Introduction

Management is a process that is well organized to ensure that organizations accomplish their goals in an efficient and effective manner. Out of classical functions of management (planning, organizing, staffing, directing and controlling), controlling as a management function has a peculiar vital role. Although, planning defines the goals and focuses on the employees to achieve them, the controlling is necessary to make sure that the real performance is in accordance to the established goals. The deviations, inefficiencies, or unexpected challenges can lead to the failure of the well-designed plans without any working controlling function.

In the modern business world that is very competitive and dynamic, organizations should always keep an eye on their operations, assess performance, and make corrective measures whenever needed. This renders controlling not only a supporting role, but a pillar in the performance management. Timely feedback to the managers, early detection of problems, and optimal utilization of resources are some of the advantages of the controlling role. Finally, it provides a linkage between planning and execution and makes sure that the organizational plans are translated into quantifiable outcomes.

This paper discusses the controlling as a management activity and its contribution to the performance management. It gives the process of control, performance standards, and methods of measurement and alternative corrective actions and shows how effective control can help organizations keep pace and attain their goals efficiently.

Controlling Function of Management

The controlling role of management is the methodical way through which managers will make sure that organizational activities are performed as planned. It entails standard setting, actual performance measurement, standards comparison and corrective measures undertaken in cases of deviation.

The classical management theory defines that controlling is a progressive and ongoing activity. Instead of just pointing out the errors after they have taken place, successful control predicts likely variances and helps to ensure that they are not turned into major issues. This dynamic character makes management a very critical component of organizational achievement.

Overall, the question that is addressed by controlling is: Are we doing what we intended to do? In case the answer is no, controlling gives the framework of determining why and what should be done to rectify the situation.

To discuss this idea, refer to this elaboration of the controlling role of management, which stresses its significance in the guarantee of effectiveness and accountability of an organization.

Controlling in Performance Management

The performance management is aimed at managing performance of individuals and the organization in accordance with strategic goals. The role of controlling in such a process is crucial in that employees, departments and systems work within expectations set.

Controlling allows managers to:

- Keep track of the employee performance in comparison with targets.

- Assess the departmental efficiency and productivity.

- Determine areas of performance gaps and their reasons.

- Enforce accountability and responsibility.

- Encourage ongoing improvement programs.

Through the association of performance outcomes with organizational objectives, controlling will ensure that effort is channeled to activities that add value. It also helps in transparency and fairness as it does not give the subjective judgment but relies on the objective standards and measurable results.

In addition, controlling as a management function is essential in motivation as it gives feedback to the employees on their performance. Employees can stay engaged and committed when they know the contribution of their work to organizational success and get feedback in a timely manner.

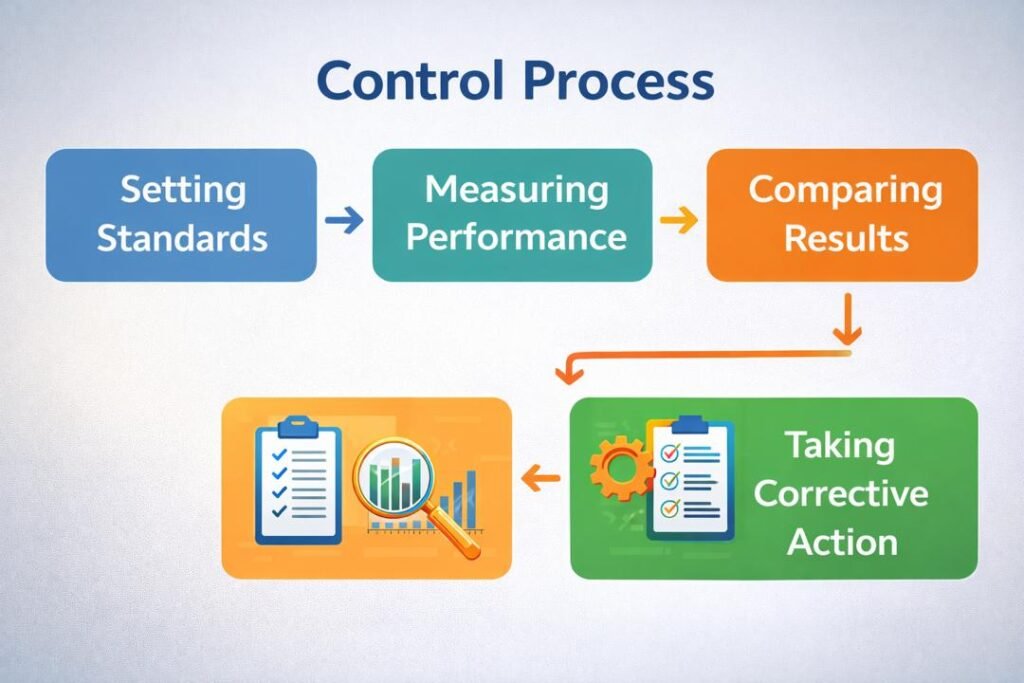

The Control Process Management

The control process refers to a logical chain of actions that managers resort to in order to make their control effective. It is usually divided into four steps:

Setting up Performance Standards

Performance standards refer to standards that are used in comparison with performance. They are standards based on organizational goal and plans and used as a reference point to evaluate them.

Promising performance standards must be:

- Specific and unambiguous – simple to comprehend and explain.

- Measurable – in a quantitative or qualitative form.

- Achievable – realistic and achievable.

- Relevant – according to organizational goals.

- Time-bound – linked to a certain period of time.

Some of the examples of performance standards are sales goals, production levels, budgetary costs, quality, and customer satisfaction scores.

In the absence of an effective set of standards, management control would be useless since managers do not have a point to compare or evaluate.

Actual Performance Measurement

After the process of setting standards, the next thing is to gauge actual performance. This is the gathering of information on the processes and performance to identify the performance of tasks.

Measurement may occur in a number of different ways, including:

- Monetary statements and reports.

- Records and statistics of operations.

- Performance appraisals

- Feedback and surveys by customers.

- Inspections and observation.

The measurement must be precise and timely and consistent. Slow or incorrect data eventually results in making bad decisions and unproductive corrective measures.

Technology has advanced, and this has immensely improved performance measurement. The modern day organizations are using management information systems (MIS), dashboards and data analytics tools to monitor the performance in real time to enable them respond faster to deviations.

Comparison of Performance and Standards

The third control process step is the comparison of the actual performance with the set standards. This comparison assists the managers to recognize deviations- differences between anticipated and actual outcomes.

Deviations can be:

- Positive, performance is above expectations.

- Where performance is below the standard, negative.

Deviations do not necessarily need to be corrected. Minor or allowable deviations could be accepted particularly when the cost of correcting them outweighs the advantages. Nevertheless, great deviations are indicators of managerial interventions.

This step proves to be very important as it will convert raw performance data information into data that is useful to make decisions.

Taking Corrective Action

The last and most important control process is the corrective action. It entails correcting the reasons behind deviations and making sure that the performance in future is in line with the standards.

The corrective measures may involve:

- Revising the work methods or processes.

- Giving extra training or supervision.

- Reallocating resources

- Modifying the performance standards when they are unrealistic.

- Taking disciplinary action where required.

The action taken to correct the situation must center on the cause of the issue and not on the symptoms. Indicatively, low productivity caused by lack of proper training will not be solved by punishment but instead, skill development is necessary.

Corrective action is not only effective but also helps in curbing the recurrence of current problems that would lead to long-term organizational improvement.

Controlling Performance Standards

Controlling as a management function is based on performance standards. They change organizational goals into individual and departmental expectations that are specific and measurable.

Performance Standards types

- Financial Standards: These are profitability, revenue goals, the return on investment (ROI) and cost constraints. The financial standards have become common as they present definite numerical standards.

- Operational Standards: These involve quality, efficiency, productivity and timeliness. Some of them are units per hour, defects, and turnaround delivery times.

- Behavioral Standards: These emphasize behavior of employees, teamwork, leadership and corporate values. Performance appraisals and feedback systems are usually used to evaluate them.

- Strategic Standards: These are measures of improvement of long-term objectives, including market share, level of innovation, or brand image.

The integration of various forms of standards would enable organizations to have a balanced strategy towards performance management.

The Techniques of Measurement in Controlling

The assessments of actual performance are measured by tools called the measurement techniques. The type of technique used is dependent on the type of activity under control.

Typical Measuring Methods

- Budgetary Control: Comparative financial performance vs. budget performance.

- Standard Costing: Cost variance measurement in manufacture.

- Performance Appraisals: The process of comparing the performance of employees with a set standard.

- Statistical Reports: This is an analysis of trends using charts and graphs.

- Management by Objectives (MBO): The performance that is measured through goal achievement.

- Key Performance Indicators (KPIs): Following the important success factors.

Proper measurement methods are those methods that yield credible data that can be used to make well-informed decisions and corrective measures in a timely manner.

Remedial Measures and Continuous Improvement

Corrective action is not only focused on the fixing of problems but also on creating a continuous improvement. Companies that interpret controlling as a learning organization can be adapted and developed.

One can categorize corrective action into:

- Corrective action is taken immediately and they deal with the deviations at present.

- Simple corrective measures, where systems, processes or policies are adjusted to avoid future deviations.

When organizations incorporate the corrective action in performance management systems, then they are likely to establish a culture of accountability, learning and improvement.

Significance of Controlling in Achieving Objectives of the Organization

Controlling as a management function role is vital because of the following reasons:

- It guarantees the effective utilization of resources.

- It helps in accomplishment of goals and alignment of strategy.

- It improves accountability and transparency.

- It aids in the coordination of departments.

- It facilitates the identification and resolution of problems in time.

Organizations that lack proper control are exposed to inefficiency, wastage, and lack of attainment of their goals.

Conclusion

One of the management functions which cannot be ignored in making sure that organizational plans are realized into actual outcomes is controlling. Managers can keep the organizations on track and remain productive by setting standards of performance, measuring actual performance, comparison and correction of results against expectations.

Control in the performance management context offers the framework and rigidity required to monitor the alignment of personal and organizational endeavors with strategic focus. It makes planning a process of action and vision a reality.

Finally, organizations with effective controlling systems are in a better position to ride uncertainty, boost their performance and ensure its sustainable success in the dynamic world of business.

Get more well researched information about control as a management function here.