Introduction

In present day’s fast changing and very competitive business world companies must transform constantly, make informed decisions, and have their operations tied to long term goals. This is what planning and control in management accounting does. As opposed to financial accounting which reports past financial performance to outside parties, management accounting is internal and forward looking. It gives managers the tools and insights they need to do planning well and to control business operations.

Planning sets the direction, also Control which sees to it that the organization stays on track. To have a better picture of the dual role of management accounting it is important to look at how these functions play out in practice and what role they play in the large scale success of the organization.

Understanding Management Accounting

Management accounting is a process of identification, measurement, analysis and interpretation of both financial and non-financial info that we put before management for use in decision making. Also it is not tied to rigid reporting rules as is financial accounting which in turn makes it a very flexible field to meet the exact requirements of each organization.

Our main goal is to present relevant and current info which in turn supports internal functions of budgeting, forecasting, performance evaluation, and strategic planning. Also we have made management accounting into a tool which guides organizational behavior and improves efficiency.

Planning Concepts in Management Accounting

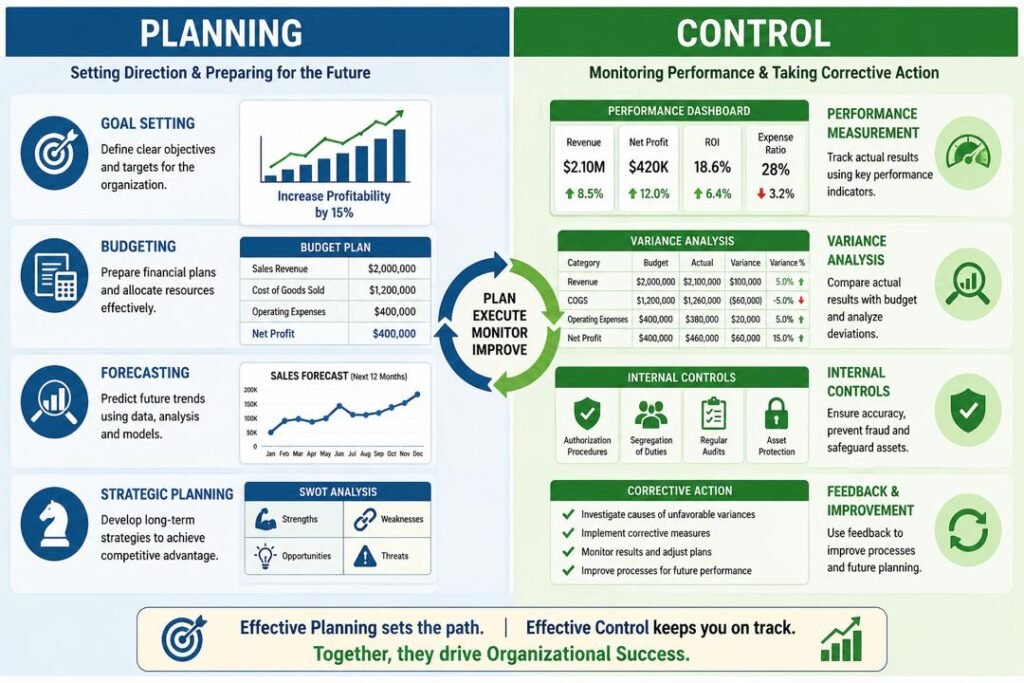

Planning is a process which sets out objectives and determines the best actions to achieve them. In management accounting planning includes forecasting future trends, allocating resources, and setting measurable goals.

Setting Organizational Goals

Planning starts with setting out clear and attainable goals. These goals may be short term or long term which in turn may include such things as increasing market share, improving profitability, or entering new markets. Management accountants supply data which is the basis for managers to put forth realistic targets which are founded in past performance and present trends.

Purchasing within our means

In the planning stage budgeting is a key tool. A budget is a financial plan which puts forth what we expect in terms of income and outgo over a given period. It acts as a road map for the organization which in turn guides which resources are used and what is done operationally.

Budgets can take various forms, including: Budgets may take the form of:

- Operating budgets

- Capital budgets

- Cash flow budgets

Each budget is for a particular purpose which in turn uses resources in the best way.

Forecasting

Forecasting is the process of projecting future financial results based on past data and market study. Management accountants which is what we are talking here use tools like trend analysis, regression models, and scenario planning to determine what future revenues, costs, and cash flows will look like.

Accurate prediction of trends which in turn enables organizations to see challenges and opportunities before they happen which is in turn a foundation for proactive decision making.

Strategic Planning Process

Strategic planning is on large scale goals and the direction of the organization as a whole. It includes analysis of internal strengths and weaknesses which we also look at external opportunities and threats (what is also known as SWOT analysis).

Management accountants play a role in strategic planning includes producing financial projections, doing cost benefit analyses, and risk assessments. Thus they base strategic decisions on sound financial information.

The Concept of Control in Management Accounting

While planning sets the direction, control sees to it that the organization stays on track. Control in this case is about performance monitoring, which is the comparison of actual results with what was planned for, and taking corrective action as required.

1. Measurement of Performance

Performance evaluation is a main element of control. We look at what the organization is doing to achieve its goals. This is done via a variety of metrics which include:.

- Revenue growth

- Profit margins

- Return on investment (ROI)

- Cost efficiency

Management which is what we of course see in the case of the large scale implementation of performance measurement systems that in turn present to us key information on issues of operational performance.

2. Variance Analysis

Variance analysis is a method which we use to compare actual results with what was budgeted. We call the difference between the two budgets, Variance.

Here are the two main types of variances:

- Favorable variance: When results outperform what was expected of them.

- Unfavorable variance: When results fall below the mark.

Through analysis of these variances managers are able to determine the causes of deviations and put in corrective action.

3. Internal Control Systems

Internal control systems and processes which protect assets, assure accuracy in financial reporting, and deter fraud. Which include:

- Authorization procedures

- Segregation of duties

- Regular audits

Management accountants also play a key role in the design and which of these controls also in the issue of compliance and efficiency.

4. Feedback Systems

Control systems use feedback for effective performance. Feedback in this process means to collect info on performance and use it to make adjustments.

For instance should a company’s spending go beyond what is in the budget management may look at what went wrong and put in place measures to bring down future costs.

The Interrelationship between Planning and Control

Planning and control do not stand alone; they are in a dynamic relationship and support each other. What we put into practice through planning also serves as a standard to which we measure performance and control’s role is to see that we live up to those plans.

1. Planning as the Base for Control.

Without a plan there is no way to which you can compare results. Planning sets the goals and what is to be achieved which in turn enables control. For example a budget which is set of expected expenditures is then used to evaluate what the actual spend was.

2. Control as a Feedback System for Planning.

Control gives out very useful feedback which in turn improves future planning. Through analysis of performance data organizations are able to identify trends, refine their assumptions and in that do better forecasting.

This continuous process of planning and control creates a dynamic which in turn improves organizational performance.

Tools for Planning and Control.

Management accounting uses a range of tools and techniques for planning and control.

1. Standard Costing

In the practice of standard costing we set out costs in advance for products or services which we then compare to actual results. This allows us to identify inefficient practices and areas for improvement.

2. Break-Even Analysis

Break at which point total revenue equals total cost is what break-even analysis does. It also helps managers out with the relationship between cost, volume and profit which in turn aids in decision making.

3. Scorecard Framework

The balanced scorecard is a strategy management tool which looks at performance from four perspectives financial, customer, internal processes, and learning growth. This approach gives a full picture of organizational performance.

4. Activity Based Costing (ABC).

ABC which we use to allocate overheads based on what causes them as opposed to the traditional methods we did before. This in turn gives us more precise cost info which is better for decision making.

Benefits of Planning and Control in Accountant’s Role in Management

Integration of planning and control in an organization’s structure provides:

1. Enhanced Decision Making

Access to present and precise info enables managers to make based decisions which in turn support org goals.

2. Effective Resource Distribution

Planning sees to it that resources go where they are most needed, and control sees to which they are used effectively.

3. Improved Performance

Through setting out defined goals and tracking progress organizations may see an increase in efficiency and productivity.

4. Risk Control.

Planning which also includes identification of possible risks and at the same time we have control measures which see to it that these risks are handled effectively.

5. Goal Convergence

Planning and design of processes sees that all departments and staff working towards the same goals which in turn promotes organizational coherence.

Issues in Implementing Planning and Control Systems

Although there are benefits to them, planning and control systems also present:

1. Uncertainty of Prediction

Accurate prediction is a challenge which is true in volatile markets. Sudden changes which may come up can make plans which we have put together go off the rail.

2. Resistance to Change

Employees may go against the change of systems or procedures which they see as restrictive.

3. Complexity

Design outlay and development of strong control systems is a complex process.

4. Issues of Data Quality

Poor quality data results in wrong conclusions and poor decision making.

Real-World Application of Planning and Control

To improve our grasp of what is at play in the area of planning and control look at the case of a manufacturing company. That which we see is a company which sets production targets at the start and also puts together a budget which includes raw materials, labor and overhead costs.

As time goes on we see which products do well and which do not in comparison to the budget. If we see that material costs have gone up we look into it maybe the supplier raised prices or we had more waste than we planned in production.

From our analysis we put in place corrective actions which include better supplier agreements and improved production efficiency. This example also shows how planning and control teams work together to achieve better operation results.

Strategic Importance of Planning and Control

In the long term planning and control in management accounting are essential to the achievement of strategic goals. They enable organizations:

- Adapt to changing market conditions

- Maintain competitive advantage

- Achieve sustainable growth

Through the integration of daily functions with strategic aims management accounting has which for the organization as a whole.

Conclusion

In any organization success is a result of setting clear goals which we achieve. Planning and control in management accounting in this is very much a part of the solution in terms of what we do which is plan and control.

Planning sets the direction which includes setting objectives, forecasting future states, and allocating resources. Control is the function of keeping the organization on track via performance monitoring, analysis of deviations, and put in corrective actions.

Together these functions create what is in effect a continuous improvement cycle which in turn supports better decision making and alignment of operations with strategy. For an organization to do well in today’s competitive business environment it is of great importance that they grasp and put into practice the dual role of management accounting.

By embedding planning and control in all aspects of their operations companies may also adapt to changes but at the same time prepare for the future.

Get more well researched information about Planning and Control in Management Accounting here.