Introduction

Corporations are the next stage of development of businesses that start their life as sole proprietorships and partnerships but switch to a corporate form to get access to more capital. Such a change brings in the increased complexity of financial structures and reporting requirements, which are the domain of corporate accounting. Understanding share capital, issue and redemption of shares, the means by which companies raise funds, the ways in which they invest funds in the hands of the shareholders and also how they record these transactions is the crucial part of any student who wants to take a step forward in accounting into the more sophisticated financial practices.

Through this article, we shall discuss the basics of company accounts i.e. the share capital, issue of shares and redemption of shares. We shall also analyze the accounting treatments, journal entries and regulatory considerations in such transactions.

Understanding Share Capital

What is a Share Capital?

Share capital is the money that is raised by the company by issuing shares to investors. It is the ownership right in the firm and constitutes a significant component of the shareholders equity in the balance sheet.

When shareholders buy shares, they become co-owners of the company and have a right to dividends and voting rights based on the nature of the shares they own.

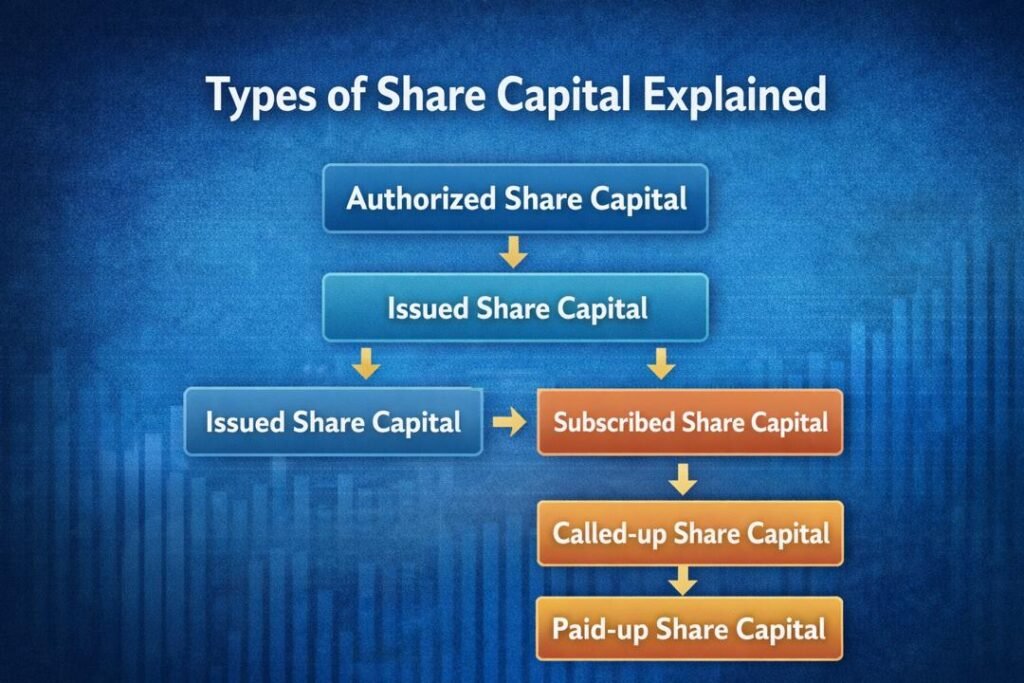

Types Share Capital

- Authorized Share Capital: This is the maximum amount of capital a company is allowed to raise as stated in its Memorandum of Association.

- Issued Share Capital: The share of authorized capital, which the company has floated to the investors

- Subscribed Share Capital: The amount of the issued capital that investors have accepted to buy

- Called-up Share Capital: The value at which the firm has called on the shareholders to pay

- Paid-up Share Capital: The sum actually remitted to shareholders.

- Reserve Capital: Capital that is not available except when it is required to be called upon during liquidation.

Types of Shares

1. Ordinary Shares (Equity Shares)

These are ownership and they are accompanied with voting rights. Dividends are variable.

2. Preference Shares

They offer stable dividends and take precedence over equity shares in liquidation but do not typically have any voting rights.

Share Capital Accounting

Upon the issuance of shares, accounting entries are done to indicate the incoming flow of money and the generation of equity.

Example: Issue of Shares at par

Assuming that a company issues 10,000 shares at ₦10 each:

Journal Entry:

- Debit Bank Account ₦100,000

- Credit Share Capital ₦100,000

This implies that the company has received cash and raised its equity.

Issue of Shares

One of the major sources of raising capital by companies is issuing shares. The issues of shares may be made in different forms:

1. Issue at Par

Stocks are sold at nominal (face) value.

Example:

The issue price of this share is ₦10 (10).

Journal Entry:

- Debit Bank Account

- Credit Share Capital

2. Issue at a Premium.

The shares are issued at a higher price than they are worth. The surplus is referred to as securities premium.

Example:

A ₦10 share issued at ₦12.

Journal Entry:

- Debit Bank Account ₦12

- Credit Share Capital ₦10

- Credit Securities Premium ₦2

Application of Securities Premium

- Writing off preliminary expenses.

- Issuing bonus shares

- Writing off- discount on issue of shares.

3. Issue at a Discount.

Shares are issued at lower-than-nominal value. This is a highly regulated and frequently constrained practice.

Example:

A ₦10 share issued at ₦9.

Journal Entry:

- Debit Bank Account ₦9

- Debit Discount on Issue of Shares 1.00.

- Credit Share Capital ₦10

4. Other than Cash Issue of Consideration.

Firms can issue shares as substitutes to assets or services.

Example:

Equity issues to purchase equipment.

Journal Entry:

- Debit Machinery Account

- Credit Share Capital

5. Calls on Shares

Share payments can be made in parts:

- Application

- Allotment

- First Call

- Final Call

Individual accounting entries are necessary in each stage.

Example Entry for Allotment:

- Debt Share Allotment Account.

- Credit Share Capital

Forfeiture of Shares

In case a shareholder does not pay calls, he is likely to lose the shares.

Journal Entry:

- Debit Share Capital

- Credit Share Forfeiture Account.

- Credit Calls in Arrears.

The shares that are forfeited can be reissued in future.

Reissue of Shares of Forfeit

The reissued shares may be sold at par, premium or at a discount (but not more than the amount forfeited).

Example Entry:

- Debit Bank

- Debit Share Forfeiture (when discount allowed).

- Credit Share Capital

Redemption of Shares

What is Redemption?

Redemption is the process where a company repurchases its shares, usually the preference shares, to the shareholders.

This dilutes the firm share capital and reimburses the investors.

Conditions for Redemption

- Shares should be paid in full.

- Redemption should be out of:

- Profits to be paid in dividend, or

- Proceeds of a fresh issue.

- In case of redemption out of profits, a Capital Redemption Reserve (CRR) needs to be established.

Accounting for Redemption

Scenario 1: Redemption Out of Profits.

Steps:

- Move profits to CRR.

- Pay shareholders

Journal Entries:

- Debit Retained Earnings

- Credit Capital Redemption Reserve.

- Debit Preference Share Capital.

- Credit Bank

Scenario 2: Redemption out of Fresh Issue.

A company can also use redemption to issue new shares.

Journal Entries:

- Existing shareholders can be persuaded to issue new shares.

- Debit Bank

- Credit Share Capital

- Redemption

- Debit Preference Share Capital.

- Credit Bank

Premium on Redemption

In case redeeming the shares at a premium:

Example:

Redeeming ₦10 shares at ₦12

Journal Entry:

- Debit Preference Share Capital ₦10.

- Debit Redemption Premium ₦2.

- Credit Bank ₦12

The premium is normally countered against securities premium or retained earnings.

Buyback of Shares

Buyback is analogous to redemption and is primarily used to equity shares.

Reasons for Buyback

- Grow earnings per share (EPS).

- Return excess cash to shareholders.

- Improve financial ratios

Accounting Entry

- Debit Share Capital

- Debit Reserves

- Credit Bank

Financial Statements Presentation

Balance Sheet (Equity Section)

- Share Capital

- Securities Premium

- Capital Redemption Reserve

- Retained Earnings

Notes to Accounts

Disclosures should be detailed and should include:

- Number of issued shares.

- Rights on shares.

- Movements in share capital.

Regulatory Considerations

Laws and standards govern corporate accounting so as to bring transparency and fairness.

Key Regulations

- Company Law: Governs share issuance, redemption, and disclosures.

- Accounting Standards: Make sure there is unified reporting (e.g. IFRS).

- Stock Exchange Rules: Submit applications to listed companies.

Restrictions and Safeguards

- No discounted issue of shares (except, of course, on certain conditions)

- Redemption should not be a disadvantage to creditors.

- It is required to be properly disclosed.

Importance of Share Capital Management

Share capital is managed well to assist companies:

- Maintain financial stability

- Attract investors

- Make sure that regulations are met.

- Optimize capital structure

Transition from Basic to Corporate Accounting

The transition between basic accounting and corporate accounting entails the knowledge of:

- Complex equity structures

- Legal compliance requirements

- Advanced journal entries

- Financial statement disclosures

Corporate accounting presents new ideas which extend beyond mere income and expense monitoring, which deals with ownership, investment and management of capital.

Practical Illustration

Let’s consider a company that:

- Issues 5,000 shares at ₦10 each

- Redeems 2,000 preference shares at ₦12.

Issue Entry:

- Debit Bank ₦50,000

- Credit Share Capital ₦50,000

Redemption Entry:

- Debit Preference Share Capital N20,000.

- Debit Premium on Redemption 04,000.

- Credit Bank ₦24,000

This case indicates the way capital inflows and outflows are reported.

Common Mistakes to Avoid

- Misleading issued and paid-up capital.

- Improper treatment of premium.

- Ignoring regulatory requirements

- Miscalculating redemption reserves

Conclusion

Learning of company accounts is an important process to acquire knowledge of the current accounting practices. The pillar of corporate financing is the share capital, the issuing and redeeming shares are the major mechanisms of money regulation and relations with investors.

Accountants can give meaningful information about the financial health of a specific company by learning how to document these transactions correctly and adhere to the regulations. A switch to corporate accounting leads to more professional financial positions and a better insight into how businesses are run at a bigger scale. Having a good understanding of the share capital, share issuance and redemption, you are half way in becoming an expert in corporate financial management.

Learning company accounts is an essential process of learning contemporary accounting practices. The backbone of corporate financing is share capital and the issuance and redemption of shares are important means of managing finances and retaining investor confidence. Such processes do not only dictate the manner in which a firm raises capital, but also the manner in which it maintains and reorganizes its financial status in the long term.

Accountants can also maintain transparency and accuracy in financial reporting by understanding how to accurately record share transactions, account premiums and discounts, and adhere to legal and regulatory systems. The knowledge is not only necessary to enhance business development, attracting investors, and protecting the interest of the stakeholders.

Moreover, a good understanding of such concepts will enable professionals to interpret corporate financial statements in a more effective way and make informed decisions. The importance of corporate accounting in the accountability and sustainability of businesses is growing as they continue to grow and develop.

Finally, acquisition of share capital, issue and redemption of shares makes the learners have skills and confidence to learn the more advanced concepts of corporate financial management as a bridge to a wider career in the accounting and finance profession.

Get more well researched information about Share Capital, Issue and Redemption of Shares here.