When you’re running a small business, access to capital can be a game-changer. Whether you’re looking to open a new location, update your equipment, or boost your working capital, securing the right funding is critical to taking your business to the next level. For many small business owners, SBA loans are one of the best financing options available. But what exactly are SBA loans, and how can you successfully apply for one?

This guide will walk you through everything you need to know about SBA lending, from its benefits and loan types to eligibility requirements, application tips, and more.

What Are SBA Loans?

SBA loans are small-business loans partially guaranteed by the US Small Business Administration. Essentially, the SBA partners with lenders—such as banks, credit unions, and other financial institutions—to reduce the risk of lending money to small businesses. By providing this guarantee, SBA loans make it easier for small businesses to access funding that they might not otherwise qualify for through traditional means.

The key appeal of SBA loans? They often come with lower interest rates, longer repayment terms, and more flexible requirements compared to other types of business financing.

Benefits of SBA Lending for Small Businesses

Why are SBA loans such a popular choice for entrepreneurs? Here are a few key benefits to consider:

- Lower Interest Rates: SBA loans provide competitive interest rates compared to conventional loans. This ensures your monthly payments are manageable and improves cash flow.

- Longer Repayment Terms: The extended repayment terms (often 10-25 years, depending on the loan type) mean you have more time to pay off the loan, which can lessen the financial burden.

- Smaller Down Payments: SBA loans often require lower down payments than traditional loans, making it easier for small businesses to secure the financing they need.

- Flexible Use of Funds: Depending on the specific loan type, SBA loans can cover everything from equipment purchases and real estate to working capital and debt refinancing.

These benefits make SBA loans a lifeline for small businesses needing affordable, reliable funding.

Types of SBA Loans Available

The SBA offers several types of loans to meet the unique needs of different businesses. SBA Loan Calculator to review breakdown of the most popular options:

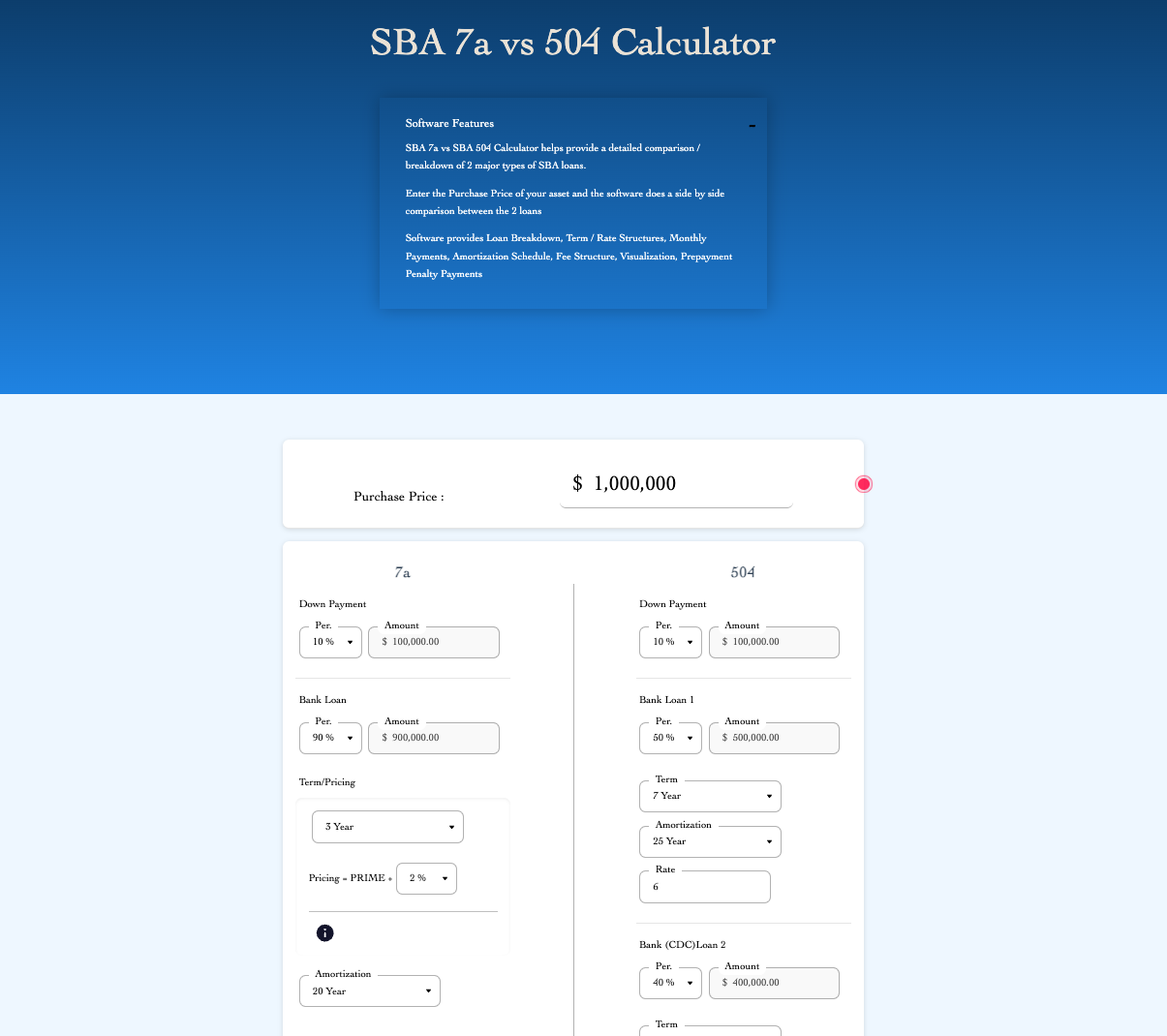

1. SBA 7a Loan

This is the most common SBA loan program and is highly versatile. Use it for working capital, equipment, real estate, or even debt refinancing. Loan amounts can go up to $5 million.

2. SBA 504 Loan

Best for large investments like purchasing fixed assets (e.g., machinery or commercial real estate), the 504 loan provides long-term financing with a focus on economic development.

3. SBA Microloan

Need a small loan? The SBA Microloan program offers loans up to $50,000, perfect for startups or businesses needing a boost in working capital.

4. SBA Disaster Loans

Designed to assist businesses affected by declared disasters, this program helps cover repair costs, operating expenses, and lower-interest financing for recovery.

If none of these seem like the right fit, it’s worth checking out the other SBA loan programs specifically tailored to exporters, veteran-owned businesses, and more.

Eligibility Requirements for SBA Loans

Every SBA loan comes with its own set of requirements, but there are some general eligibility criteria all applicants must meet:

- Business Size: Your business must meet the SBA’s size standards, which vary by industry.

- Location: The business must operate within the U.S. or its territories.

- Profit Motive: The business should operate for profit; non-profits are typically not eligible.

- Owner Investment: Owners must have personally invested time and/or money in the company.

- Financial Health: While SBA loans cater to small businesses, lenders still look for strong financials, acceptable credit scores, and the ability to repay the loan.

Additionally, if you can access funding through alternative means (e.g., personal assets or another loan), you may have trouble qualifying for an SBA loan.

The SBA Loan Application Process

The SBA loan application process may seem daunting at first, but breaking it down step-by-step can help make it manageable. Here’s what you can expect:

- Prepare Your Business Plan: Lenders want to see a detailed yet concise business plan, including your financial projections, goals, and strategies.

- Complete Necessary Paperwork: This includes loan applications, tax returns, and financial statements. You’ll also need to submit a personal financial statement.

- Choose a Lender: Not all lenders offer SBA Loans, so make sure you’re working with one that does.

- Work with Your Lender: Your selected lender will help guide you through the SBA loan packaging process, completing the required SBA forms and submitting your application for approval.

- Wait for Approval: Once submitted, applications can take weeks to months for approval, depending on the complexity of the loan and lender preferences.

Pro tip: Organize all your documents ahead of time to minimize delays.

Tips for a Successful SBA Loan Application

Want to boost your chances of securing an SBA loan? Here’s how to strengthen your application:

- Check Your Credit Score: A strong credit score increases your credibility, so address any errors or outstanding issues on your report before applying.

- Be Realistic About Loan Amounts: Base your loan request on what you genuinely need (and can repay).

- Provide Detailed Financials: Show your business’s financial health with accurate, up-to-date financial statements, including balance sheets, income statements, and cash flow statements.

- Have a Clear Plan for the Funds: Lenders want to know how the loan will help your business grow or solve a specific challenge.

Common Mistakes to Avoid When Applying

Navigating SBA loans can be tricky, and mistakes could jeopardize your chances. Here are some common pitfalls to watch out for:

- Insufficient Documentation: Missing or incomplete files may delay or derail your application.

- Unclear Business Plan A lackluster business plan can raise red flags for both lenders and the SBA.

- Requesting the Wrong Loan: Make sure the loan type suits your needs to avoid application rejection.

- Applying without Creditworthiness: Check your credit to ensure you meet baseline requirements.

Steer clear of these errors to maximize the likelihood of your application’s success.

SBA Loan Alternatives

If an SBA loan doesn’t work out, don’t worry! Here are some alternative funding options you can consider for your business needs:

- Business Lines of Credit: Access funds on an as-needed basis for working capital.

- Merchant Cash Advances: Get an advance on future sales, though at a higher cost.

- Online Small Business Loans: Tech-savvy platforms like Kabbage or Fundera offer faster (albeit potentially pricier) lending options.

- Grants and Competitions: Check for small business grant opportunities or pitch competitions in your local area or industry.

Is an SBA Loan Right for You?

SBA loans can be a powerful way to fund your business, but they’re not always the perfect solution for every entrepreneur. By understanding the benefits, requirements, and process, you can determine whether SBA lending meets your needs or if an alternative option might work better.

Nice blog! Is your theme custom made or did you download it from somewhere? A design like yours with a few simple tweeks would really make my blog stand out. Please let me know where you got your theme. Appreciate it

Very interesting topic, thanks for posting.

Perfect piece of work you have done, this website is really cool with superb info .

Some truly interesting information, well written and generally user friendly.

Only wanna remark on few general things, The website layout is perfect, the articles is very great : D.