Introduction

Accounting is a discipline which is seen as being pragmatic in task since it involves documentation of financial transactions and financial statements. But, under these daily operations, there is an orderly body of knowledge, which directs the practice and understanding of accounting. This is referred to as accounting theory. It gives the background on which accounting standards are created, financial reports are drawn and economic decisions are drawn.

The accounting framework is important not only to students and professionals but also to stakeholders, who use financial information. It describes the reasons of accounting practices, not how the practice is done. This paper provides general information about accounting principles, its definition, scope and importance as well as stressing its importance in the financial reporting, standard-setting, and interpretation of financial data.

You can read more about accounting theory and its changing role in the contemporary financial system to discover more about frameworks and its applications.

Definition of Accounting Theory

Accounting theory is a body of rules, ideas, assumptions and procedures that form the basis of the preparation and reporting of financial statements. It is a rational system that controls the accounting practices and that aids in explaining and predicting the accounting conduct.

Accounting theory is defined variably by different scholars and professional bodies, but it is possible to identify common elements:

- Conceptual Foundation: It offers the foundations on which accounting practices are based.

- Explanatory Role: It is the reason behind the use of some accounting methods.

- Predictive Function: It assists in predicting the impact of accounting information on decision making.

- Normative and Positive Aspects: It incorporates both; prescriptive (what should be done) and descriptive (what is actually done) analysis.

Essentially, the accounting theory helps to bridge the divide between abstract and applied accounting concepts.

Nature and Characteristics of Accounting Theory

There are a number of different attributes that accounting theory has in common with bookkeeping or procedural accounting:

- Systematic and Logical: It is organized in a rational way, and financial reporting and interpretation is consistent.

- Dynamic and Evolving: The accounting concepts has been changing according to the changes in the business environment, the economic conditions and the regulatory conditions.

- Positive Dimensions and Normative: Normative theory is concerned with the accounting practices that should be. The positive theory predicts and explains the actual accounting practices.

- Conceptual Framework-Based: It is also closely associated with the conceptual frameworks that are created by standard-setting organizations which give directions in financial reporting.

- Interdisciplinary Nature: The accounting theory is based on economics, finance, law, and behavioral sciences, which explain financial phenomena.

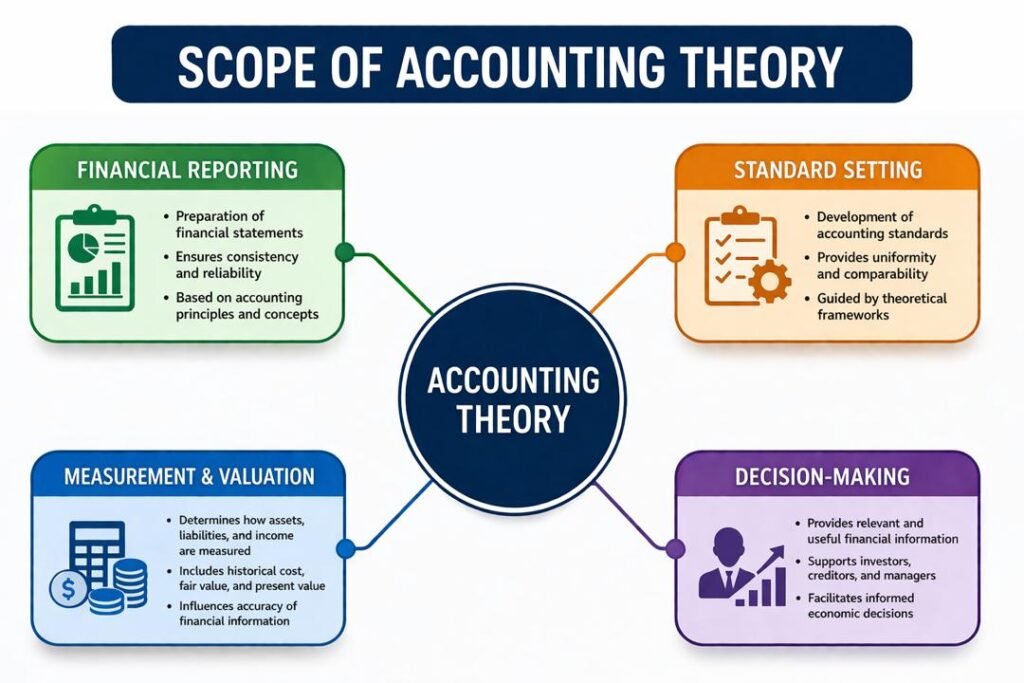

Scope of Accounting Theory

Accounting theory is very extensive and covers many elements of accounting practice and research. It is not only about the financial reporting, but also about concepts, regulation and analysis.

1. Financial Reporting

Financial statements prepared using accounting framework includes:

- Balance sheet (statement of financial position).

- Income statement

- Cash flow statement

It oversees that such reports are prepared based on similar principles and standards.

2. Standard-Setting

Among the most significant fields that fall under the accounting theory is its contribution to the accounting standards. Standard-setting organizations make use of theoretical frameworks to:

- Establish accounting rules

- Be consistent with organizations.

- Respond to arising financial reporting situations.

3. Measurement and Valuation

The principles of accounting is concerned with the measurement of assets, liabilities, revenues and expenses. This includes:

- Historical cost accounting

- Fair value measurement

- Present value techniques

Such bases of measurement affect the reporting and interpretation of financial information.

4. Recognition and Disclosure

It determines:

- When the financial aspects need to be identified in financial statements.

- What is to be revealed to users?

This makes financial statements sufficiently relevant and complete.

5. Decision-Making Framework

The accounting theory is used to aid in decision-making by providing appropriate financial information to:

- Investors

- Creditors

- Managers

- Regulators

6. Behavioral Aspects

It also takes into account the responses of individuals and organizations to accounting information, such as:

- Managerial incentives

- Earnings management

- Investor reactions

7. Ethical Considerations

Ethical accounting practices is an academic field that teaches professionalism and provides integrity in financial reporting.

Objectives of Accounting Theory

The theory of accounting is developed to accomplish a number of goals:

- Offer a Conceptual Framework: It provides a systematic basis of accounting standards and practices development

- Enhance Consistency: It provides consistency in accounting in organizations and industries.

- Enhance the Quality of Financial Reporting: It enhances precision, consistency and topicality of financial statements

- Facilitate Comparability: It allows users to compare money between various organizations and durations.

- Support Decision-Making: It is a valuable source of economic information.

Importance of Accounting Theory

The accounting theory is extremely important in the operations of the contemporary financial systems. Several of its contributions can be understood as important:

1. Foundation for Financial Reporting

Financial reporting is supported by the accounting theory. It gives the principles and guidelines that would make financial statements:

- Accurate

- Consistent

- Meaningful

Financial reporting would not be structured and coherent in the absence of accounting theory.

2. Guidance to Standard-Setting

Accounting theory is an important factor that accounting standard-setting bodies consider in the development of accounting standards. These standards are necessary to:

- Having consistency in reporting.

- The emerging financial difficulties.

- Adhering to regulatory requirements.

3. Enhancing Transparency

Effective financial reporting is based on transparency. The accounting theory should encourage openness through:

- Promotion of disclosure of relevant information.

- Less information asymmetry between management and the stakeholders.

4. Ensuring Comparability

The accounting theory makes sure that the financial statements are made in the similar ways so that the user can:

- Compare company performance on financial basis.

- Evaluate trends over time

5. Improving Reliability

Reliability is the referral to accuracy and reliability of financial information. The accounting theory will increase the reliability by:

- Creating measurable and recognition standards.

- Less subjectivity in reporting.

6. Making Economic Choices

Financial information is important as it guides investors, creditors and other interested parties to make decisions. This information is ensured by accounting theory because it:

- Relevant

- Timely

- Useful

7. Discussing Complicated Financial Problems

The contemporary business settings entail elaborate dealings like:

- Derivatives

- Leasing arrangements

- Revenue recognition

Tools to deal with these complexities can be found in accounting theory.

Role of Accounting Theory in Financial Reporting

The theory of accounting is key in influencing the practice of reporting financial matters. It has the model that makes financial reports attractive to their users.

1. Development of Conceptual Framework

Accounting framework forms the basis of conceptual frameworks that are used as a guide:

- It involves preparing financial statements.

- Diffusion of accounting concerns.

- Developing new standards

2. Identification and Evaluation

According to accounting principles, the following is determined:

- What are to be expressed in financial statements?

- The way these things are to be measured.

As an example, the decisions regarding the use of historical cost and fair value are based on theoretical concepts.

3. Disclosure Requirements

It provides principles that determine what information is to be disclosed so that financial statements are:

- Complete

- Transparent

- Informative

4. Consistency and Uniformity

The framework of accounting makes sure that similar transactions are handled in a uniform manner in various organizations.

Role in Standard-Setting

The accounting theory plays a critical role in accounting standards development. The theoretical frameworks assist the standard-setting bodies in:

- Contemporary accounting principles.

- Develop new standards

- Reform the current laws.

This is to make sure that standards are:

- Logical

- Consistent

- Changeable in circumstances.

In the absence of the accounting principles, there would be no consistency in standard-setting.

Role in Interpretation of Financial Data

The accounting theory also assists its users to understand financial information. It gives a model under which to comprehend:

- Financial ratios

- Performance indicators

- Trends and patterns

1. Analytical Framework

It allows users to systematize the analysis of financial data and make substantial conclusions.

2. Understanding Assumptions

The assumptions in accounting theory are brought to the fore like the following:

- Going concern assumption

- Accrual basis of accounting

3. Reducing Misinterpretation

Accounting framework also reduces the chances of misinterpreting financial information because it gives the right guidelines.

Limitations of Accounting Theory

Although it is an important aspect, accounting theory has some limitations:

- Lack of Universality: Various nations and institutions can use diverse accounting systems.

- Subjectivity: Judgment in some accounting principles results in the difference in application.

- Complexity: Non experts may find accounting theory rather complex and understandable.

- Changing Environment: This is because accounting theory needs to be updated regularly due to the rapid changes in business practices.

Evolution of Accounting Theory

The accounting framework has grown in many ways over time:

1. Traditional Approach

Specialized in bookkeeping and historical cost accounting

2. Modern Approach

Includes fair value assessment and prospective knowledge

3. Contemporary Trends

Include:

- Sustainability reporting

- Integrated reporting

- Digital accounting systems

This development is an indication of the shifting stakeholder requirements and technology.

Conclusion

The accounting theory is the foundation of the accounting profession that offers the guidelines and principles according to which one can understand financial reporting, setting standards and data interpretation. It also assures that financial data is clear, comparable, and credible and hence aids in making decisions.

It is applicable to different issues of accounting, such as measurement, recognition, disclosure, and behavioral issues. The accounting theory, despite its shortcomings, is crucial in the process of responsiveness to the intricacies of the current financial systems and the need to respond to the emerging issues.

The accounting framework is a very important tool in a world where financial information forms a critical part of economic decision-making. It is also important to know what it is, what it covers and the significance of it so it is important to any person engaged in accounting or financial analysis.

Get more well researched information about Accounting Theory here.