Introduction

The accounting in contemporary organizations is much more than the mechanical aspects of debits and credits. It is a systematized information system that gathers economic information, data, and processes on standardized criteria, stores the received information in a secure environment and delivers it to different users to make informed decisions. Accounting as an information system has been the foundation of the organizational intelligence of small enterprises to multinational corporations to translate raw financial transactions into reports that can be understood and put into practice.

In order to realize the strategic value of accounting, it is important to know that the system is systemic. Instead of considering accounting as bookkeeping, it has to be realized as a dynamic, interrelated system that encompasses people, procedures, technology and regulatory frameworks. Such a systemic base makes sure that the flow of financial information between the operational activities and the managerial dashboards as well as the outside financial statements works in an uninterrupted manner.

The Structured Information System of Accounting

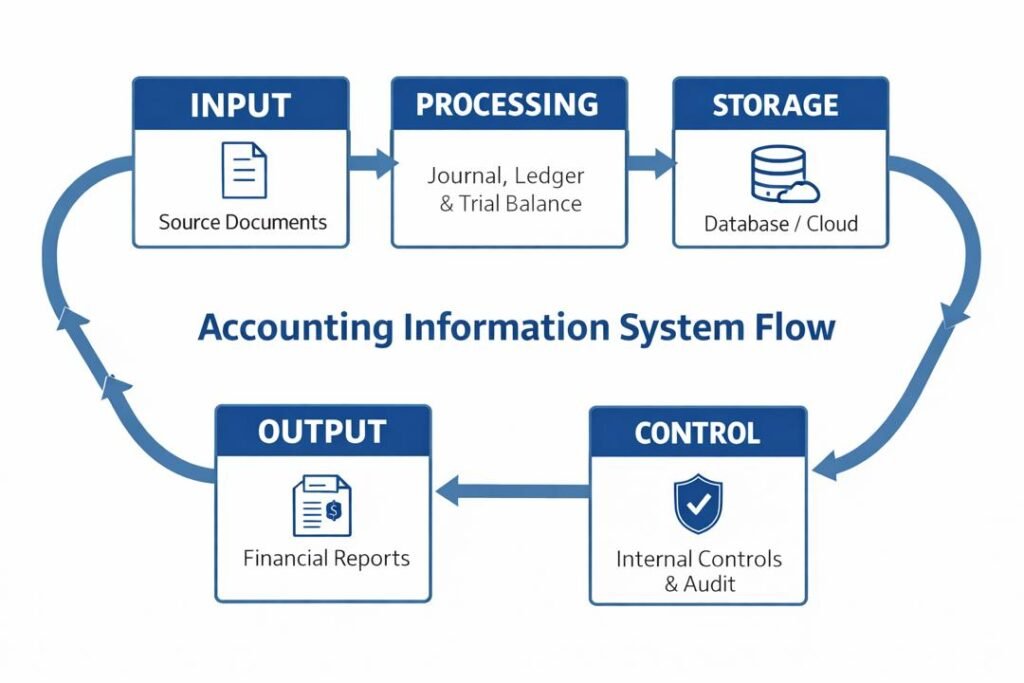

The majority of definitions of an information system tend to be a well-coordinated arrangement of parts that gather, process, store, and distribute information to aid in decision-making, coordination, and control. Accounting perfectly fits in this definition. It is a systemized mechanism that is set to record financial information, transform it into structured information and present it to the stakeholders in a timely and trustworthy way.

There are a few components within the accounting information system (AIS) which relate to each other:

- The source documents and transaction records are the input mechanisms.

- Processing (classification, summarization, adjustment)

- Archives, databases, ledgers, storage systems.

- Outputs (financial reports, management reports, dashboards)

- Internal controls, audits, compliance checks, control measures.

These factors interact to provide that the financial information is true, full, and useful. It is not any one of these functions which make accounting systemic, but their interdependence with each other.

Data Collection: Capturing Economic Events

The first stage of the accounting system is the recognition and gathering of data of the economic events. All financial transactions like sales, purchases, payrolls, acquisition of assets or repayment of loans produce documentation. These reports consist of invoices, receipts, contracts, bank statements and payroll records.

This phase is very important since the output will be as good as the input. Poor records or poor data capture mechanisms undermine the whole system. Enterprise resource planning (ERP) systems are commonly applied by modern organizations to automatically capture transactions as they happen. Indicatively, in the event that a sale transpires, revenue records, inventory balances and accounts receivable are updated.

The accounting information system is thus not a self-sufficient system. It has interfaces with the sales systems, procurement modules, human resource management systems and production operations. This integration guarantees the real time data flow and efficiency.

Data Processing: Raw Transactions to Structured Data

Once data have been collected, it has to be processed. Processing means categorizing, documenting, generalizing and modifying financial transactions based on the known accounting regulations and standards like International Financial Reporting Standards or local regulations frameworks.

The double-entry system is traditional, and every transaction has the impact on at least two accounts that ensures the accounting equation:

Assets = Liabilities + Equity

Processing includes:

- Journalizing transactions

- Posting to ledger accounts

- Preparing trial balances

- Making adjusting entries

- Creation of financial summaries.

In this formal process, the raw data about transactions is processed into systematic finance. It is this change that makes the difference between accounting and mere record-keeping. Bookkeeping captures data; accounting analyses, interprets and organizes data to make decisions.

Data Storage: Organizational Memory.

Accounting is also the financial memory to the organisation. Ledgers, computer databases and cloud storage systems maintain records on the past transactions and financial records that can be used in the future. Such records support audits, tax evaluation, regulatory compliance as well as strategic analysis.

The present-day accounting systems are dependent on digital databases. The software based on the clouds has a central data that can be backed up and accessed in real time. Storage mechanisms should provide:

- Data integrity

- Confidentiality

- Accessibility

- Adherence to legal retentions.

This storage facility enhances accountability and transparency. The organisations are unable to make strategic decisions devoid of historical data to compare and analyze trends.

Communication: Delivering Information to Stakeholders

Communication is the final goal of the information system of accounting. The information that is processed and stored in the system should be presented in a meaningful format to internal and external users.

Internal Users

Accounting information is used by the managers to:

- Budgeting and planning

- Cost control

- Performance evaluation

- Resource allocation

- Investment decisions

The management accounting report can also contain variance analysis, cost-volume-profit analysis, break-even analysis, and cash flow forecast. These reports are highly customized and are usually made regularly based on the requirements of the organisation.

External Users

The external stakeholders entail the investors, creditors, regulatory agencies, and tax authorities, as well as employees. They are dependent on standardized financial statements like:

- Financial Position Statement.

- Statement of Profit or Loss

- Statement of Cash Flows

- Changes in Equity Statement.

Such reports give an idea about profitability, liquidity, solvency, and efficiency. In the case of publicly traded companies, the transparency and credibility are achieved by adhering to the regulatory agencies like the Financial Reporting Council of Nigeria.

The visible product of the accounting system is therefore communication, which is based on an intricate basis of structured processes.

Integration with Operational Systems

Integration of accounting information system with operational system is one of the distinguishing attributes of accounting information system. The accounting is incorporated in the production, marketing, procurement, logistics, and human resources.

For example:

- A production system captures material usage which is used in cost accounting.

- A sales system records the revenue and receivables.

- Payroll system- a payroll system is calculated and the expense and liability accounts are updated.

- Inventory management system records the stock which affects the cost of goods sold.

The ERP systems used in the modern organisations have brought these functions together in a centralised database. This integration saves on redundancy, accuracy, and real time reporting.

This interconnection is the manifestation of the systemic nature of accounting. The alteration in a single department of operation translates to various accounting aspects, which impact the managerial decisions.

Providing support to Planning Functions

Planning entails identifying goals and the means of accomplishing them. Accounting data assists in the process of planning by budgeting, forecasting and financial modeling.

Budgeting

Budgets give a financial guide of how the company will operate in future. They are made according to past figures and forecasted trends. The basis is founded on accounting data:

- Sales budgets

- Production budgets

- Cash budgets

- Capital expenditure budgets.

Budgeting can only be speculative without proper accounts information, and unreliable.

Forecasting

Forecasting is based on historical patterns of finance as an indicator of future results. All the analysis of trends, ratio analysis and scenario modeling require the correct accounting data. These forecasts help managers predict the cash crunch periods, to analyze the growth prospects or to plan in the event of economic slump.

Therefore, accounting is a predictive instrument rather than a historical instrument.

Supporting Control Mechanisms

Control is used to make sure that organizational activities are as planned and as objectives. The accounting is essential in creating the performance measurement and internal controls in order to establish the control systems.

Internal Controls

Internal controls refer to the procedure that is put in place to protect the assets, avoid inaccuracy, and prevent fraud. They include:

- Segregation of duties

- Authorization procedures

- Reconciliations

- Audit trails

These are controls that are incorporated in the accounting system to ensure reliability.

Variance Analysis

Managers compare the actual results and the budgeted results to determine variances. Greater deviations raise an inquiry and corrective action. The accounting reports therefore give feedback loops that keep the organisations in check.

Accounting strengthens organizational stability and accountability by ensuring that planning is combined with monitoring.

Performance Evaluation and Strategic Planning

Performance evaluation is a process that entails measuring efficiency and effectiveness of meeting organizational objectives. Quantitative indicators of success include such accounting measures as return on investment (ROI), gross profit margin and earnings per share.

The strategic decisions that involve mergers, acquisitions, diversification of product or expanding to a new region needs a lot of financial analysis. Accounting data supports:

- Cost-benefit analysis

- Decisions relating to capital budgeting.

- Risk assessment

- Break-even analysis

The absence of structured financial information would translate into strategic decisions being made based on intuition and not evidence.

Compliance and Regulatory Framework

The regulatory environments in which accounting systems are conducted are those that assure standardization and comparability. Organisations are governed by international and national organisations that provide rules to be adhered to.

As an example, international organizations are obligated to international Accounting Standards Board that formulates international reporting standards. The statutory compliance in Nigeria is regulated by the Corporate Affairs Commission.

These models enhance the systemic nature of accounting through establishment of legal and ethical aspects into financial reporting. Compliance will make sure the information that is passed out externally is acceptable and comparable with other organisations.

Technology and the Evolution of Accounting Systems

The use of technology has greatly changed the accounting to a complex information system. The manual ledger systems have been substituted with electronic systems that automate the procedures of transactions and reporting.

Significant technological factors are:

- Cloud computing

- Artificial intelligence

- Data analytics

- Blockchain technology

Automation lessens the human error, improves efficiency, and improves real time reporting. Data analytics tools enable organisations to gain extra insights out of financial data, which is important in making strategic decisions.

An example is the used blockchain technology that has increased transparency and security through the generation of unchangeable records of transactions. This development proves that accounting is constantly shifting to technological innovation without losing its systemic structure.

Accounting Beyond Bookkeeping

The common misconception associated with accounting is that it is equal to bookkeeping. Where bookkeeping is concerned with recording transactions, accounting is all about analysis, interpretation, reporting, and strategic assistance.

The systemic aspect of accounting makes it unlike the normal data entry. It involves:

- Conceptual frameworks

- Regulatory compliance

- Analytical tools

- Strategic integration

- Feedback mechanisms

Financial information, as interpreted by the accounting professionals, is used to provide advice to management, investors and policymakers. They do not just record but also form organizational strategy.

The Interconnected Feedback Loop

Accounting is a feedback system in the organisation. Data is created due to operational activities. This data is processed by accounting and reports generated. These reports are reviewed by the management and strategies are changed. The new strategies affect the future operations forming a cycle.

It is a cyclical process which underscores the systemic nature of accounting. It is not a fixed role but a dynamic process which is responsive to the organizational and environmental changes.

Ethics and Reliability of information

Accounting being an information system has to be integrity upheld. Through ethical standards, financial reporting is not distorted. The codes of conduct in the field of professions underline honesty, objectivity, and transparency.

Stakeholder confidence in accounting information is generated. Proper reports are important in informing the decisions of investors regarding capital allocation. Before issuing loans, creditors consider the solvency. Taxation and policies are based on the financial information presented by governments.

Ethical violations create chaos in the system and may attract serious consequences, such as prosecution and tarnished reputation. Thus, ethics is a part of the accounting system.

Conclusion

There is no denying the fact that accounting is the foundation of organizational decision-making. It is an organized information system that gathers, processes, archives and disseminates financial information to various users. Accounting is a trusted source of strategic and tactical decisions through the process of integrating with the operational systems, support planning and control as well as adherence to regulatory standards.

By identifying accounting as a system and not book keeping, we value the importance of accounting as a strategy. It converts crude economic incidents into valuable outputs, fosters responsibility and propels organizational results.

The systemic aspects of accounting help organizations to stay informed, transparent and strategic in a more and more complex business environment. Accounting is not the administrative job in the background, but at the heart of organizational intelligence and long-term decision-making.

Get more well researched information about Accounting as an Information System here.