Introduction

One type of business organization is partnership which is mostly used by small and medium-sized businesses. In contrast to the sole proprietorship, partnership accounting admission and retirement enables two or more persons to pool resources, abilities, and competence in order to meet the common business objectives. Nevertheless, partnerships are dynamic and as such, any changes in structure, e.g. the arrival of a new partner or the retiring of an old one are bound to occur. These developments present some complications in accounting especially in aspects such as profit sharing ratios, capital adjustments, and valuation of goodwill.

These adjustments need to be understood in order to keep partners fair and to apply accounting principles. This paper is a comprehensive guide to partnership accounting including admission, retirement and goodwill valuation in addition to the emphasis of both the theoretical concepts and practical application.

To get a deeper base on this issue, you may read more about partnership accounting and its main principles.

Partnership Accounting Meaning and Features

Partnership accounting is defined as the accounting of transactions, reporting and analysis of transactions of a partnership business. It is the keeping of the correct records on capital contributions, profit distributions, drawings, and changes of the partnership structure.

Key Features:

- Profit-sharing ratio: This is the manner in which the profits and losses are shared.

- Capital accounts: Indicates the capital investment of every partner in the business.

- Mutual agency- Each partner is an agent of the firm.

- Flexibility: partnership agreements are able to be adjusted to certain needs.

The partnership deed is very important, since it provides terms in terms of profit sharing, capital interest, and amount of salary to partners and admission/retirement procedures.

Admission of a Partner

Admission is the entry of a new partner into an existing partnership. This normally occurs when the company needs extra capital or experience.

Reasons for Admission:

- Growth of business operations.

- Need for additional capital

- Introduction of specialized skills.

- Sharing risks with additional partners.

Accounting Adjustments on Admission

Some adjustments have to be made when a new partner joining is made thus making equity among all the partners.

1. New Profit-Sharing Ratio

The new partner will have a portion of the profits in the future. This stock is bought out of the current partners and the ratio of profit sharing is altered.

Example:

Assuming A and B share profits in 3:2 ratio and C is admitted on a 1/5 share, A and B will have to lose some of their shares.

2. Sacrificing Ratio

The sacrificing ratio is the ratio whereby the current partners relinquish their portion of profits to the new one.

Formula:

Sacrificing Ratio = Old Ratio -New Ratio.

It is a significant ratio of goodwill adjustment.

Goodwill and Its Relevance

Goodwill refers to the reputation of the firm, brand loyalty and customer loyalty. It is the power of a company to make more profits than other companies of the same nature.

Features of Goodwill:

- Intangible asset

- Hard to quantify specifically.

- Comes as a result of reputation, location and customer base.

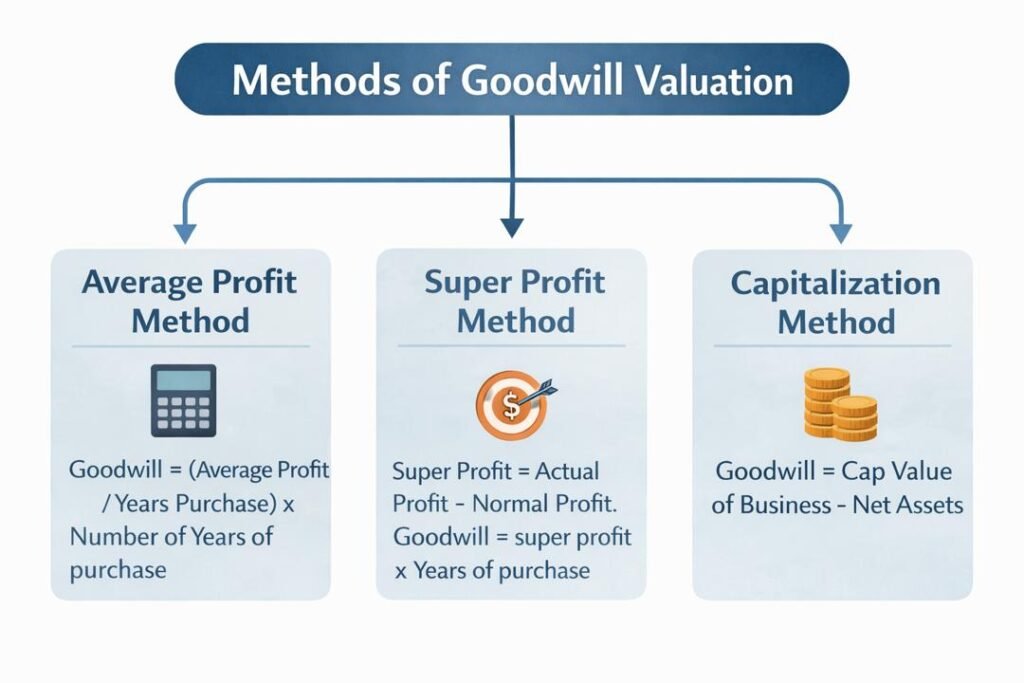

Valuation of Goodwill

In case there is a change in the structure of partnership, goodwill should be considered.

Common Methods:

1. Average Profit Method

Goodwill = (Average Profit/ Years purchase) x Number of Years of purchase.

2. Super Profit Method

Super Profit = Actual Profit -Normal Profit.

Goodwill =super profit x years of purchase.

3. Capitalization Method

Goodwill = Cap Value of Business -Net Assets.

Both methods can be applied in accordance with the type and the size of the business.

Accounting Treatment of Goodwill on Admission

In case of a new partner joining, he or she has to pay the existing partners the share of goodwill.

Methods of Treatment:

1. Premium Method

The cash is introduced by the new partner as goodwill and is shared among the partners that are present in a sacrificing ratio.

Journal Entry:

Cash A/c Dr.

To Goodwill A/c

Goodwill A/c Dr.

To Old Partners capital A/c

2. Revaluation Method

The goodwill is modified by use of partners’ capital accounts without the need to open a goodwill account.

3. Memorandum Revaluation Method

Applied when partners wish to move goodwill on a temporary basis without reflecting them in the balance sheet

Revaluation of Assets and Liabilities

Prior to the admission of a new partner, the assets and liabilities are to be revaluated to show the current market value.

Revaluation Account

- Credit: Increment in the value of the assets.

- Decline in asset value -Debit.

- Profit or loss carried forward to old partners in old proportion.

The Capital Accounts Adjustments

After admission:

- Capital accounts are to be modified according to new ratio.

- New partner can be bringing capital equivalent to his/her share.

- Old partners can also change their capital accordingly.

Retirement of Partner

Retirement is the process that happens when an already existing partner is quitting the partnership based on some reasons like age, health status or individual choice.

The major concerns in the retirement:

- Settlement of dues

- Revaluation of assets

- Adjustment of goodwill

- The change in the profit-sharing ratio.

Gaining Ratio

In case of retirement of a partner, the rest of the partners acquire the share of the retiring partner.

Formula:

Gaining = New Ratio -Old Ratio.

This ratio is employed in the distribution of goodwill among other partners.

Goodwill on Retirement Treatment

The retiring partner is allowed to have his portion of goodwill.

Adjustment Entry:

- Remaining Partners Capital A/c Dr.

- To Capital A/c of Retiring Partner.

The value is allocated in the gaining ratio.

Assets and Liabilities Revaluation on Retirement

As with admission, assets and liabilities are revalued.

- Profit is accrued to all partners (as well as retiring partner)

- Loss Debited to all partners.

Settlement of Account of Retiring Partner

The partner retiring is paid:

- Capital balance

- Share of goodwill

- Share of revaluation profit.

- Accumulated reserves

Payment Methods:

- Lump sum payment

- Installments

- Move to loan account.

Adjustment of the Reserves and Profits not distributed.

Partners have to receive their retirement share of the reserves on the old basis.

Examples:

- General reserve

- Profit and loss account balance.

Practical Illustration: Admission

Example:

The proportion of profits between A and B is 3:2. They are C shareholders 1/5. Goodwill is valued at ₦100,000.

- C’s share of goodwill = ₦20,000

- Distributed in sacrificing ratio of A and B.

Practical Illustration: Retirement

Example:

Profits in A, B and C are in 2:2:1 proportion. C retires. Goodwill is ₦60,000.

- C’s share = ₦12,000

- A and B capital accounts adjusted in gaining ratio.

Difference between Admission and Retirement

Both admission and retirement are associated with changes in the partnership structure, however, they are both different in purpose and accounting. The entry of a new partner to the firm with new capital and in most cases new knowledge is referred to as admission whereas the exit of a partner to the business and the removal of his interest is referred to as retirement.

Goodwill wise, a new partner pays a partner his goodwill during the admission process, and the rest of the partners pay the outgoing partner in retirement. On the same note, admission will deal with the calculation of a sacrificing ratio among the existing partners and retirement will deal with calculation of gaining ratio among the continuing partners.

The capital changes are also not the same: when the new partner joins the company, the capital base is typically augmented whereas when the old partner retires, the capital base is decreased as the money is given back to the exiting partner. These differences notwithstanding, asset and liability revaluation are necessary in both processes in order to be fair and accurate.

Partnership Accounting Common Mistakes

- Poorly calculated sacrificing/gaining ratio.

- Improper goodwill valuation

- Disregarding assets revaluation.

- Mistakes in adjustments of capital.

These errors should be avoided so that there is proper financial reporting.

Importance of Partnership Accounting.

- Maintains equity in partners.

- Helps in easy changeover.

- Maintains transparency

- Supports decision-making

Conclusion

Partnership accounting is a critical part of the management of the partnership business especially in the case of structural changes which include admission and retirement of partners. The changes need to be understood and adjusted well in the profit sharing ratios, capital accounts and goodwill valuation to be fair and accurate. Admission brings new dynamics and existing partners are forced to make some sacrifices in their earnings whereas retirement forces a departing partner to be compensated, usually by means of goodwill and revaluation adjustments.

In both cases, goodwill is an important factor, which shows the reputation and earning potential of the firm. Evaluation and treatment should be done cautiously and in the appropriate means like average profit, super profit or capitalization method. Also, assets and liabilities revaluation will make sure that the partners will share the gains of alteration of the market value equally.

As a matter of fact, partnership accounting needs some theoretical knowledge as well as detailing. Appropriate use of accounting principles is a preventive measure of conflicts between partners as well as enhancing the financial stability of the business. Through these understanding, one would be able to comfortably deal with intricate partnering transactions and lead to the eventual success of the company.

Get more well researched information about Partnership Accounting Admission and Retirement here.