Introduction

Accounting has been termed as a business language. The cornerstone of this language is a great and beautiful system called the Double-Entry Principle and Accounting Equation. The principle is the structural foundation of the contemporary accounting and guarantees that all the financial transactions registered by the business are balanced and internally consistent. In its absence, financial reporting would be hectic, unreliable and prone to errors.

This article discusses the concept of the double-entry bookkeeping and its basis on accounting equation (Assets = Liabilities + Equity). It describes the rules of debiting and crediting, balancing of transactions and conceptual integrity of the accounting system. Finally, it shows how the principle of financial records accuracy ensures the maintenance of the mathematical integrity of financial data and the consistency of financial information.

Understanding the Double-Entry Bookkeeping Principle

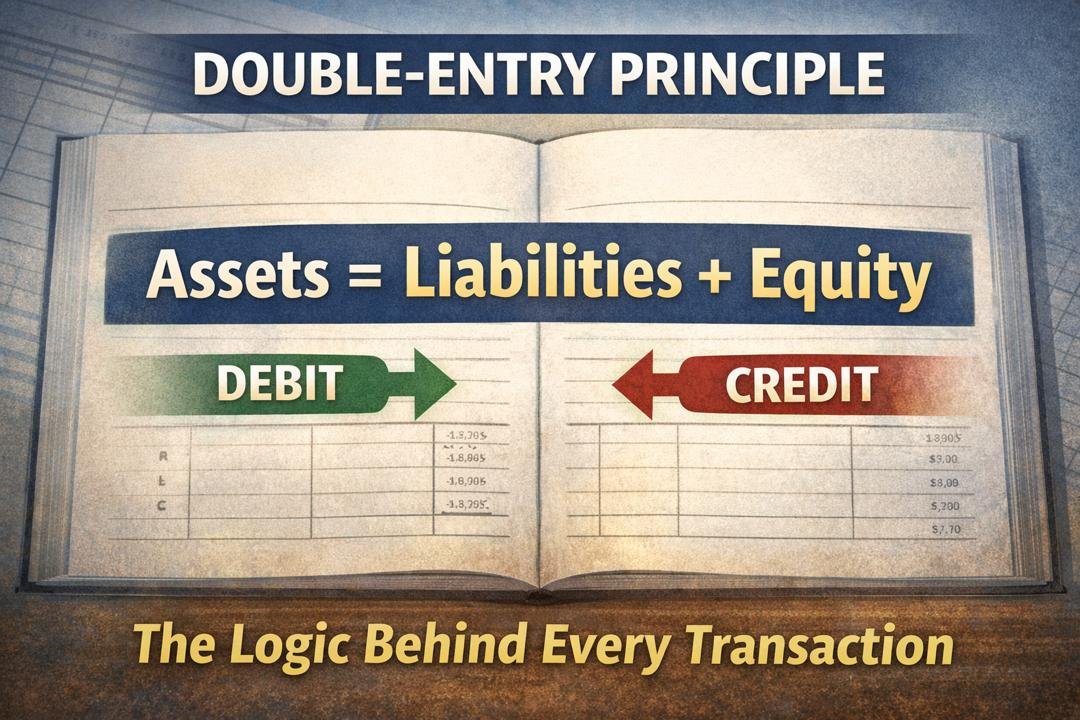

There is the Double-Entry Principle and Accounting Equation according to which all financial operations have at least two accounts to be impacted and that the sum of debits should always be equal to the sum of credits. That is, the impact of every transaction is two-fold.

This rule is not a fortuitous one. It is based on the accounting equation which is:

Assets = Liabilities + Equity

This equation must be maintained in every transaction that has been recorded. When the equation is not balanced when recording a transaction, then an error has been made.

The rationale of double-entry is quite straightforward and at the same time far-reaching, the resources of a business (assets) can be financed either by making loans (liabilities) or by the owner’s investment and accrued profits (equity). Thus, any alteration in resources has to be matched with a corresponding alteration in claim over the resources.

The Accounting Equation: Double-entry Basics.

Accounting equation represents the financial position of any business at any given time:

Assets = Liabilities + Equity

Let us define each component:

- Assets: Economical resources that have been owned or possessed by a business (cash, inventory, equipment, accounts receivable).

- Liabilities: Creditor claims (loans, accounts payable).

- Equity: The undistributed interest of the owners in the business (capital contributions and retained earnings).

In the equation, the assets may be financed by either creditors or the owners. There should always be a balance in this relationship.

For example:

Assuming a business has N1,000,000 assets and N400,000 liabilities, then equity has to be N600,000.

The equality is not voluntary–it is institutional. The principle of a double-entry bookkeeping is present with the aim to ensure that this structural balance must remain at all times.

The implications of Transactions on the Accounting Equation

All the transactions should maintain a balance in the accounting equation. The equation can be influenced by transactions in a number of ways:

- Before and after a rise in one asset, a reduction in another asset.

- Increase one liability and reduce another liability.

- Increase asset and increase liability.

- Grow assets and increase equity.

- Reduce the assets and reduce the liabilities.

- Reduce the assets and reduce equity.

With all these combinations, there is equality.

Example 1: Owner Invests Cash

N500,000 cash is invested in the business by its owner.

- Cash (Asset) increases by N500,000.

- Owner Capital (Equity) is brought up by N500,000.

The formula is equal since there is a proportional increase on each side.

Example 2: Purchase Equipment on Credit.

The equipment costing N200,000 is bought by the business on credit.

- Expenses (Asset) goes up by N200,000.

- Accounts Payable (Liability) goes up by N200,000.

Again, balance is preserved.

Example 3: Payment of Rent

The company is paying N50,000 as rental.

- Cash (Asset) decreases by N50,000.

- Equity is decreased (in terms of retained earnings) by N50,000 Rent Expense.

The reduction of assets results in an equal reduction of equity.

In all the cases, equality is observed. This is the reasoning that lies behind the concept of the double-entry bookkeeping.

Debit and Credit Regulations Defined

Accountants use debits and credits in order to operationalize the double-entry system. These do not mean an increase or decrease in every instance. Rather they are directional entries in accounts.

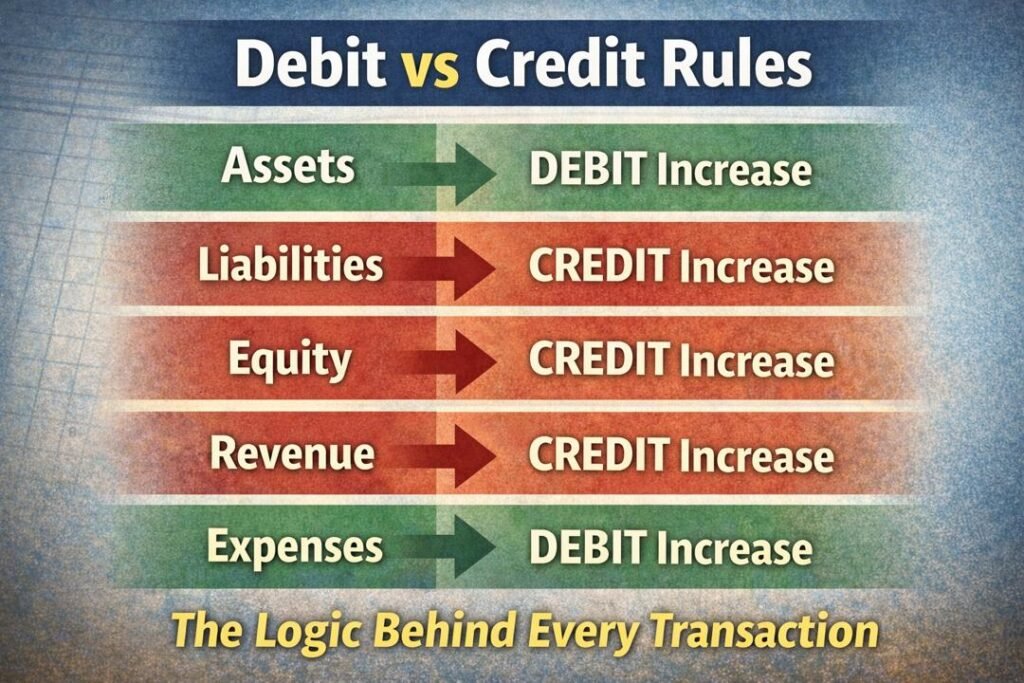

The normal balance side of the accounts is as follows:

| Account Type | Increases With | Decreases With |

| Assets | Debit | Credit |

| Liabilities | Credit | Debit |

| Equity | Credit | Debit |

| Revenue | Credit | Debit |

| Expenses | Debit | Credit |

The key rule is:

Total Debits = Total Credits

This rule enforces balance.

Why Assets grow with Debits

The accounting equation has the assets on the left. Left-side entries are represented in debits. Consequently, the increment of an asset involves debiting.

Justification of the increase of Liabilities and Equity with Credits

On the right hand side of the accounting equation, they are liabilities and equity. Credits are right side entries. Thus, raising the liabilities or equity will need a credit.

This ledger format structure is a reflection of the accounting equation.

The Ledger and T-Accounts

As it happens, the records of transactions are made in journals and later posted to ledger accounts. Every ledger account may be depicted in the form of a T-account:

Account Name

Debit | Credit

For example:

In case of receipt of cash by a customer:

- Debit Cash

- Credit Revenue

The credit is recorded on the left hand side of the Cash account. The credit is recorded at the right hand side of the Revenue account.

Debits in all the accounts should be equal to credits at the end of the accounting period. Otherwise, the discrepancy will be seen in the trial balance.

Transaction Balancing in a Practice

We shall look at a full cycle transaction.

Scenario: Sale of Goods for Cash

A company is selling commodities at N100,000 cash.

Step 1: Determine Information at risk.

- Cash (Asset) increases

- Sales Revenue (Equity through retained earnings) is augmented.

Step 2: Adopt the rule of debit and credit.

- Debit Cash N100,000

- Credit Sales Revenue N100,000

Step 3: Verify balance

- Total debits = N100,000

- Total credits = N100,000

Balanced

Scenario: Paying a Supplier

The firm makes N30,000 in paying an outstanding payable.

Accounts affected:

- Cash (Asset) decreases

- Accounts Payable (Liability) reduces.

Journal entry:

- Debit Accounts Payable N30,000

- Credit Cash N30,000

Again, debits equal credits.

This balancing process eliminates the effects of one-sided recording. There can never be a transaction in a vacuum.

The Conceptual Integrity of the System

The brilliance of the concept of the double-entry bookkeeping is in its conceptual soundness. It ensures:

- Mathematical Accuracy: The equality condition has to be fulfilled in every transaction.

- Error Detection: In case the debits are not equal to the credits, then the errors can be instantly detected.

- Complete Recording: Every transaction has its cause as well as its impact.

- Financial Transparency: The system has a clear way of showing the source of the resources and their utilization.

The accounting equation is a self-balancing mechanism. It is internally consistent in nature.

Prevention of Mathematical Discrepancies

The entry-dual system avoids an array of accounting issues:

One-Sided Entries

This is because a transaction cannot be recorded with a single account. The necessity to have two entries inhibits incomplete data.

Arithmetic Errors

In the event of differences in totals, accountants get to know instantly that there is an error. The balance sheet acts as a control point.

Misclassification

The systematic application of the debit and credit rules makes it possible to spot the erroneous treatment of accounts.

Fraud Reduction

Although the system is not complete proof against it, it makes it more challenging to hide, as each manipulation should be entered.

Relationship between Revenue, Expenses and Equity

Revenue augments equity, whereas the expenses lessen equity.

Expansion of the accounting equation:

Assets = Liabilities + Owner Capital + Revenue -Expenses -Drawings

This is an expanded equation of the influence of operational activities on equity. Since the effect of revenue is positive, and the effect of expenses is negative, the effect is similar to the right side of the equation.

For example:

- When the revenue rises higher than expenses, the equity rises.

- When there is a surplus of expenses compared to revenue, there will be a reduction in equity.

In this manner, the balance sheet is eventually linked to the income statement via retained earnings.

The Trial Balance: An Experiment in Equality.

Businesses prepare a trial balance at the conclusion of an accounting period. This account is a list of all accounts and the debit or credit balance.

If:

Total Debits = Total Credits

The books are mathematically equalized.

It is however worth noting that not all the errors (including the wrong amount included in the debit and credit) would be detected using the trial balance. However, it minimizes the occurrence of mathematical discrepancies greatly.

Historical Importance and Modern Relevance

The principle of the double-entry bookkeeping has been able to survive over centuries due to its logical soundness. The fact that it survived, proves that the accounting equation has a universally applicable structure.

The modern accounting software automatically records the debit and credit postings, although, the principle is the same. All the digital transactions do not violate the principle that total debits should be equal to total credits.

Technology has increased the speed of processing, which has not substituted the structural logic of double-entry bookkeeping.

Why the System Works

It is a working system, since it is based on logical symmetry:

- Every resource has a source.

- There is a claim relating to every increase.

- All reductions are corresponding to a reduction.

Internal coherence is the result of this symmetry. In the case of business acquiring assets, they have to be funded. In case the liabilities are reduced then the assets should be reduced or equity should be increased.

It does not have a mathematical ambiguity.

Conclusion

The Double-Entry Principle and Accounting Equation is much more than a system of mechanical recording. It is a rationally arranged system, which is based on the accounting equation (Assets = Liabilities + Equity). It provides mathematical equality by balancing of transactions and posting of transactions through use of debit and credit rules.

Internal consistency is ensured by its conceptual integrity. Balancing requirement does not permit one-sided entries. It has structural symmetry, which encourages financial transparency. and of its checks eliminate the chances of discrepancies.

Finally, the double-entry system dramatically changes accounting into a record-keeping system and makes it a disciplined and logically sound system. Each of the simplest purchases is a part of an interdependent system which operates according to equality. The fact that equality is not optional–it is the basis on which financial reporting can be relied upon to stand so well.

By doing this, the principle of a double-entry bookkeeping has remained the rationale behind all transactions and the protection of financial accuracy in the contemporary business practice.

Get more well researched information about the Double-Entry Principle and the Accounting Equation here.