Introduction

When preparing the financial statements, it is necessary to be accurate in registering and categorizing the transactions. Yet, even with proper bookkeeping, errors may still be made in either recording or posting, or balancing of accounts. All these errors are normally termed as accounting errors. When correction of errors in accounting does not take place, it may interfere with financial information, mislead decision-makers, and decrease the effectiveness of financial reports.

Knowledge of the causes of errors and ways of correcting them is consequently a vital aspect of accounting practice. Accountants involve systematic process of identifying and correcting anomalies in the process of upholding the integrity of the double-entry system. In this process, two tools are important and include suspense accounts and control accounts. Such records are used to determine differences in the books and give a provisional or summarized record, which is used to facilitate the detection and correction of errors in accounting

This article describes the character and types of accounting errors, how they are corrected and how suspending and control accounts play a role in the operations of maintaining proper ledger records.

Understanding Accounting Errors

Accounting errors are those that are inadvertent and are in the recording, classification, calculation, or posting of financial transactions. Such mistakes can be attributed to human factor, lack of understanding of accounting principles or mechanical errors when entering data.

Manual and computerized accounting systems are prone to errors. The risks of arithmetic errors are minimized by modern accounting programs, but it is still possible that there can be the mistake of wrong entries or depending on the wrong group.

Detection of these mistakes is a significant process toward ensuring reliability of financial records. The trial balance is considered to be the initial checkpoint in as far as it confirms the sum of debits to that of credits on the ledger. There are, however, a number of errors that cannot be identified by the trial balance. There are some mistakes in which it applies to both sides of the ledger and hence this is concealed until reviews or reconciliations are conducted in details.

Causes of Accounting Errors

The causes of accounting errors are due to:

- Human Mistakes: Accountants or clerical personnel can key in the wrong figures or record entries to accounts which are not correct.

- Misinterpretation of Transactions: A transaction can be misunderstood and recorded incorrectly.

- Lack of Accounting Knowledge: The misclassification of the transactions can be caused by poor interpretation of accounting principles.

- Fatigue or Carelessness: Financial data can be monotonous so that there might be neglect in maintaining or oversight.

- Technical Issues: Even computerized ones could have a mistake because of the software glitches or wrong system configuration.

The identification of these causes assists organizations to introduce better internal controls to minimize accounting errors.

Classification of Accounting Errors

The different categories of accounting errors are based on the way they are created or how they affect the accounting records.

- Errors of Omission: These happen when a transaction is omitted fully or incompletely in books of accounts.

Example:

A sale of credit in the amount of $500 is not entered on the sales journal.

Types of omission include:

- Complete omission – the transaction is not reflected anywhere in the books.

- Partial omission – this is used when the transaction is made in the journal but not in the ledger.

- Errors of Commission

Errors of commission are a situation where the transactions are entered with the wrong figures or with the wrong accounts of the same category.

Example:

A transaction that is supposed to go to Customer A is charged against the account of Customer B.

Even though the balance of the trial may be still congruent, there will be wrong balances of individual accounts.

- Errors of Principle

These are in case accounting principles are breached.

Example:

Office equipment is not purchased as a capital asset but as an expense.

These mistakes influence the financial statement accuracy in spite of the fact that trial balance balances.

- Errors of Original Entry

This mistake is done when the incorrect amount is entered in the journal and the erroneous amount in the ledger also.

Example:

A purchase of $950 is recorded as $590.

Since the same wrong figure appears in the debit and credit side then still, the trial balance will balance.

- Compensating Errors

There are cases in which errors are compensated where two errors and more can offset each other.

Example:

A cost that is underreported by a figure of less than 200 and an over reported cost of more than 200.

Even when there are mistakes, the trial balance will be seen to be correct.

Identification of Accounting Errors

The accounting errors can be detected by reading financial records and pointing out inconsistencies. Some common methods include:

- Trial Balance Review: In case the balancing of trials is irrelevant, it means there are errors.

- Rechecking Ledger Entries: Perpetual balances are used to compare ledger balances with original journal entries to identify posting mistakes.

- Reconciliation Procedures: Bank reconciliations and subsidiary ledger reconciliations are useful in detecting discrepancies.

- Verification of Calculations: When the calculations are made manually, the annexed tables must be verified and confirmed by the managers. Arithmetic errors can be identified by checking additions, balances and totals.

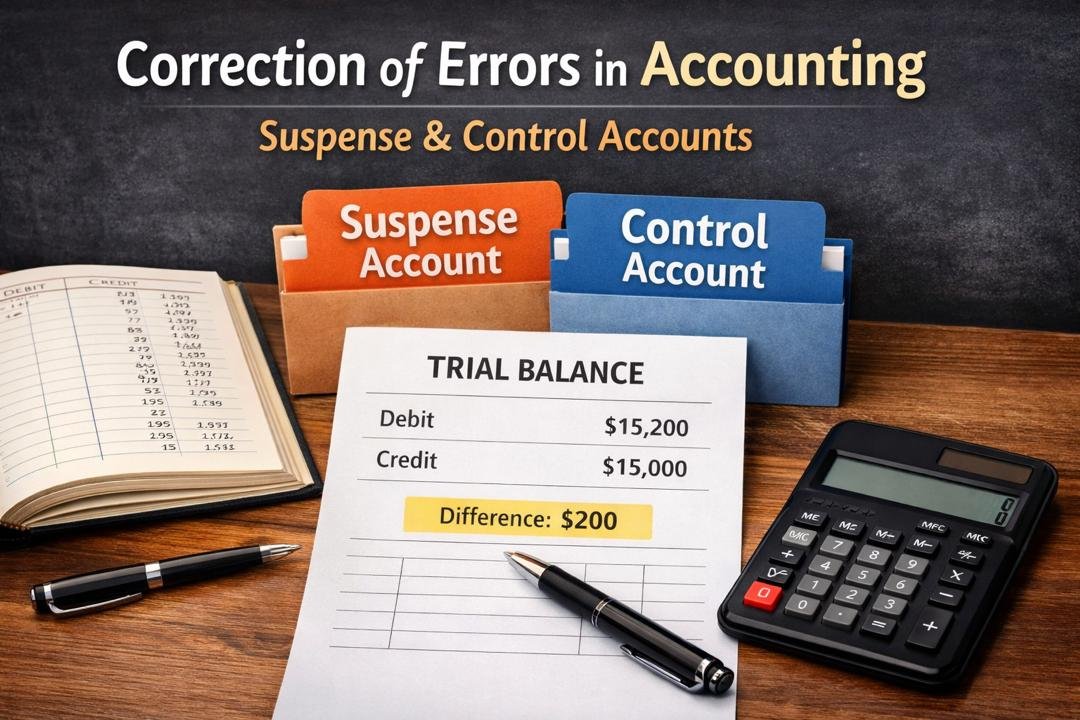

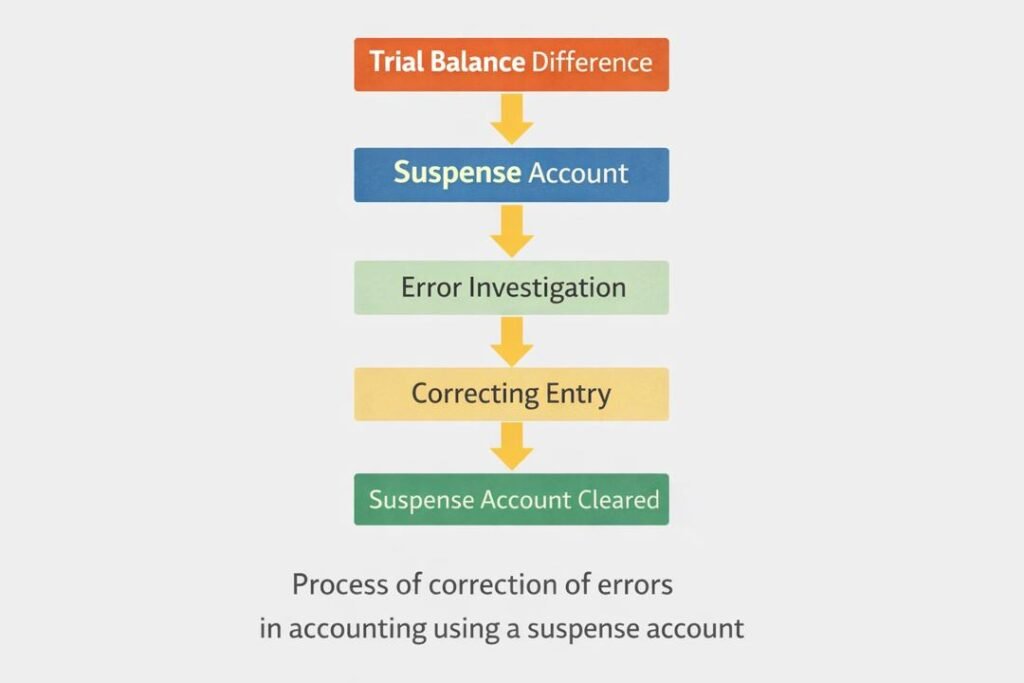

Suspense Accounts and their Roles

Suspense account is an account that is temporary in nature and is applied when the balance in the trial is not equal or when the proper classification of a transaction is not known.

It enables accountants to record temporarily the difference as they investigate.

Purpose of a Suspense Account

- To provisionally receive anomalies in the books.

- So that preparation of financial statements can be made possible in the event of errors being investigated.

- To aid in verifiability of errors.

In case the error was found, corrective entries are prepared and a suspension account is cleared.

Example of a Suspense Account

Suppose that the trial balance indicates:

Total Debits: $15,200

Total Credits: $15,000

There is a difference of $200.

In order to bring the balance to an extent of agreement, the accountant will temporarily record:

Debit Suspense Account $200

After the mistake has been corrected, the suspense will be removed to the account.

Rectification of Errors

When accounting errors are found, their correction is done by making correct adjusting entries to regain accuracy of the ledger.

When the Trial Balance does not balance:

Mistakes that occur on one side of the ledger lead to trial balance errors.

Example:

The payment of $300 by a customer was recorded only in the debit account of cash but not on the credit account of the customer.

Correction entry:

Customer Account: Credit $300

When the Trial Balance Balances:

Certain mistakes are not observed in the trial balance.

Example:

Furniture purchase in office is considered as office expense.

Correction entry:

Debit Furniture Account

Credit Office Expense Account.

Control Accounts Explained

A control account is a summary account in the general ledger which is used to consolidate balances in the subsidiary ledgers.

Control accounts assist the accountants to ensure that the detailed records are accurate.

Types of Control Accounts

- Sales Ledger Control Account: summarizes the accounts receivable.

- Purchases Ledger Control Account: sums up accounts payable.

These records enable the accountants to compare totals between the general ledger and the subsidiary ledger.

Advantages of Control Accounts

Control accounts have a number of advantages:

- Error Detection: The discrepancy between control account and subsidiary ledger shows the potential accounting errors.

- Simplified Reporting: Instead, they generalize thousands of pieces of information into totals.

- Division of Work: Subsidiary ledgers can be kept by different members of staff but the control account is kept independently.

- Fraud Prevention: Fraudulent changes are discouraged through regular reconciliation.

Sample of Sales Ledger Control Account

Assume the following data:

Opening receivables balance: $5,000

Credit sales: $3,000

Cash received: $2,000

Calculation of control account:

Opening Balance = $5,000

- Credit Sales = $3,000

- Cash Received = $2,000

- Closing Balance = $6,000

This balance at the end must be equal to the sum of all the individual customer balances.

Otherwise, an investigation is needed to identify accounting mistakes.

Relationship between the Suspense Accounts and the Control Accounts

Although the two accounts are useful in preserving the accuracy, they are used in different purposes.

| Feature | Suspense Account | Control Account |

| Purpose | Differences for holding account (temporarily). | Balance of subsidiary ledger. |

| Duration | Temporary till mistakes are rectified. | Part of accounting system that is permanent. |

| Main Role | Helps find and correct accounting mistakes. | Helps check validity of subsidiary records. |

These accounts, combined, increase the credibility of financial reporting.

Structured Sample of Error Correction

Suppose the following case:

Purchases made of goods amounting to 400 dollars were recorded as 40 dollars to purchases account.

Step 1: Identify the Error

Correct amount: $400

Recorded amount: $40

Difference: $360 understated.

Step 2: Correct the Entry

Debit Purchases Account $360

This restructuring makes sure that the ledger is captured as having the right type of transaction.

Preventing Accounting Errors

Correction of errors in accounting procedures are critical but prevention is all the more. The following practices are ways through which organizations can reduce accounting errors:

- Strong Internal Controls: Distribution of functions and setting up of approval processes minimize errors.

- Regular Reconciliation: Repeated reconciliation of the ledgers, bank statements and control accounts assists in identifying discrepancies at an early stage.

- Staff Training: Accounting officers that are well trained will lessen their errors in classification.

- Automated Systems: The accounting software used in the modern days minimizes arithmetic and posting errors.

- Periodic Audits: External and internal audits are used to determine the flaws of the accounting system.

Conclusion

Financial reporting is dependent on the quality of financial records. The errors are however caused by human error, lack of understanding of transactions, or mechanical problems. The apprehension of what accounting errors are and the type of error they represent assists the accountant to identify inconsistencies and implement the relevant correction of errors in accounting.

Suspense use enables the accountants to temporarily balance the differences in the trial balance whilst inquiry is sought. Control accounts on the other hand contain summarized records that are used to confirm the accuracy of subsidiary ledger.

A combination of these mechanisms enhances the integrity of the double-entry system, and the financial information is reliable, consistent, and useful to make decisions. Through rigorous error detection devices and effective internal controls, the organizations are able to keep proper accounting records and ensure that their financial statements are credible.

Get more well researched information about the Correction of errors in accounting here.