Introduction

Financial information takes the center stage in the planning, controlling and decision making in any organization be it a small business, a non-profit organization or a multinational corporation. Bookkeeping vs Accounting is a fundamental topic in financial management, without proper financial information, managers are not able to define profitability, investors are not able to gauge performance, and governments are not able to gauge compliance with regulations. Bookkeeping and accounting are two important terms which make this financial system functional.

These terms are used interchangeably however, they are different yet closely related processes in the financial management system. Most of the time, various individuals confuse bookkeeping with accounting or assume that one is a more complex form of the other. The resulting confusion is blurred professional roles and responsibilities and the general arrangement of financial management.

This article defines accurately what bookkeeping and accounting is, their similarities and differences, and how bookkeeping is the backbone of accounting operations. These two functions will be discussed as to how they are used in conjunction to assure financial accuracy, aid business decisions and enhance accountability in organizations.

Understanding Bookkeeping

Definition of Bookkeeping

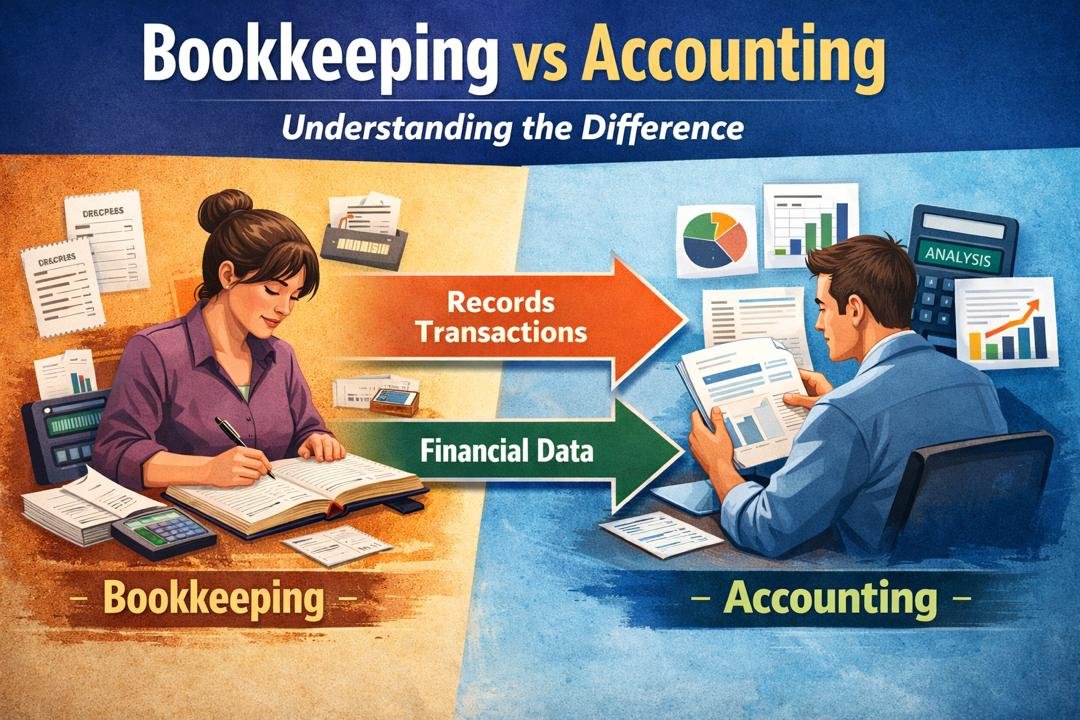

Bookkeeping is the organized procedure of determining, documenting, and classifying financial deals of a business or an organization. It is concerned with recording everyday financial transactions, including: sales, purchases, payments, and receipts, in an organized and uniformed way.

In a simplistic manner, bookkeeping provides the answer to the question, what financial dealing has been done?

Data entry and documentation are the major concern of bookkeeping. All the financial transactions should be documented correctly and in the chronological order such that it can be utilized in the future to analyze and report.

Bookkeeping: Main Functions

Bookkeeping has the following major functions:

- Recording Transactions: In proper journals or accounting software, all the financial transactions are registered. These are cash dealings, credit purchases, costs, payroll and purchase of assets.

- Classifying Transactions: The transactions are classified into some relevant accounts like cash, accounts receivable, inventory, revenue and expenses.

- Books of Accounts Maintenance: Some of the major records that bookkeepers keep include the cash book, sales journal, purchase journal and the general ledger.

- Assuring Accuracy and Completeness: Every transaction has to be justified by documents such as invoices, receipts, and payment vouchers.

- Balancing Accounts: Bookkeepers will periodically verify that the amount of debits matches the amount of credits so that the records are mathematically accurate.

Nature of Bookkeeping

Accounting is mostly mechanical and procedural. It is not very interpretive or judgmental. Rather than that, it involves attention to details, regularity and compliance with set rules like the double entry system.

The main objective of the bookkeeping is to develop a trusted financial database that will be used by the accountants in future to analyze and report.

Understanding Accounting

Definition of Accounting

Generally, accounting is the general procedure of identifying, gauging, categorizing, summarizing, interpreting, and conveying financial data to the user to aid in choice making.

Whereas bookkeeping records a raw financial data, accounting converts the raw financial data into meaningful information. That is, accounting provides the answer to the following question, What is the implication of these financial records to the organization?

Accounting is more than registering transactions. It entails the analysis of financial information, financial statements and interpretation of financial results to the management, investors, creditors and other stakeholders.

Key Functions of Accounting

The key roles that accountings play are:

- Classification: Organizing financial data into any significant categories like assets, liabilities, equity, income, and expenses.

- Summarization: The ability to compress high amounts of transaction data into financial statements including the income statement, balance sheet, and cash flow statement.

- Claims Analysis and Interpretation: Analysis of financial performance to determine trends, profitability, liquidity and solvency.

- Reporting: Exporting financial information to the internal and external users as financial reports.

- Decision Support: The provision of appropriate financial intelligence that assists managers in the planning, controlling, as well as making strategic decisions.

Nature of Accounting

Accounting is technical and analytical. It involves judgment of a professional, insight of accounting standards and interpretation of financial data in context.

The accounting process, contrary to the bookkeeping process, entails assessment, approximating and analysis.

Comparisons of Bookkeeping vs Accounting

There are also some significant similarities between bookkeeping and accounting though the two are very different. All these similarities bring about the reasons why they are usually mixed up and yet they cannot be separated in practice.

- They both deal with Financial Data

Bookkeeping and Accounting work with the financial information. They worry about documenting, arranging and processing financial transactions concerning business operations.

- Both are Goal-oriented towards Financial Accuracy.

The two roles focus on accuracy. Mistakes during bookkeeping result to wrong accounting report and bad accounting interpretation may give a wrong meaning to correct book keeping records.

- Both Share the same Accounting System.

Their main similarity is that both of them are based on the basic principles of the double-entry system when all transactions involve at least two accounts.

- They both support decision-making.

Even though accounting has a more direct influence on it, bookkeeping assists in decision-making indirectly since it is the source of raw information, which is analyzed to facilitate financial analysis.

- Both are a part of Financial Management Process.

The financial information system of any organization is constituted by bookkeeping and accounting. It is impossible to work without the other.

Major Differences between Bookkeeping vs Accounting

Although closely interrelated, bookkeeping and accounting vary in their scope, role, skills, and purpose.

Difference in Scope

Bookkeeping:

- Narrow in scope

- Only able to record and classify transactions.

Accounting:

- Broad in scope

- Includes reporting, interpretation and analysis.

Bookkeeping is concerned with the manner in which transactions are captured and accounting is concerned with the sense of such transactions.

Difference in Function

Bookkeeping:

- Operational function

- Fixed on record keeping and data entry.

Accounting:

- Planning and critical thinking capability.

- Concerned with financial analysis and decision support.

Diversity in Skill Requirement

Bookkeeping:

- Needs basic understanding of accounting.

- Emphasizes accuracy, order and detail.

Accounting:

- Needs advanced professional training.

- Focuses on analytical skills, judgment and interpretation.

Difference in Output

Bookkeeping Output:

- Journals

- Ledgers

- Trial balances

Accounting Output:

- Income statement

- Balance sheet

- Cash flow statement

- Financial analysis reports

Difference in Decision-Making Impact

Bookkeeping:

- Indirect impact

- Provides raw financial data

Accounting:

- Direct impact

- Guides business choices, investments and policy making.

Bookkeeping as the Operational Foundation of Accounting

The correlation between accounting and bookkeeping is hierarchical. First, there is bookkeeping, then there is accounting. It is due to this reason that bookkeeping is termed as the operational base of accounting.

And accounting cannot exist without bookkeeping. The profession of accountants wholly relies on the records of bookkeeping in order to carry out their functions. Without proper recording of transactions, the financial statements will be erroneous and thus the decisions made on it will be erroneous.

How Bookkeeping Supports Accounting

- Provides Reliable Data: It is through bookkeeping that financial data is created that the accountants analyze.

- Ensures Completeness: Every transaction should be documented prior to its summing up or interpretation.

- Minimizes Accounting mistakes: Having proper bookkeeping reduces the chances of misstatement in the financial reports

- Promotes Financial Reporting: Bookkeeping is a process that systematizes the information into ledgers, which the accountants utilize to prepare financial statements.

In this respect, bookkeeping is the engine room whereas, accounting is the control room of the financial system. One creates the raw materials, the other works on these creating actionable insights.

Eliminating Factual Fallacies

Misconception 1: There is a difference between bookkeeping and Accounting.

This is the common misconception. The two are connected, whereas bookkeeping is concerned with the recording, and accounting is concerned with reporting and interpretation.

Misconception 2: Bookkeepers and Accountants perform the same role.

Bookkeepers deal with daily transactions. Financial information is processed by accountants who give strategic guidance. Their functions are not the same, they are complementary to each other.

Misconception 3: Accounting is More Significant than Bookkeeping.

They are dependent on each other since neither is more important. Without bookkeeping accounting cannot work and without accounting bookkeeping does not add up to much.

Misconception 4: Technology has eliminated book-keeping.

Despite the fact that accounting software automates most tasks, there is still bookkeeping. The use of technology has transformed the manner in which bookkeeping is carried out, rather than its significance.

Interrelationship between Bookkeeping vs Accounting

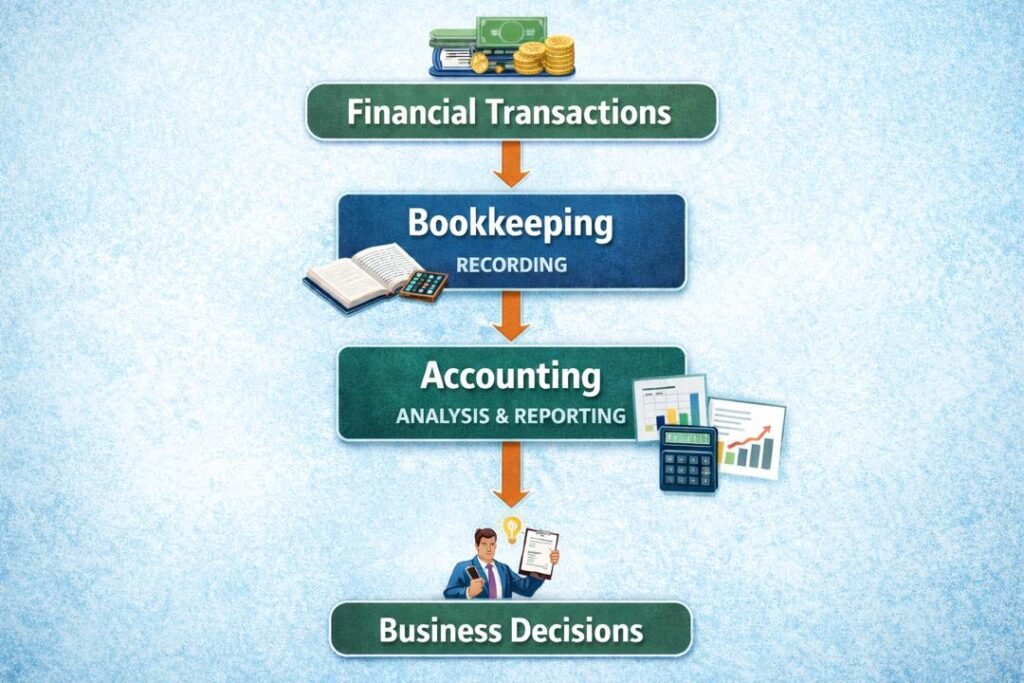

The correlation between bookkeeping and accounting can be described in the form of a process flow:

- Financial transfer takes place.

- The transactions are recorded in bookkeeping.

- It summarizes and classifies the information under accounting.

- Preparation of financial statements.

- Reports are used by the management to make decisions.

This flow indicates that bookkeeping and accounting are not dissimilar systems but are interlinked processes in the financial information cycle.

Importance of Bookkeeping and Accounting in Organizations

For Small Businesses:

- Accounting assists in monitoring cash flow and expenditures.

- Accounting assists in determining profitability and growth.

For Large Organizations:

- Regulatory compliance is guaranteed through bookkeeping.

- Accounting helps in strategic planning and appraisal.

For Government and Non-Profit Organizations:

- Transparency is achieved through bookkeeping.

- Accounting provides responsibility and sound utilization of funds.

Conclusion

Two pillars of financial management include bookkeeping and accounting. Although bookkeeping is related to the systematic control of financial transactions, accounting is related to the classification, summarization, interpretation and reporting of financial data.

The similarity between them is that they are interested in financial information and precision whereas the differences can be found in the terms of scope, level of analysis and influence on decision making. Above all, bookkeeping represents the functional basis of accounting through which the necessary data is converted into valuable financial conclusions of accounting.

The knowledge of the difference and interdependence between the two functions dispels most of the misconceptions and underscores the complementary nature of the functions. Bookkeeping and accounting are effective in managing the financial integrity of the organizations, in providing informed decisions, and long-term sustainability.

Get more well researched information about Bookkeeping vs. Accounting here.