Introduction

In today’s dynamic and very competitive business world companies must make quick and efficient decisions. That is where management accounting comes in. As opposed to traditional accounting which mostly reports past financial actions, managerial accounting is forward looking and put in place to support internal decision making.

At the root of it, management accounting is what gives managers access to the info they need in terms of finance and also other areas for them to plan out, control, and assess business activities. It serves as a bridge between unstructured data and strategic actions which in turn helps companies to achieve their goals more effectively.

To that end you may wish to study this in depth which we present in our detailed guide to managerial accounting and which we present as very important in today’s organizations.

Understanding Management Accounting

Management reporting which is also referred to as managerial accounting is the preparation of financial and operational information for use by internal management. This includes analysis of data, interpretation of financial results and presentation of reports which in turn support managerial decision making.

In contrast to what is reported in financial accounting to stakeholders like investors and regulators, management accounting is for the internal users’ needs which include managers, executives, and department heads.

Management’s main goal in accountancy is to turn numbers into action oriented insights which in turn support decision making by way of detailed info on costs, revenues, budgets and performance metrics.

The Nature of Management Accounting

In some what which management accounting is characterized by the following:

1. Forward-Oriented approach.

Management is forward looking as opposed to being tied to the past. We do forecasting, budgeting and planning through which we help companies to look ahead at what is to come.

2. Decision Oriented.

It is a tool for management which is put in place to support informed decision making. In terms of pricing a product, expanding into new markets, or reducing costs management accounting puts forth relevant data for analysis.

3. Versatile and Adaptive

In contrast to financial accounting that is based on strict rules and standards, management accounting is flexible. Organizations may design their own systems according to their particular goals.

4. Interdisciplinary in Scope

Management accounting is a field which draws on many different areas of study which include finance, economics, statistics, and operations management. This makes it a very broad based tool for the assessment of business performance.

5. For internal use only

The information we present is for our internal use only, also we do not have external agencies’ review which enables us to customize.

6. Non-Financial and Financial Data

Management does not depend exclusively on financial numbers. Also included are what may be thought of as non-financial elements like that of employee performance, production efficiency, and customer satisfaction.

Scope of Management Accounting

Managerial accounting has a wide range of functions which extend into many areas of a business. It includes:

1. Cost Accounting

This includes the calculation of product or service costs. We see which resources are used and also which areas have room for cost reduction.

2. Budgeting and Forecasting

Management in the field of accounting includes the preparation of budgets and financial forecasts. These tools in turn help organizations plan for the future and allocate resources efficiently.

3. Financial Analysis

We look at financial reports to determine performance and identify trends.

4. Performance Evaluation

Management accounting reports on the performance of various departments and staff.

5. Decision-Making

It reports on which to base strategic choices like pricing, investment and expansion.

6. Risk Management

Through analysis of financial reports management accounting which in turn identifies possible risks and puts forth strategies to deal with them.

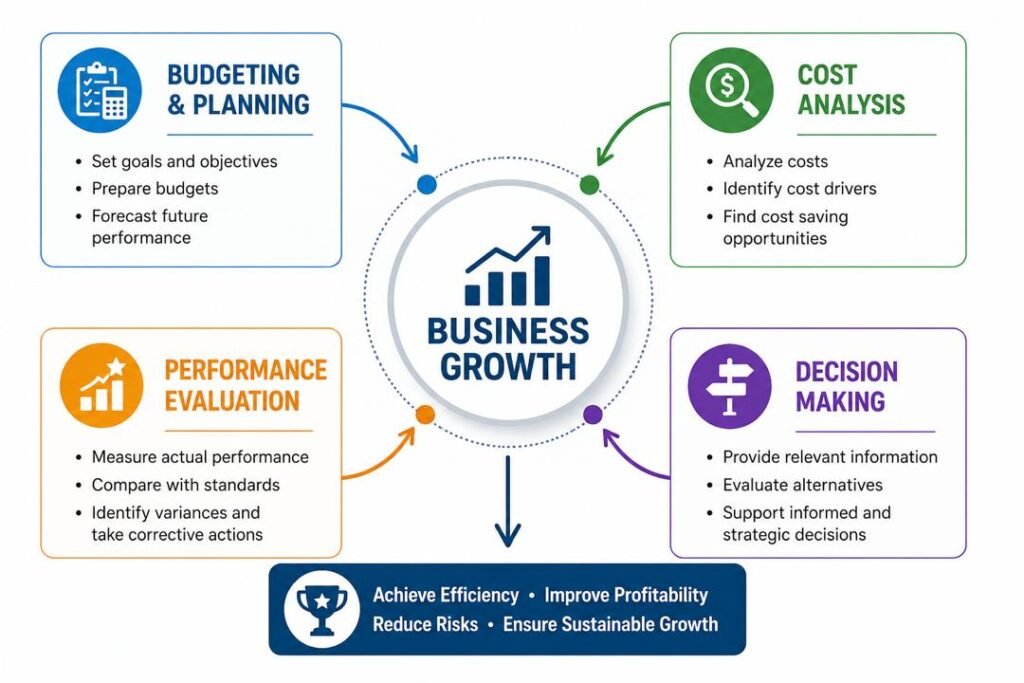

Core Functions of Management Accounting

Management reporting which plays a key role in the success of an organization:

Planning

Planning is a very key function. In managerial accounting we see that it is used to set goals and develop strategies to achieve those. Also through budgeting and forecasting managers are able to put forth what will happen in the future and allocate resources accordingly.

Regulating

Control of a process or resource involves the comparison of present performance with what was planned. Management accounting supplies tools like variance analysis which identify issues and enable corrective action.

Choice Determination

Management in turn gives out relevant info for decision making. For instance manager’s study cost volume profit relationships to determine a product’s profitability.

Assessment Report

It is a tool for evaluating the performance of departments, teams and individuals. We use key performance indicators (KPIs) to determine success and to identify what needs improvement.

Cost Control.

Cost out is key to profit improvement. Managerial accounting which in turn helps to identify waste and put in place cost saving measures.

Communication

Communication is also known as Management reporting which is what we see in managerial accounting improves the flow of info within the org by putting out clean and to the point reports which in turn promote transparency and accountability.

Tools and Techniques in Management Accounting

Management in the field of accounting uses a variety of tools and techniques which achieve its goals:.

Budgeting

Budgets are financial tools which present what is expected in terms of income and outgoings. They also serve as a base for performance review.

Standard Costing

We set out predetermined costs and then we compare them to actual costs to identify variances.

Variance Analysis

Variance analysis determines the gap between what was expected and what actually happened which in turn enables corrective action.

Break-Even Analysis

At the point where total revenue is equal to total cost this technique is used which in turn helps businesses determine their profitability.

Cost Volume Profit (CVP) Analysis

CVP analysis looks at the cost, volume, and profit relationship which in turn aids in decision making.

Activity-Based Costing (ABC)

ABC assigns resources to activities which in turn presents a more accurate picture of resource use.

Differences between Management and Financial Accounting

In that although management accounting and financial accounting report on financial data they do so for different reasons:

Purpose

Management accounting is for internal decision making, also financial accounting which is geared toward external reporting.

Users

Management accountants use certain tools which are applied within the company. External parties like investors, creditors and regulators use what financial accountants report.

Time Focus

Managerial accounting looks to the future while financial accounting looks at the past.

Flexibility

Management accounting is very adaptable and does not follow strict rules. In financial accounting we are tied to certain standards.

Level of Detail

Managerial accounting provides in depth specific reports but financial accounting gives out broad summaries.

Importance of Management Accounting in Business

Management accounting is a key element to an organization’s success. As for what that includes:

- Improved Decision-Making: Through provision of accurate and relevant data management accounting enables better decisions.

- Efficient Resource Allocation: It enables organizations to best put their resources to use which in turn produces the best results from present assets.

- Cost Control: Managerial accounting reports on which areas of expense can be cut without affect quality.

- Strategic Planning: It is a tool for long term planning which also gives out info on market trends and financial projections.

- Performance Improvement

Through the process of performance evaluation managerial accounting helps to identify strengths and weaknesses.

Management’s role in strategic planning

Strategic planning is about setting long term goals and which actions to take to achieve them. In this process managerial accounting plays a key role in:.

- Providing financial forecasts

- Analyzing market trends

- Evaluating investment opportunities

- Assessing risks

With this information managers may put forth plans that align to the organization’s goals.

Management Accounting and Decision-Making

The core of what managerial accounting does is decision making. Managers use accounting info to make which includes:

- Pricing Decisions: Setting the right price for a product is a function of cost, demand and competition.

- Investment Decisions: Management accounting is used to determine the profit of future investments.

- Make-or-Buy Decisions: Organizations that which products to make in house or outsource.

- Expansion Decisions: Management accounting issues out data which is used to determine the viability of entering new markets.

Challenges in Management Accounting

Despite that which is great about it, managerial accounting has issues of:

- Complexity: Advanced tools and techniques used in managerial accounting may present a complex picture.

- High Implementation Costs: Setting up a management accounting system is a costly affair which is true for small businesses in particular.

- Data Accuracy: Management quality is a function of data accuracy. Poor data leads to poor decisions.

- Resistance to Change: Employees may be resistant to new systems and processes.

The Evolving Role of Management Accounting

With the growth of technology the role of accounting in management is changing very quickly. Today’s organizations are into data analytics, artificial intelligence, and automation which they use to improve their accounting processes.

Management accountants are a different breed today; they are strategic partners which we see at the helm of business growth. They present perspectives that foster innovation and competitive edge.

Business Value of Managerial Accounting

The true worth of managerial accounting is in its ability to transform data into strategic insight. In many ways it adds to the value of businesses:

1. Enhancing Profitability

Through identification of cost saving options and improvement in efficiency managerial accounting which in turn increases profitability.

2. Supporting Growth

It has the data which will enable us to grow in to new markets.

3. Reducing Risks

Managerial accounting is a tool which identifies risk issues and develops strategies to deal with them.

4. Improving Accountability

Through measurement of results which in turn fosters accountability and transparency in the organization.

Real-World Application of Management Accounting

In today’s world management accounting is used in a variety of industries:

- Manufacturing firms use it for cost control.

- Retailers use it for inventory and pricing.

- Service organizations use that to increase efficiency and improve customer satisfaction.

In all industries management accounting is a key to business success.

Conclusion

Management accounting is a key component in today’s organizations. It goes beyond what is traditional accounting to provide action oriented information which supports in decision making, planning, and performance evaluation.

It’s adaptable and progressive which in turn makes it a great resource for managers which they can use to guide them through complex business settings. Through the use of both financial and non-financial information managerial accounting enables companies to achieve their strategic goals and to maintain that competitive edge.

While there are issues which managerial accounting presents it still has great value which it brings. As companies transform and grow in the coming years management accounting will only become more important which will in turn establish it as a fundamental element of good management and long term success.

Get more well researched information about Management Accounting here.