Introduction

In a globalized economy where businesses, investors and governments are becoming more interdependent, financial information is needed that has an element of reliability, comparability and transparency across borders. Evolution of accounting standards from IASC to IFRS represents one of the most significant developments in modern financial reporting. The disparity in the accounting rules in different countries used to complicate the comparison of financial statements prepared in various countries. To find a solution to this dilemma the international accounting regulation concept came in as a joint attempt to standardize the financial reporting standards across different countries.

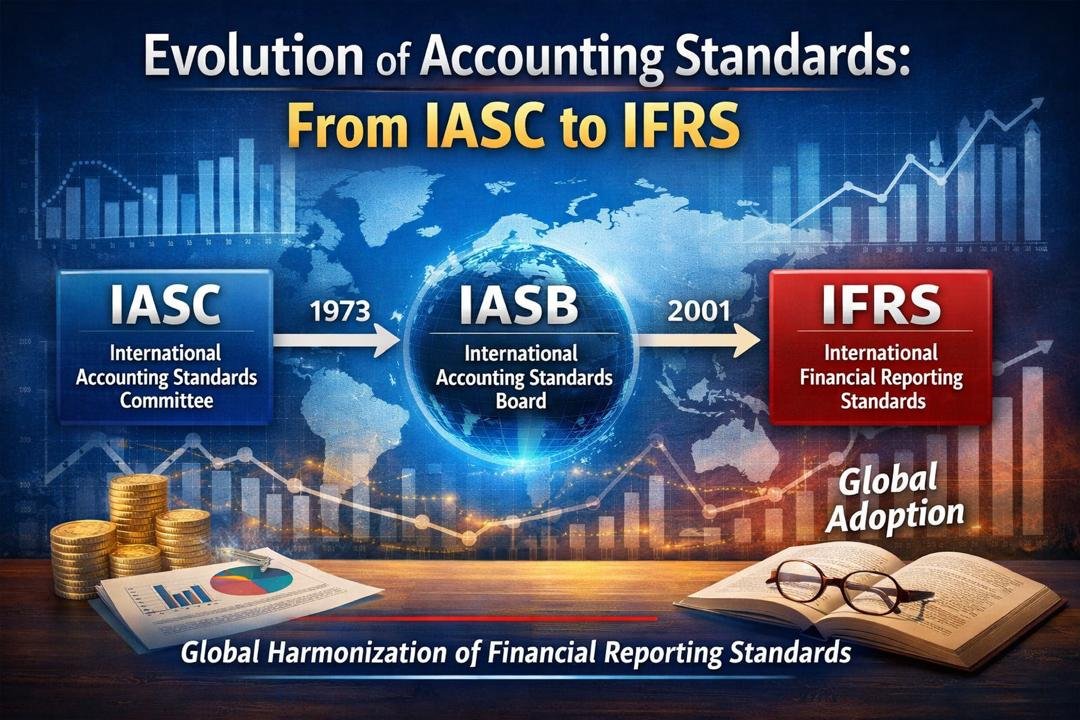

The international accounting standards did not just develop in a flash. Rather it has undergone a number of institutional and regulatory phases, such as the formation of the International Accounting Standards Committee (IASC) in 1973 and the formation of the International Accounting Standards Board (IASB) in 2001 and the adoption of International Financial Reporting Standards (IFRS). These advances were followed by national regulatory agencies that control the use of these standards in the various jurisdictions.

Nigeria and other countries have had a significant part to play in this process by implementing the IFRS and setting up regulatory bodies such as the Financial Reporting Council of Nigeria (FRCN) to oversee the financial reporting practices. The adoption of IFRS by Nigeria as a substitution of the local accounting standards can be seen as a great move towards harmonizing with international best practices and enhancing the quality of information presented in financial statements.

This paper focuses on the history of Evolution of Accounting Standards from IASC to IFRS and institutional change of IASC to IASB, adoption of the IFRS, and how the national regulatory bodies (especially in Nigeria) have led the way in adopting and applying these standards.

The Need for International Accounting Regulations

Prior to the establishment of global accounting standards, national Generally Accepted Accounting Principles (GAAP) were the major relied sources of countries. These domestic standards were aimed at addressing the regulatory, economic and cultural requirements of local nations. Nevertheless, with the growth in international trade and cross-border investments, the differences between national accounting systems have posed a number of issues.

To start with, multinational companies have experienced challenges in the preparation of financial statements that adhered to various national requirements. Second, investors were not able to easily compare financial reports of companies that had different jurisdictions. Third, regulators found it difficult to make the world financial markets transparent and accountable.

These issues brought out the Evolution of Accounting Standards from IASC to IFRS , which would help in aligning accounting practices among different countries and also help in the provision of consistency in financial reporting. The establishments of such regulation aids in making sure that the financial statements that are stated in various jurisdictions are comprehensible and that they can be compared by the user across the globe.

Formation of International Accounting Standards Committee (IASC)

After the initial move of global accounting standardization in 1973 through the formation of International Accounting Standards Committee (IASC), it was the first step in as far as global accounting standards were concerned. Professional accounting bodies of a number of countries such as the United States, United Kingdom, Canada, Germany, France, Australia, Japan, and the Netherlands formed the committee.

The primary aim of the IASC was to come up with accounting standards that were acceptable on a global basis. This committee tried to ensure that financial reporting practices varied less between different countries by developing common accounting principles.

Objectives of the IASC

The IASC had the following key objectives:

- Establishing and issuing accounting standards which might be employed across the globe.

- Encouraging the harmonization of accounting policies as well as financial reporting.

- Promoting the implementation of these norms by the national regulatory bodies.

In order to fulfill these objectives, the IASC started issuing a set of accounting standards called International Accounting Standards (IAS). These standards were used to guide the creation and presentation of financial reports and to deal with some accounting challenges like value of inventory, depreciation and recognition of revenue.

With time, the IASC was able to gain a lot of recognition in the world. Today, the use of international accounting standards is increasing as over 150 accounting bodies used the standards by the year 2000 and this was in over 100 countries.

Although such success was achieved, the IASC encountered various criticisms. It was perceived by many stakeholders that its structure was not independent and that the level of flexibility of its standards laid too much room to multiple accounting treatments. Such issues ultimately resulted in significant changes being made on the international accounting standard-setting process.

Transformation from IASC to the International Accounting Standards Board (IASB)

It was in April 2001 that the IASC was restructured significantly leading to the formation of the International Accounting Standards Board (IASB). This revolution was a new dawn in the development of international accounting standards.

The restructure formed a new organizational structure meant to enhance independence, transparency and effectiveness in the process of setting standards. The IASB has the IFRS Foundation that governs it, funds it, and provides it with strategic direction.

Key Features of the IASB

The IASB came up with a number of improvements over the predecessor:

1. Independent standard-setting

The IASB members are not chosen on the basis of national representation: the individuals are chosen on the basis of professional competence and this increases their independence in the decision-making process.

2. Global participation

The board encompasses people who have expertise in various countries and professions associated with financial reporting because it is global.

3. Rigorous due process

IASB has an elaborate consultation process comprising of exposure drafts, public comments, and stakeholder participation prior to the publication of new standards.

4. Focus on high quality standards

IASB expects to establish accounting standards that would facilitate transparency, accountability and efficiency in the financial markets.

With the IASB superseding the IASC, all the stipulated International Accounting Standards (IAS) were to be valid. Nevertheless, new standards were put forth by the IASB and were referred to as International Financial Reporting Standards (IFRS).

Globalization of International Financial Reporting Standards (IFRS)

The International Financial Reporting Standards are a system of internationally recognized accounting principles that have been created to promote the comparability and reliability of the financial reports. IFRS is principally based standards that do not give a comprehensive set of rules but general guidelines.

Objectives of IFRS

The most important goals of IFRS are:

- The provision of one set of global high-quality accounting standards.

- Improving financial reporting.

- Enhancing international financial statement comparability.

- Favoring effectiveness in world capital markets.

The accounting issues that are covered by the IFRS are quite varied in the sense that they cover financial instruments, recognition of revenue, lease, and consolidation of financial statements.

Global Adoption of IFRS

IFRS has gained wide usage in the world ever since the early 2000s. Numerous countries have either completely adopted IFRS or internally aligned their national standards to the IFRS principles. The European Union, as an example, required listed companies to use the IFRS since 2005, which has greatly boosted the adoption of the standards globally.

The IFRS are now applied in over 140 jurisdictions across the world, thus making it one of the most acceptable accounting systems in world economy.

The Role of National Regulatory Bodies

Although the international standards are an international basis of reporting financial information, they are mostly applied through the national regulatory bodies. These regulators make sure that businesses adhere to accounting practices and that the financial reporting systems are free of fraud.

The national regulatory bodies have a number of functions:

- Imposition of accounting standards and financial reporting requirements.

- Monitoring compliance by audit committees and companies.

- Offering accounting policy advice.

- Fostering transparency and confidence of investors in the financial markets.

The overriding institution in charge of the reporting of the financial reporting in Nigeria is the Financial Reporting Council of Nigeria (FRCN).

Financial Reporting Council of Nigeria (FRCN)

The Financial Reporting Council of Nigeria (FRCN) is the regulator, which has the mandate to set and enforce accounting, auditing and corporate governance standards in Nigeria.

Establishment of the FRCN

The formation of the FRCN was as a result of the passage of the Financial Reporting Council of Nigeria Act in 2010. This law superseded the Nigerian Accounting Standards Board (NASB), which was using local accounting standards, called Statements of Accounting Standards (SAS).

The establishment of the FRCN belongs to a wider initiative of Nigeria to harmonize its financial reporting system with that of the international best practices.

Functions of the FRCN

FRCN has significant roles, which consist of:

- Formulation and implementation of accounting and financial reporting standards.

- Ensuring adherence to the IFRS and other regulations.

- Enhancing good financial reporting and corporate governance.

- Concurring that international accounting standards should be implemented in Nigeria.

Through such functions, the FRCN engages in the development of the financial reporting infrastructure of Nigeria.

Nigeria’s Transition from IAS to IFRS

In 2010, Nigeria changed its accounting system to IFRS as the national accounting framework after it was sanctioned by the Federal Executive Council.

The implementation was done by use of the phased transition plan to make the migration between local standards and IFRS a smooth process.

Phased adoption of IFRS in Nigeria

Its usage was done in three stages:

- Companies and major public interest entities that are publicly traded: Obliged to switch to the use of IFRS starting in January 2012.

- Other third party interest organizations: The need to implement IFRS beginning in January 2013.

- Small and medium-sized companies (SMEs): Mandated to implement IFRS to SMEs by January 2014.

This gradual process provided organizations with ample time to re-align their accounting systems, staff train and re-align financial reporting procedures.

The advantages of IFRS Adoption in Nigeria

The implementation of the IFRS has had a number of great advantages to the financial reporting landscape in Nigeria.

1. Improved Transparency

According to IFRS, the financial statements have to include very specific disclosures that would allow the stakeholders to have a better understanding of the financial situation of the firms and their performance.

2. Enhanced Comparability

This has enabled companies in Nigeria to prepare financial statements which are comparable with those of companies in other countries enabling cross-border investment.

3. Foreign Investment is increased

International standards of accounting are also used to ensure that foreign investors are drawn because it makes financial reports more credible.

4. Integration into Global Capital Markets

The adoption of IFRS would help the companies in Nigeria to engage in the global financial markets more efficiently by fulfilling international reporting standards.

Challenges in the Implementation of IFRS

The change of IFRS has also been associated with a number of challenges even though it has a number of advantages.

- Training and Building Capacity: The intricacies of IFRS necessitated a lot of training of many accountants and auditors.

- Cost of Transition: Firms were spending a lot of money on updating accounting systems, training personnel and reorganizing the financial reporting procedures.

- Regulatory Adjustments: Regulators and government bodies had to change the current policies and legislation to keep up with the IFRS requirements.

However, this has been slowly overcome by unremitting professional development and regulatory reforms.

The Future of International Accounting Standards

The trend in international accounting standards is expected to evolve as international financial markets are becoming more and more complicated. The IASB also continuously revises IFRS to respond to the new accounting challenges and enhance the quality of financial reporting.

Recently, the International Sustainability Standards Board (ISSB) was created that is concerned with the financial reporting on sustainability-related issues. The program demonstrates the increased relevance of environmental, social, and governance (ESG) aspects of financial reporting.

Countries such as Nigeria are also on the front line of the same developments and this is an indication that they are interested in keeping the standards of financial reporting high.

Conclusion

One of the most remarkable changes in the current financial reporting is the Evolution of Accounting Standards from IASC to IFRS. Since the formation of International Accounting Standards Committee in 1973 the international accounting community has strived to develop a single system of financial reporting.

The institutionalization of the international standard setting process by the change of the IASC to the International Accounting Standards Board in 2001 was an important step towards enhancing the institutional process of setting global standards. International Financial Reporting Standards also contributed to the increased comparability, transparency, and credibility of the financial statements across the borders.

The national regulatory bodies like Financial Reporting council of Nigeria have a very important role to play in the implementation of these standards and also in the enforcement of the standards in its jurisdictions. The staged switching of IFRS in Nigeria between the year 2012 and 2014 is a sign of the intentionality of the country to be in line with international accounting practices.

With the trend of globalization that has transformed the financial markets, the role of international accounting regulation will continue to rise. Through harmonization of standards and enhanced regulation, IFRS and its supporting institutions help to enhance stability, transparency and efficiency of the international financial system.

Get more well researched information about the Evolution of Accounting Standards from IASC to IFRS here.