Introduction

In the modern competitive business world, organizations need information that is sound and reliable so as to make good economic decisions. Being a small startup or a multinational corporation, the business has to constantly review the performance, optimize its resource usage, and stay responsible to the stakeholders. It is in this context that accounting is crucial. The nature and scope of Accounting is not just a process of copying figures or making financial statements but it is a systematic process that assists in planning, control, evaluation and communication in an organization.

Accounting is the language of business as it is the standard structure by which the financial activities are quantified, assessed, and reported. The nature and scope of Accounting is used to evaluate the profitability of a business, financial position, cost management and regulatory obligations. More to the point, accounting allows the stakeholders, including investors, creditors, managers and regulatory authorities to make sound decisions using correct and pertinent financial data.

The conceptual framework is the central point of accounting and is available to determine how financial information is identified, measured, presented, and interpreted. Accounting conceptual framework facilitates consistency, transparency, and reliability of financial reporting therefore increasing the level of trust and credibility of business activities.

This paper discusses the concept, scope, and nature of accounting in the context of its conceptual basis, role in the economy, and strategic significance. It brings out the role of accounting in supporting financial reporting, cost measurement, accountability and compliance with regulations which makes accounting a technical and a strategic business instrument.

The Nature of Accounting

Accounting may be described as a methodological way of determining, documenting, quantification, categorizing, summarization, interpretation and relaying of financial data. It concerns mainly economic activities which may be monetized.

The following key features can be used to describe the nature of accounting:

1. Accounting as a Measurement System

Business activities are quantified in money in accounting. All transactions are recorded in monetary units e.g. sales, purchases, salaries or acquisition of assets. This enables businesses to perform a comparative analysis of the performance over time and assess the financial performance objectively.

2. Accounting as an Information System

Financial statements and reports are used to process the raw financial data into meaningful information compiled by accounting. These outputs give information on profitability, liquidity, solvency and efficiency of operations.

3. Accounting as a form of Communication

The accounting conveys financial data to both internal and external users. Financial reports are used to provide stakeholders with knowledge of financial status of an organization.

4. Accounting as a Social Science

Even though the use of accounting involves the application of numbers, it is not completely devoid of judgment, estimation and interpretation. Accountants use professional judgment when it comes to depreciation, valuation and revenue recognition.

5. Accounting as a Service Activity

The purpose of accounting is to be able to answer the needs of the users through giving relevant and reliable financial information that they can use in form of decision making.

Essentially, accounting is the kind of activity that has a dual nature, as it is considered a technical process, and also a decision supporting system.

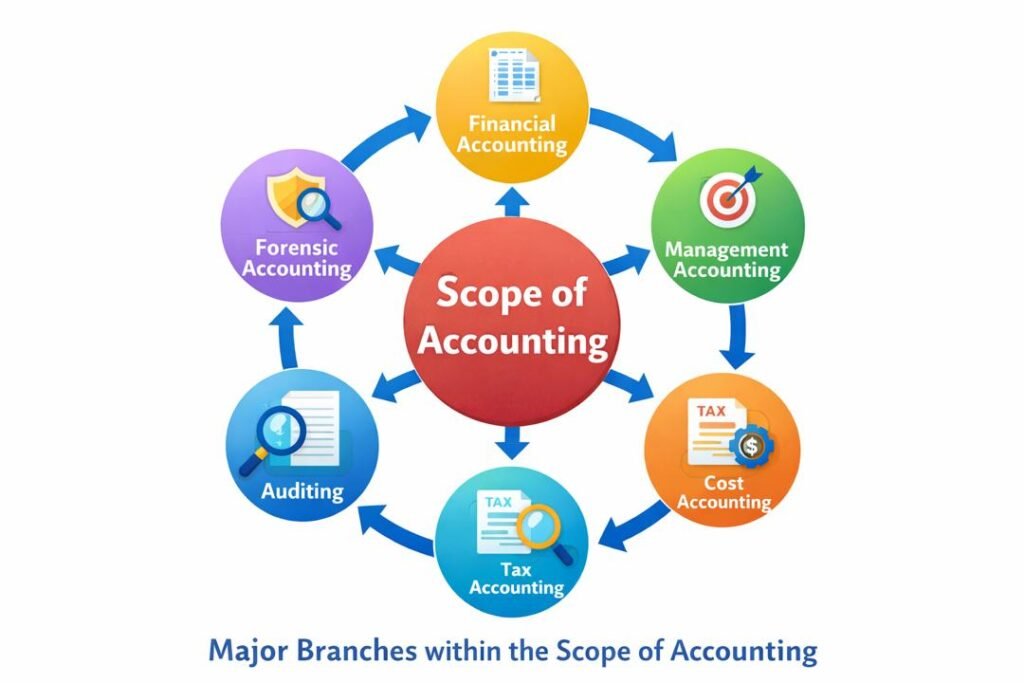

The Scope of Accounting

The area of accounting can be defined as the extent of the activities and functions of accounting in an organization. Accounting does not just deal with just book keeping, but spreads out in many different spheres of business operations.

Financial Accounting

Financial accounting is concerned with presenting financial statements to outsiders like the investors, creditors, regulators and the general population. It entails preparation of:

- Financial Position (Balance Sheet) Statement.

- Income (Profit and Loss Account) Statement.

- Cash Flow Statement

- Statement of Changes in Equity.

Such reports are based on standardized rules and principles to guarantee comparability and reliability.

Management Accounting

Management accounting gives non-financial and financial information to make internal decisions. It assists in the planning process, budgeting, performance analysis, and strategy analysis.

Cost Accounting

The cost accounting stresses on calculating the cost of production or service delivery. It assists organizations to manage costs, price determination and efficiency.

Tax Accounting

Tax accounting is concerned with tax preparation and tax compliance. It takes care of the businesses to comply with their statutory obligations as well as reducing tax liabilities in accordance with the law.

Auditing

Auditing refers to the unbiased review of financial accounts so as to make sure that they are accurate and in accordance to the accounting principles.

Forensic Accounting

Forensic accounting involves the use of accounting expertise in matters of fraud, financial misconduct and litigation.

The extensive nature of accounting indicates the fact that it is entrenched in all of business practices.

The Conceptual Framework of Accounting

Conceptual framework of accounting is a collection of principles, concepts and guidelines on which financial reporting are based. It offers rational framework in the formulation of accounting standards and brings uniformity in the financial practices.

Purpose of the Conceptual Framework

The key goals of the conceptual framework are:

- To influence the formulation of accounting standards.

- To eliminate the accounting problems in which no standard is available.

- To make comparison and transparency more effective.

- To enhance quality of financial reporting.

Important elements of the Conceptual Framework

1. Financial Reporting Objectives

The ultimate purpose of the financial reporting is to make financial data helpful to the stakeholders in making economic decisions. This will contain details of:

- Financial performance

- Financial position

- Cash flows

2. Qualitative Characteristics of Financial information

The useful financial information must have some properties:

- Relevance: Information is supposed to play a role in decision-making.

- Honest Representation: The information should be full, impartial and devoid of inaccuracy.

- Comparability: The users are expected to be in a position to compare information over time and across organizations.

- Verifiability: The information must be backed with evidence.

- Timeliness: Data must be made timely when required.

- Understandability: The information must be simple to understand.

3. Financial Statements Elements.

The framework outlines the important elements which include:

- Assets

- Liabilities

- Equity

- Income

- Expenses

These are the building blocks of financial statements.

4. Recognition and measurement

Recognition is the process of determining when an item is to be recorded in financial statements and the other is the process of attaching monetary values to an item either by historical cost, fair value, or present value.

The Economical Use of Accounting

In the economic systems, accounting is one of the main components that facilitate effective distribution of resources. It allows the firms to quantify the economic activities and report the financial performance to the market.

Resource Allocation

The accounting information is used by investors in making decisions on where to allocate their money. Proper financial reporting will make sure that the capital is invested in productive and profitable businesses.

Performance Evaluation

Accounting assists in the review of business performance in terms of profitability ratios, percentage of returns on investment, and cost analysis.

Economic Stability

Accounting systems that are reliable enhance transparency and accountability that are fundamental towards ensuring trust in the financial markets.

Financial Reporting and Stakeholder Decision-Making

One of the greatest roles of accounting is financial reporting. It offers formalized information, which is helpful to different stakeholders:

- Investors: Financial reports help investors to evaluate profitability, risk and growth potential before investing.

- Creditors and Lenders: Banks and creditors analyze liquidity, solvency and cash flow to know whether a company is credit worthy.

- Management: Managers make use of accounting information in strategic planning, budgeting and performance control.

- Regulatory Bodies: Financial reports are used to guarantee that the regulators are in compliance with laws and standards.

- Employees and the Public: Employees will gauge job security and stability of the organization whereas the population gauges corporate responsibility.

Cost Control and Measurement

Cost measurement is a vital factor of accounting which facilitates efficiency and profitability of operation.

Importance of Cost Measurement

- Helps set the price of the products.

- Facilitates budget and forecasting.

- Improves cost control

- Increases profitability reporting.

Standard costing, marginal costing and activity-based costing are some of the methods that organizations can use to identify inefficiencies and optimize resource use.

Accountability and Stewardship

Accountability is among the core functions of accounting. Managers are also charged with the organizational resources and are supposed to prove responsible utilization of the resources.

Accountability in Accounting

Accounting ensures that:

- The bookkeeping of financial activities is recorded.

- Assets are safeguarded

- Lack of proper management and fraud are reduced.

- Management can be assessed by the stakeholders.

This notion is also referred to as stewardship where the management is considered to be a custodian of organizational resources.

Regulatory Compliance in Accounting

The accounting environment is regulated by laws, standards and professional standards.

Importance of Regulatory Compliance

- Ensures transparency

- Guarantees investors and creditors

- Promotes ethical behavior

- Enhances market confidence

Adherence to accounting standards will make financial reporting similar in organizations and industries.

Accounting as a Strategic Business Tool

In addition to technical purposes, accounting is a strategic tool that is useful in promoting business success over time.

Accounting Strategic Roles:

- Favors business planning and forecasting.

- Helps in managing performance.

- Improves competitive advantage.

- Helps in managing risk.

- Makes the decision on investment.

In other words, modern accounting systems combine financial information and strategic goals and therefore, accounting is a part of organizational strategy.

Conclusion

Accounting is much more than a standard practice of documenting transactions. It is an extensive framework providing measurement, processing, and communication of financial data that is necessary in economic decision-making. Accounting has a conceptual framework that offers a reliable, transparent, and accountable financial reporting.

The nature and scope of Accounting indicates that the accounting is a measurement, communication, and information system, but its scope is extensive to the financial accounting, management accounting, cost accounting, auditing, and regulatory compliance. Accounting fosters the stakeholders by giving them information on financial performance, resource usage, and the stability of the organization.

Accounting is a technical field and a strategic business instrument by allowing the control of costs, accountability, regulation, and strategic planning. Finally, accounting is the backbone of the quality business decision making, which has resulted in a sustainable growth, economic stability, and corporate prosperity in the world that is becoming ever more complicated.

Get more well researched information about the nature and scope of accounting here.