Introduction

The financial accounting is the key to the contemporary business systems. It also presents systematic, standardized and regulated financial data to its external users like investors, creditors, regulators and the rest of the community. Organizations use financial statements (income statements, balance sheets, cash flow statements and statements of changes in equity) to convey their performance and financial standing. Nonetheless, even in terms of its significance, financial accounting is not flawless. The limitations of financial accounting are being increasingly important in the contemporary dynamic, technology-driven, and knowledge-based economy.

The article focuses on inherent limitations of financial accounting in terms of historical bias in cost, no future facing information, lack of qualitative information and managerial judgment manipulations. It also assesses the effects of such constraints on stakeholder interpretation and compares financial accounting and management accounting to explain their contextual constraints.

1. Historical Cost Bias

Financial accounting has many of the most notable weaknesses, the most noticeable of them all being that it uses the historical cost principle. In traditional accounting systems like the International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP), the current market price of assets and liabilities is not usually taken into account but rather the initial purchasing price is taken into account.

Distortion of Asset Values

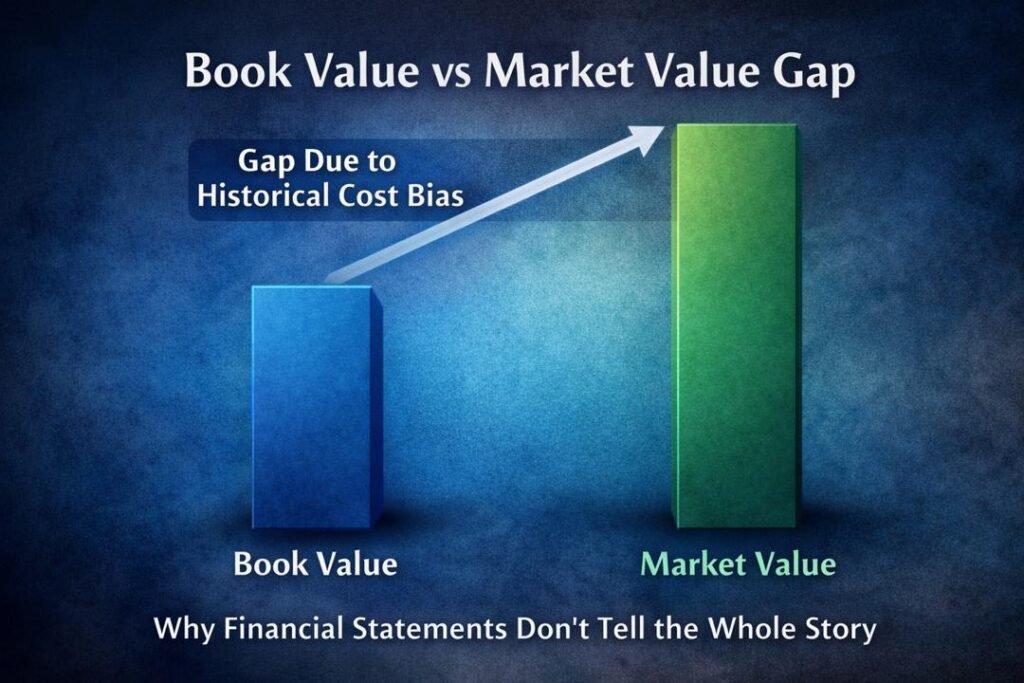

Historical cost accounting is an accounting approach which presupposes that original transaction price is objective and verifiable. Although this increases reliability, it compromises relevance. An example of this is the land that was obtained several decades back might be recorded on the balance sheet at a fraction of its current market value. On the other hand, the technology assets can be deterred at a high cost of acquisition even when they become obsolete.

Financial statements can be grossly misleading in an environment full of inflation. Older cost allocations may result in understating of assets, inaccuracy of depreciation charges and overstated profits.

Effect on the Decision of Stakeholders

Investors who use financial statements to make their decisions might undermine or overvalue the real economic worth of a company. Creditors can fail to assess the strength of collateral and analysts can come up with incorrect financial ratios. This limitations of financial accounting can be usually seen in the gap between book value and market value.

Whereas fair value accounting has been implemented to deal with some of these problems, it has its own critic, which is volatility and increased reliance on estimations.

2. The absence of Future-Oriented Information

Financial accounting is backward looking in nature. It documents the previous transactions and occurrences, but offers little information about the future opportunities.

Absence of Forecasting Data

Financial statements result in a summary of what has already taken place in a reporting period. They do not provide:

- Revenue projections

- Market expansion plans

- Understandings of competitive strategy.

- Innovation pipelines

In a constantly changing business environment, especially in some of the more dynamic industries such as in technology, renewable energy, or digital services, what is possible in the future may be more important than what has been achieved in the past.

Strategy Decision-Making Constraints

The stakeholders are also seeking predictive information more. Investors desire to learn about the upsurge chases, peril encounter, and sustainability strategies. However the accounting systems limit the forward-looking statements because of the reliability and legal liability issues.

This causes users to need to use supplementary disclosures including management commentary or external analyst reports. This segregation lessens the understanding of financial statements.

3. Omission of Qualitative Information

The other major shortcoming is the fact that financial accounting focuses on measurable monetary information.

Intangible Assets and Intellectual Capitals

The intangible resources that give value to modern businesses include:

- Brand reputation

- Customer loyalty

- Employee expertise

- The ability to conduct research and development.

- Organizational culture

Internally generated intangible assets are however hardly ever recognized in the financial statements except when obtained externally. As an example, the internal brand can be a powerful brand, yet it is not considered as an asset, but a bought brand is.

This omission brings about a lack of correspondence between economic reality and accounting reflection.

Social and Environmental Impact

In the modern business setting, stakeholders are concerned with environmental sustainability, social responsibility and governance practice. Whereas frameworks are taking into consideration sustainability reporting, classic financial accounting dwells more on financial metrics.

As such, an organization that has high social impact can look like an organization with low ethical standards on financial reports as long as their financials are similar.

4. Susceptibility to Manipulation through Judgment

Financial accounting is claimed to provide objectivity and comparability but it does have a managerial aspect to it. This brings in manipulation space.

Accounting Estimates and Assumptions

Financial reporting involves estimations concerning:

- Depreciation methods

- Useful life of assets

- Bad debt provisions

- Inventory valuation

- Impairment assessments

These estimates are capable of having a huge bearing on the profits reported and the value of assets. Even under allowable standards, managers would be discretion to smooth earnings or raise positive results.

Earnings Management and Creative Accounting

As it has been proven in history, accounting manipulation acts as a source of misleading stakeholders. The downfall of businesses like Enron revealed the extent to which aggressive accounting can misrepresent the financial reality even being in accordance with the formal standards.

Although regulatory authorities have enhanced regulation since such scandals, accounting based on judgment has ethical issues.

5. Standardization vs. Flexibility: A Structural Constriction

Financial accounting is meant to be uniform and comparative between entities. Contextual nuance may however be constrained by standardization.

Various industries are run with various risk profiles and value drivers. However, standardized reporting systems are trying to use general principles in a universal way. This may end up in financial statements which may not be able to capture any industry-specific dynamics.

One example is that, technology firms that spend a lot of money on research can seem to have less profit, as they expense research and development, but manufacturing firms that have taken advantage of physical resources can seem to have larger asset bases.

6. Effects on the Interpretations and Decision-Making of Stakeholders

Financial accounting has serious limitations that affect interpretation of data and decision-making by the stakeholders.

Investors

Financial statements are used by the investors in valuation and risk assessment. Historical cost bias and failure to look into the future may result in:

- Mispricing of shares

- Excess dependencies on earnings per share.

- Lack of knowledge of innovation potential.

The impact of this is usually the tendency of investors to complement accounting information with market research and industry analysis.

Creditors

Through accounting data, creditors evaluate credit capacity and solvency in terms of the financial ratios. Credit risk assessment can be faulty in case the asset values are old and the estimates could be overly optimistic.

Management

Paradoxically, financial accounting is not the one that is intended to be used in internal decision-making. Financial accounting does not provide managers with detailed cost behavior analysis, budget forecasts and operational metrics.

The regulators and policymakers

Financial statements help the regulators in taxation and monitoring compliance. Both the tax income and economic control may be infiltrated by manipulation or estimation bias.

7. Contrasting Financial Accounting and Management Accounting

When the contextual boundaries of financial accounting are to be known, they need to be compared with management accounting.

Purpose and Audience

Financial accounting works in the interest of external users and follows standardized systems, such as IFRS and GAAP. Management accounting on the other hand is in-house and does not follow rigid regulatory formats.

Time Orientation

- Financial accounting: Periodic and historical.

- Management accounting: Progressive and proactive.

The management accounting encompasses budgeting, strategy planning, the variance analysis, and forecasting.

Qualitative and non-financial Data Inclusion

Management accounting incorporates non-financial measures of customer satisfaction, efficiency of operations and production schedules. It can employ performance dashboards and balanced scorecards.

Flexibility

Management accounting is flexible to suit the needs of an organization as compared to financial accounting which lays emphasis on comparability and compliance.

8. Contemporary Business Environment: Growing Dynamism of the Limitations

The digital economy increases the vulnerabilities of the traditional accounting systems.

Knowledge-Based Assets

Firms in such industries as software, artificial intelligence, and biotechnology generate value based mostly on intellectual capital. However, internally generated intangible assets are difficult to record using financial accounting.

Globalization and Volatility

Business environments are dynamic due to global supply chains, currency changes and quick changes in technology. The past financial information can soon get outdated.

ESG and Sustainability Requirements

ESG measures of environmental, social and governance are becoming paramount to the investors. The conventional accounting financial frameworks are less than comprehensive in the dimensions.

Is it possible to Improve Financial Accounting?

Although the limitations are still in place, accounting standards are still being reformed.

- Extended measurement of fair value.

- Increased disclosure provisions.

- Integrated reporting projects.

- Increased openness of assumptions.

Nevertheless, there exist trade-offs between the relevance and the reliability, comparability and flexibility, objectivity and judgment.

Financial accounting can never meet all information requirements of stakeholders since its primary purpose is not to think long-term or to measure all of the value, but to report on financial performance in a systematic manner.

Conclusion

The transparency, comparability, and accountability of the contemporary economies would not be achievable without financial accounting. However, the limitations of financial accounting such as bias on historical cost, unavailability of future oriented information, omission of qualitative information and the tendency to be affected by the judgment of the managers, limit its capacity to reflect an entire economic view.

Such constraints influence the interpretation of financial information and decisions made by investors, creditors, regulators and the managers. Though financial accounting forms a common ground, it should be surrounded with management accounting tools, market analysis, and strategic disclosures in order to create a complete picture of organizational performance.

Under the changing environment of business in the world, it is very important to be aware of the contextual scope of financial accounting. Instead of considering it a wholesome decision-making resource, the stakeholders are to consider it a part of the larger informational ecosystem. It is only at this point that financial data can be viewed with a critical and responsible interpretation towards sustainable and informed decision making.

Get more well researched information about the Limitations of Financial Accounting here.