For large physician groups, choosing the right malpractice insurance structure can be the difference between stable long-term protection and costly coverage gaps. While individual doctors often make decisions based on affordability or simplicity, group practices must balance risk management, cash flow, and compliance across multiple specialties and locations.

At the heart of this decision lies a critical choice between claims-made and occurrence malpractice insurance policies. Both types offer important protections, but their coverage timelines, costs, and long-term implications differ significantly.

Understanding how each works is key to designing a sustainable insurance strategy for your organization. For a more detailed breakdown of policy differences, you can explore

Claims Made vs Occurrence Malpractice Insurance to understand in detail how each policy type impacts coverage, cost, and long-term protection.

What Is a Claims-Made Policy?

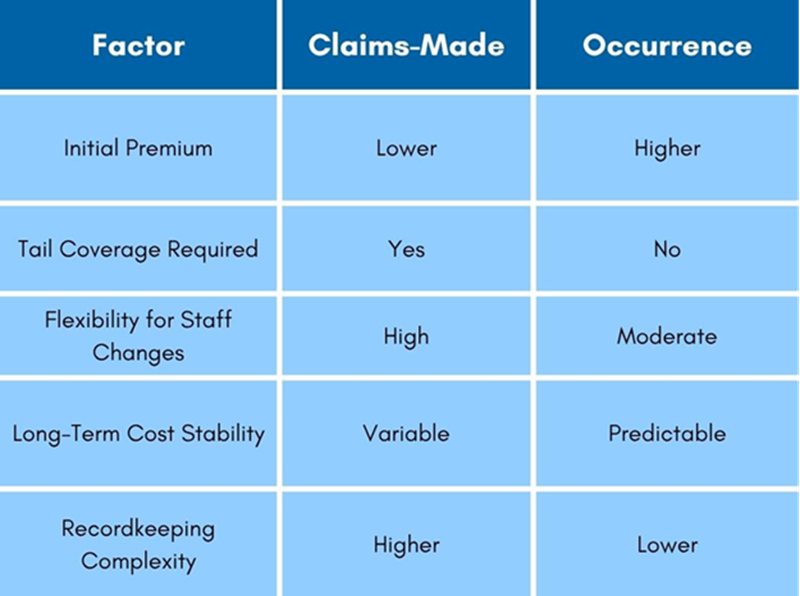

A claims-made policy covers malpractice incidents only if the claim is filed and reported while the policy is active. Once the policy ends or is canceled, coverage stops unless the group purchases an extended reporting endorsement, also known as tail coverage.

For example, if a claim is filed in 2026 for a treatment performed in 2024, the physician or group must still have the same policy active in 2026 to be covered. If the policy were terminated without a tail, there would be no protection for that event.

Why Large Groups Choose Claims-Made Coverage

- Lower initial premiums: These policies usually cost less in the first few years and gradually increase as exposure grows.

- Ease of transfer: Groups that frequently add or release physicians can manage policies more efficiently with flexible retroactive dates.

- Customizable risk management: Claims-made coverage makes it easier to track and evaluate ongoing liability trends.

Key Drawback

When physicians retire or leave the practice, the group must ensure tail coverage is purchased to protect against future claims. This one-time cost can range from 150% to 250% of the expiring premium, making it a significant financial consideration for group administrators.

What Is an Occurrence Policy?

An occurrence policy covers any incident that happens during the policy period, regardless of when the claim is filed. Even if a lawsuit surfaces years after a physician leaves the group, the insurer will still provide defense and indemnity, provided the incident occurred while the policy was active.

Why Occurrence Policies Appeal to Larger Practices

- Permanent protection: There is no need to buy tail coverage when a doctor leaves or retires.

- Simplified administration: Each policy year stands alone, eliminating concerns about retroactive dates.

- Predictable budgeting: Premiums are higher initially but do not escalate over time as they do with claims-made coverage.

Key Drawback

Occurrence policies tend to cost 20 to 35 percent more upfront. For large groups managing dozens of physicians, the higher premiums can significantly impact annual budgets, especially in high-risk specialties like surgery or obstetrics.

Cost Comparison and Long-Term Impact

The initial savings of a claims-made policy may seem appealing, but the total long-term cost, including tail coverage, can often match or exceed an occurrence policy. For large groups, the decision often depends on turnover rates, specialty mix, and financial planning priorities.

Large physician groups with steady staffing and long-term contracts may prefer occurrence coverage for its simplicity, while organizations with frequent transitions or younger physicians may benefit from the flexibility of claims-made coverage paired with negotiated tail options.

To gain deeper insight into how malpractice costs and legal processes work together, you can read Medical Malpractice Explained: Your Rights and Legal Options, which breaks down the connection between policy structure, claim handling, and a physician’s legal protection.

Managing Risk Across Large Physician Groups

For group administrators, the insurance decision is not just about premiums; it is about risk continuity and reputation management. Some practical steps include:

- Standardizing policy types: Ensuring all physicians are on compatible coverage helps avoid gaps.

- Negotiating tail terms upfront: Many insurers offer discounted tail coverage when purchased at the start of the policy.

- Annual audits: Review each provider’s retroactive date, policy limits, and specialty risk to ensure ongoing protection.

- Educating staff: Physicians should understand how claims timing impacts coverage and their personal liability.

For additional insight into how tail coverage strengthens long-term protection,

See Key Benefits of Tail Coverage Insurance for Physicians, a useful resource for groups planning future transitions or retirements.

Building a Smarter Coverage Strategy

There is no universal answer when choosing between claims-made and occurrence coverage. A large hospital-affiliated group may favor occurrence policies to simplify compliance, while a private multispecialty network might leverage claims-made coverage for cash-flow efficiency.

The key is to evaluate both short- and long-term implications, not just annual cost. Partnering with experienced insurance consultants ensures that coverage decisions align with your organization’s growth strategy, physician turnover, and risk tolerance.

A thoughtful, well-planned insurance structure allows large physician groups to protect what truly matters: their people, their patients, and their reputation.