profit +Other Income- Operating Expenses.

In case cost is greater than revenue, then there will be a net loss.

This statement will give a clue to the efficiency of the business.

Adjustments Required in Financial Statements

In developing financial statements, some adjustments have to be undertaken in order to remain accurate. These adjustments consider the transactions which are related to the accounting period but which are not recorded in a proper manner.

1. The accruals (Outstanding Expenses)

Accrued expenses refer to expenses, which are incurred but not paid. These are unpaid salaries, rent or utilities at the close of the accounting period.

Treatment:

- Add the amount outstanding to the expense account concerned.

- Present it in the statement of financial position as a liability.

The accruals make sure that the expenses are recorded to the relevant accounting period.

2. Prepayments

The pre-paid expenses are when one has made a payment in advance of a future accounting period.

Examples are prepaid rent, insurance or subscriptions.

Treatment:

- The amount paid in advance is to be deduced in the cost account of profit or loss.

- The amount that was prepaid is recorded as a current asset in the statement of financial position.

This makes sure that expenses are adjudicated against the period it is associated with.

3. Depreciation

Depreciation refers to the fact that the value of the fixed assets will decrease over time because of wear and tear, utilization, or even obsolescence.

The typical depreciable assets are:

- Machinery

- Furniture

- Vehicles

- Equipment

Methods of Depreciation

- Straight-line method: The depreciation of the asset is on a fixed basis per annum.

- Reducing balance method: Depreciation is done on a percentage basis of the remaining value of the asset.

Treatment:

- Depreciation is taken as expense in the profit and loss account.

- The worth of the asset is lowered in the financial position statement.

Depreciation is used to make sure the costs of the assets are distributed over their useful lives.

4. Closing Inventory

The inventory is calculated as closing inventory, which is the value of the goods that have not been sold at the end of the accounting period.

It matters as it influences the trading account and also the statement of financial position.

Treatment:

- Include deduct closing inventory in computation of the cost of goods sold in trading account.

- This is to be recorded in the statement of financial position as a current asset.

To calculate the gross profit in the right way, it is necessary to calculate its value by means of accurate inventory valuation.

Preparing the Statement of Financial Position

The financial position of the business at a given date is presented in the statement of financial position (otherwise referred to as the balance sheet).

It consists of three significant elements:

Assets

Assets are the resources of the business which have future economic benefits.

Examples include:

- Cash

- Accounts receivable (debts).

- Inventory

- Equipment

- Vehicles

Assets may be categorized into current and non-current.

Liabilities

Liabilities are liabilities that the business owes in future.

Examples include:

- Creditors (accounts payable)

- Bank loans

- Outstanding expenses

Having liabilities can be defined as a current or a long term liability based on the time needed to pay it off.

Owner’s Capital

Capital is an investment made by the owner of the business. Capital is adjusted in the accounting period in which it applies to:

- Net profit (added)

- Drawings (deducted)

- Added additional investments.

The accounting equation is given below:

Assets = Liabilities + Capital

Calculating Profit on incomplete records

At other times profit is calculated through the capital comparison technique.

The formula is:

- Closing Capital

-Opening Capital

- Drawings

-Alternative Capital Added.

= Net Profit

This is a technique made common in the cases where there are no detailed records.

Importance of Preparing Financial Statements on Incompleteness Records

It is important to prepare financial statements even in cases where business has incomplete records.

Key benefits include:

- Performance appraisal of business: The financial statements indicate the profitability of the business.

- Enhancing financial management: The detection of missing records assists in enhancing the bookkeeping activities.

- Undergoing business decisions: Owners are able to make good decisions regarding expansion, pricing or cost management.

- Adherence to legal and tax demands: Taxes and regulatory compliance Financial statements are commonly required when filing financial statements.

- Securing financing: Financial statements are needed by banks and investors prior to loan or investment.

Challenges of incomplete Records

In spite of the approaches that can be used to conduct reconstruction, incomplete records are problematic in several aspects:

- Accuracy can be compromised by estimation.

- There can be missing of important transactions.

- Lack of checks of double-entry may leave the errors undetected.

- Financial analysis is more complicated.

Due to such constraints, most businesses end up moving to full double-entry accounting systems.

Conclusion

Preparing Accounts from Incomplete Records should be done carefully and their information restored through analysis and reconstruction. Accountants can identify the missing values, calculate reliable reports by utilizing available documents and methods of accounting.

The process will normally start with a reconstruction of the financial data then the trading account is being prepared to establish gross profit. It is then computed as a profit or loss account and that made up of net profit after deducting operating expenses. Lastly, the statement of financial position gives a clear outlook of the financial position of the business.

Temporary adjustments in terms of accruals, prepayments, depreciation, and ending inventory are necessary in making sure that financial statements capture the actual financial performance of the business. Despite the challenges of incomplete records, there are ways to make some meaningful financial reporting and to make an informed decision by using systematic accounting methods.

Get more well researched information about Preparing Accounts from Incomplete Records here.