Introduction

Financial reporting is essential in assisting the organizations to communicate their financial performance and status of the organization to the various stakeholders that include investors, creditors, managers and regulators. Financial statements would however not be useful and accurate without a code of principles that operate the manner in which financial data is prepared and presented. Such are the accounting concepts and conventions. They base the financial reporting because they make the financial statements prepared in a consistent manner, transparently and in a manner that users can make good economic decisions.

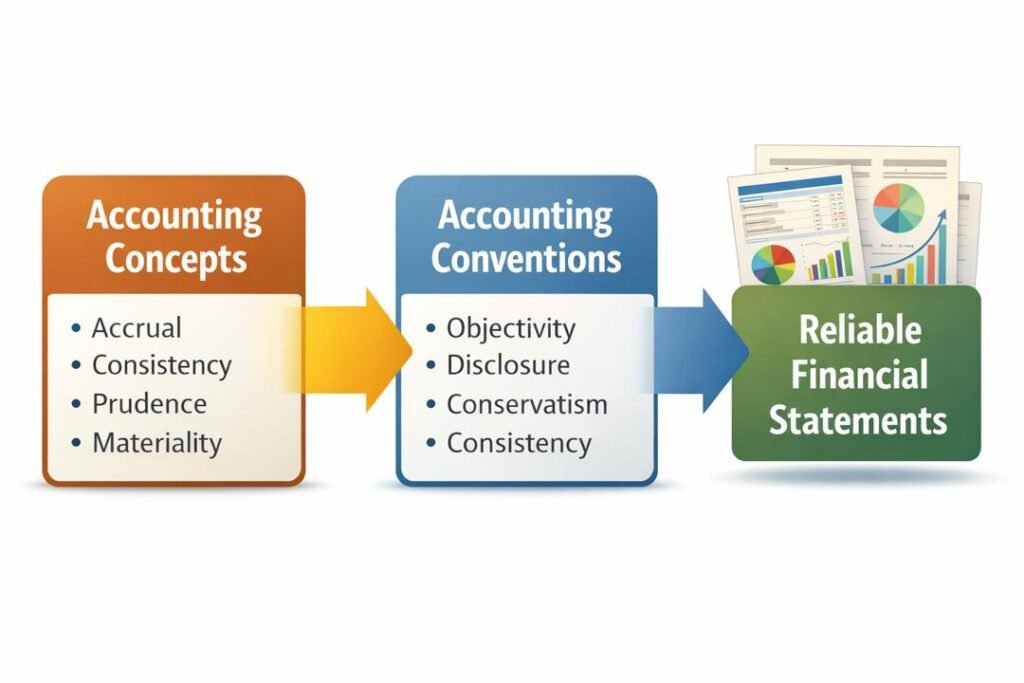

The concepts of accounting represent the underlying assumptions that lie behind the preparation of financial statements and the accounting conventions describe the generally accepted practices that accountants follow with application of the accounting concepts into real-life situations. They are together used to generate uniformity, reliability and comparability between financial reports prepared by different organizations and on different periods.

Some of the most significant principles in the financial reporting include accrual, consistency, going concern, prudence and materiality. Such underlying concepts aid in making sure that financial statements give a fair and fair picture of the financial position of an organization and its performance. The knowledge of these principles is crucial to any person working in the accounting, finance, or business decision-making process.

To gain a more insight into these principles, it is sufficient to discuss the underlying accounting concepts and conventions that can be regarded as the blocks of financial reporting systems worldwide.

Understanding Accounting Fundamentals and conventions

Accounting concepts refer to the underlying assumptions and fundamental principles, which are used in the preparation and presentation of financial statements. They offer a guideline; through which financial information is captured in a systematic and regular way.

Accounting conventions, in their turn, are the common usages that the accountants adhere to in the course of implementing the accounting principles. These conventions are useful in addressing the practical problems that might be involved in financial reporting and making the information comprehensible and helpful to the stakeholders.

Accounting concepts and conventions, in combination, facilitate the primary goals of financial reporting that are:

- Information providing useful information to make economic decisions.

- Promoting accountability and transparency.

- Encouraging financial reporting uniformity.

- Admission of inter-organizational and inter-accounting period comparison.

Devoid of these principles, the financial statements may be inconsistent, misleading and hard to interpret.

1. The Accrual Concept

The accrual concept is one of the most basic concepts of accounting. According to this concept, the revenues and expenses must be recognized in the accounting period in which they arise and not in the period where they are actually received or paid.

The accrual basis of accounting requires that financial transactions should be recorded when they are earned or incurred. This makes financial statements to be a mirror of the actual economic operations of a business at a certain period of time.

To illustrate this, when an organization offers service to a customer in December, but is paid in January then the revenue would be registered in December since that is the month of service. The same applies with regards to expenses that are incurred but later paid.

Accrual concept enhances the precision of the financial reporting because it allows matching the revenues to the expenses incurred to produce the revenue. The strategy is more effective in giving a better understanding of the profitability and performance of a given company.

2. The Consistency Concept

The consistency concept mandates that a business adopt the same accounting procedure and methods in two accounting periods. Consistency also means that financial statements may be compared across time and thus the stakeholders may analyze the performance and financial position trends.

An example is that when a company selects certain depreciation method of its assets, it ought to maintain the same methodology the next time it prepares its accounts. A shift in accounting methods would often lead to a situation where, the financial statement users will not be able to make a comparison of financial results over time.

Consistency however does not imply that accounting methodology cannot change. In case another accounting system offers more consistent or pertinent information, then a firm can switch to it. When this happens, the change should be reported transparently in the financial statements in order to make the users know the impact of the change on the financial performance.

Stability fosters trust and openness of financial reporting and builds trust among stakeholders about financial statements.

3. The Going Concern Concept

The concept of going concern presupposes that a business will exist at least up to the predictable future and is not aimed at the liquidation of its assets and considerable shrinkage of its operations.

This is the assumption around which the preparation of financial statements is based as assorted accounting practices depend on this assumption. In a case illustration, assets are normally valued at their historical prices as opposed to their liquidation prices in that the business is likely to still use the assets in its operations.

Financial statements would be different had a company not been viewed as a going concern. Other assets may be required to be valued at their market value in the immediate sale and their liabilities may also be different.

The accountants and auditors are vigilant in appraising the appropriateness of the going concern assumption. In case of severe uncertainty in the continuity of a business, the same should be reported in the financial statements.

The going concern concept thus assists in providing that there is a long term operational view of most business reflected in the financial reporting.

4. The Prudence (Conservatism) Concept

Prudence is also referred to as the principle of conservatism and this is to be cautious when making judgments during accounting. This concept holds that accountants are not supposed to over-state the assets and income, but rather they should not under-state liabilities and expenses.

This practically implies that possible losses must be registered immediately they are projected, but gains can only be registered when they are realized or at the point of being certain.

To illustrate, in the case when a business anticipates that some of its customers will default their debts, it records an allowance of doubts debt to indicate the potential loss. Likewise, it may also reduce inventory when it declines in the market to a lower value than its cost less the market value.

The concept of prudence prevents the financial statement users against excessive optimism in financial reporting. It helps to promote reliability and credibility of financial information by promoting careful measuring and recognition.

5. The Materiality Concept

The concept of materiality appreciates the fact that not all financial information is equal. Information is deemed to be material when the omission or misstatement of such information is likely to affect the economic decision-making of financial statements users.

This means that accountants would pay more attention to important items that might influence their financial decision, and less attention to minor items.

An example is that a big company can expense office supplies that are small and not noted as an asset as its effect on financial reports is minimal. Nevertheless, large amounts of money like machinery or buildings should be well documented and reported.

Materiality assists in maintaining a balance between ensuring that financial statements prepared by an organization are practical and cost-effective and at the same time make the financial statements useful to users.

Accounting Conventions in Financial Reporting

Besides the ideas of accounting, accountants are also guided by a number of conventions in the application of their concepts in practice. These conventions are those practices that have been accepted and ensure uniformity and transparency in financial reporting.

Convention of Disclosure

Disclosure convention also stipulates that any and all the financial information that is pertinent and significant should be reported in a clear manner in the financial statements. This provides transparency and lets the users know the financial position of a company in a perfect way.

Disclosure can be in form of notes to the financial statements, explanations on the accounting policies and the details on contingent liabilities and risks.

Convention of Objectivity

The objectivity convention underscores the fact that financial information must be backed by verifiable evidence e.g. invoices receipts or contracts. This eliminates the bias and guarantees that the financial statements are founded on factual information and not personal opinion and estimations.

Objectivity is necessary in ensuring that trust is prepared in financial reporting and aiding the work of auditors to examine financial statements.

Convention of Conservatism

Though closely connected with the prudence concept, the convention of conservatism strengthens the notion that financial performance or position should not be overstated by accountants using accounting treatment.

To illustrate, in an environment of uncertainty, accountants can choose to use the method that causes lower reported profits instead of larger profits. This is a conservative way of ensuring credibility in financial reporting.

Convention of Consistency

The consistency convention is consistent with the concept of consistency mentioned above. It points out that the accounting methods must not change across time unless some reasonable reason is given. Whenever there are changes, they should be displayed in a manner that would allow users to read the financial information properly.

Importance of Accounting Concepts and Conventions

Financial accounting concepts and conventions play a fundamental role in providing useful financial information which is reliable. This can be explained by the importance which they have in various aspects.

1. Promoting Uniformity

These principles give companies a similar way of preparing financial statements by offering them a common moment of financial reporting. This standardization will minimize confusion and enhance the reliability of financial information.

2. Enhancing Reliability

Such concepts as prudence, objectivity, and accrual are aimed at giving the financial statements the economic reality as precise as possible. Dependable financial data is essential to investors, creditors and other parties who would be guided by the financial reports to make decisions.

3. Improving Comparability

Uniformity of accounting practice enables users to make comparisons between financial statements that are of different periods as well as financial statements of different companies. Comparability aids investors to assess a trend of performance and also to determine investment opportunities.

4. Supporting Decision-Making

Clear and precise financial reporting aids management, investors and regulators to make decisions. Decision-makers are always dependent on the financial reports that are prepared well to help them in assessing profitability, determining the risk, and or planning future strategies.

Relationship with Accounting Standards

Although accounting concepts and conventions are used to give a theoretical basis of financial reporting, accounting standards make these principles into specific rules and guidelines.

Most of these concepts are taken into consideration in international frameworks like International Financial Reporting Standards (IFRS), in order to provide consistency in global financial reporting. These standards improve transparency in the financial information of a growing global economy by harmonizing accounting between countries.

As an example, the IFRS standards are more focused on accrual accounting, disclosure transparency, and fair presentation of financial information. The standards are based on the previously mentioned accounting concepts and offer practical guidance on how the concept can be implemented.

Challenges in the implementation of Accounting Concepts

In spite of their significance, it is not always easy to apply the accounting concepts and conventions in the practice. Numerous financial dealings are related to judgment, estimates, and uncertainties.

As an example, the size of the business and the nature of the business may dictate the materiality of an item. Likewise, using the prudence principle entails judiciousness not to be too conservative thereby distorting financial outcomes.

Also, business landscape changes, emerging financial mechanisms and shifting regulation necessities can pose complexities in financial reporting.

Accountants need to incorporate technical expertise and professional judgment and ethics in response to these challenges.

Conclusion

Financial reporting systems today are based on accounting concepts and conventions. These principles make sure that the financial statements are reliable, consistent, and useful in decision making by making sure that the financial information is recognized, measured, and presented in a manner that is acceptable.

The theoretical foundation of the recording of financial transactions is the key concepts of accrual, consistency, going concern, prudence, and materiality, and the accounting conventions can be taken as practical procedures of the utilization of these concepts in practical cases. Collectively, they contribute to producing uniformity and transparency in financial reporting, which allow the stakeholders to rely on and compare financial information across organizations and time.

These principles are just as important today as the business environments across the globe keep on changing. They still remain the guiding principle that helps financial reporting to maintain its credibility, relevance, and usefulness in the decision-making process of the economic activity.

Get more well researched information about Accounting Concepts and Conventions here.